When you default on a second mortgage in Calgary, the lender will immediately issue a formal demand letter for the arrears. If the debt remains unpaid, they will file a Statement of Claim in the Alberta Court of King’s Bench to initiate foreclosure proceedings or sue you directly for the outstanding balance. Depending on your property’s available equity, the lender will either force a judicial sale to liquidate the home or pursue a personal judgment to garnish your wages and seize your assets.

Key Takeaways

- Immediate Legal Action: Lenders can file a Statement of Claim within 30 to 45 days of a missed payment.

- Equity Determines the Strategy: High-equity properties face rapid foreclosure, while low-equity situations often trigger personal lawsuits.

- Credit Devastation: A default will plummet your credit score by 100 to 150 points and remain on your Equifax report for up to seven years.

- Primary Mortgage Risk: Defaulting on secondary financing can trigger a cross-default clause, jeopardizing your first mortgage.

- Negotiation is Possible: Proactive communication with lenders can lead to forbearance agreements, modified terms, or structured settlements before court action begins.

Understanding the Mechanics of Secondary Financing Defaults

Homeowners in Alberta frequently utilize secondary financing to consolidate debt, fund renovations, or manage emergency expenses. However, these financial instruments carry distinct risks. Because primary lenders hold the first position on the property title, secondary lenders assume a significantly higher degree of risk. To compensate, they charge higher interest rates and enforce aggressive recovery protocols when payments cease.

According to 2026 data from the Bank of Canada, the rising cost of borrowing has tightened household budgets, leading to stricter enforcement of loan covenants by private lenders. When a borrower breaches these covenants, the lender’s primary objective is capital preservation.

As David Chen, a senior underwriter at a prominent Alberta lending institution, explains: “Secondary lenders do not have the luxury of patience. Because they are second in line during a payout, any depreciation in property value directly threatens their capital. This is why default protocols are executed with extreme prejudice.”

The Legal Timeline: What Happens When Payments Stop?

The foreclosure process in Alberta is strictly governed by the Law of Property Act. Unlike some jurisdictions that allow non-judicial power of sale, Alberta requires lenders to navigate the court system. Understanding this timeline is crucial for mounting an effective defense.

1. The Missed Payment and Demand Letter

The process begins the moment a payment is returned for non-sufficient funds (NSF). Within 15 to 30 days, the lender’s legal counsel will issue a formal demand letter. This document outlines the exact arrears, accrued interest, and legal fees, providing a strict deadline for remittance.

2. Filing the Statement of Claim

If the demand letter expires without resolution, the lender files a Statement of Claim. This is the official commencement of legal action. Once served, homeowners have exactly 20 days to file a Statement of Defence or a Demand for Notice. Failing to respond allows the lender to proceed with a default judgment. It is vital to understand the difference between a simple default notice and a formal Statement of Claim to protect your legal rights.

3. The Redemption Period

If the court grants a foreclosure order, they will establish a redemption period. This is a legally mandated window—typically ranging from one day to six months—allowing the borrower to pay off the arrears and halt the foreclosure. The length of this period depends heavily on the property’s equity. You can learn more about how courts calculate this window in our guide to Alberta foreclosure redemption periods.

4. Final Order of Foreclosure or Judicial Sale

Once the redemption period expires, the court will issue either a Final Order of Foreclosure (transferring the title directly to the lender) or an Order for Judicial Sale (listing the property on the open market). Navigating the final order timeline requires immediate intervention from legal and financial professionals.

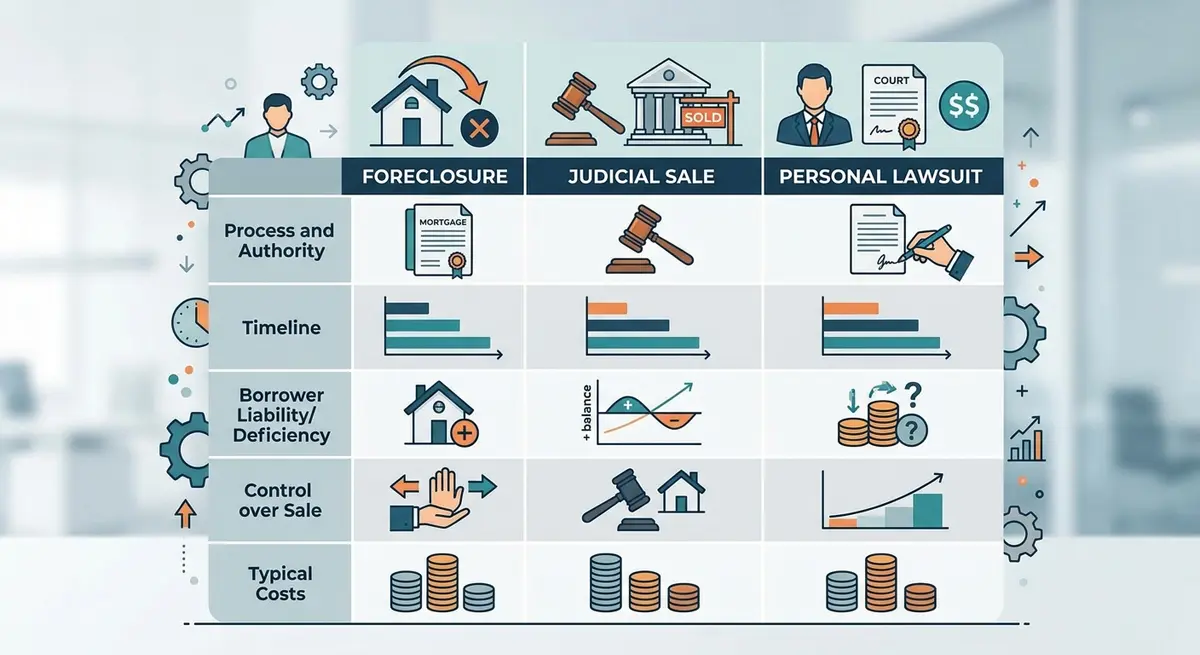

Foreclosure vs. Lawsuits: How Equity Dictates Lender Actions

A critical factor in how a lender responds to a default is the amount of equity remaining in the property. Equity is calculated by taking the current market value of the home and subtracting all registered encumbrances.

High Equity Scenarios

If your property possesses substantial equity (typically over 20%), the secondary lender will aggressively pursue a judicial sale. They are confident that selling the property will generate enough capital to pay off the first mortgage, cover their own principal and interest, and satisfy all legal costs. In these cases, the property itself is the primary target.

Low or Negative Equity Scenarios

If the property has depreciated or is heavily over-leveraged, a judicial sale might not cover the secondary lender’s debt. In Alberta, if a conventional mortgage is uninsured, lenders can sue the borrower on the personal covenant. This means they will bypass the property and target your personal finances.

Research from the Financial Consumer Agency of Canada (FCAC) indicates that unsecured personal judgments are devastating to long-term financial health. Lenders can freeze bank accounts, seize non-exempt assets, and initiate wage garnishment to recover their funds.

The Financial Fallout: Credit Scores and Compounding Debt

The collateral damage of a defaulted loan extends far beyond the immediate threat of losing your home. The financial repercussions can cripple your borrowing capacity for the better part of a decade.

Credit Score Devastation

According to Equifax, a single mortgage default can cause a credit score to plummet by 100 to 150 points. This catastrophic drop reclassifies you as a subprime borrower. Consequently, securing future financing, obtaining credit cards, or even passing a background check for a residential lease becomes exceedingly difficult. These negative marks remain on your credit bureau for six to seven years from the date of first delinquency.

Deficiency Judgments

If the property is sold via judicial sale but the proceeds fall short of the total debt, the lender may pursue a deficiency judgment for the remaining balance. Understanding how deficiency judgments are calculated is essential for borrowers who are underwater on their mortgages.

The Silent Threat of Compounding Interest

Once a loan enters default, standard interest rates are often replaced by punitive default rates, which can exceed 18% to 24% annually. Furthermore, legal fees, property management costs, and appraisal fees are tacked onto the principal balance. Because of the frequency of compounding interest, the total debt can snowball to unmanageable levels within a matter of months.

How Co-Borrowers and Guarantors Are Affected

Many secondary loans require a co-signer or guarantor to mitigate the lender’s risk. If you default, these individuals are equally liable for the debt.

Sarah Jenkins, a Calgary-based real estate attorney, warns: “Borrowers often mistakenly believe that the lender must exhaust all avenues against the primary homeowner before targeting a guarantor. In reality, lenders will pursue whichever party has the most liquid assets. A guarantor’s wages can be garnished just as easily as the primary borrower’s.”

If a family member co-signed your loan, their credit score will suffer the exact same 150-point drop. For a comprehensive breakdown of these risks, review our guide on guarantor liability in Alberta.

Strategic Solutions: How to Halt Foreclosure in 2026

While a default is a severe financial crisis, it is not an irreversible death sentence for your homeownership. Proactive intervention and strategic negotiation can yield favorable outcomes.

Comparing Your Mitigation Options

| Strategy | How It Works | Best Suited For |

|---|---|---|

| Forbearance Agreement | Lender temporarily pauses or reduces payments, adding arrears to the end of the loan. | Temporary job loss or short-term medical emergencies. |

| Loan Modification | Permanent restructuring of the loan terms, such as extending the amortization or lowering the rate. | Permanent reductions in household income. |

| Debt Consolidation Refinance | Securing a new, larger loan to pay off both the primary and secondary mortgages. | Borrowers with substantial equity and recovering credit. |

| Voluntary Sale | Listing the property privately before the court orders a judicial sale. | Situations where the debt is entirely unsustainable. |

Step-by-Step Guide: What to Do If You Cannot Make Your Payment

If you anticipate missing an upcoming payment, immediate action is required to protect your assets and your credit rating. Follow these critical steps:

- Assess Your Financial Reality: Review your household budget. Determine exactly how much of a shortfall you are facing and whether the crisis is temporary or permanent.

- Contact the Lender Proactively: Do not wait for the demand letter. Call your lender before the payment bounces. Lenders are far more receptive to negotiation when borrowers demonstrate transparency and accountability.

- Consult a Specialized Mortgage Broker: Traditional banks will not assist borrowers in active default. You need a broker who specializes in distressed properties and alternative lending to explore buyout options.

- Retain Legal Counsel: If you have been served with a Statement of Claim, you have exactly 20 days to respond. Hire a real estate lawyer immediately to file a Demand for Notice, which ensures you are kept informed of all court proceedings.

- Explore Alternative Financing: If you have sufficient equity, you may qualify for a rescue loan from a private syndicate to pay out the aggressive secondary lender.

For additional resources on managing severe debt, consult the Government of Alberta’s debt management guidelines.

Conclusion

Defaulting on a secondary property loan in Calgary triggers a rapid and aggressive legal process designed to protect the lender’s capital. From the initial demand letter to the potential of a judicial sale or wage garnishment, the consequences are severe and long-lasting. Your credit score, your personal assets, and your primary mortgage are all at risk. However, by understanding the legal timeline, leveraging your available equity, and acting proactively, you can mitigate the damage and find a viable path forward.

Time is your most valuable asset when facing financial distress. Ignoring the problem will only accelerate the legal proceedings and inflate your debt through compounding penalty interest. If you are struggling to maintain your payments or have already received a demand letter, professional intervention is critical. Contact our expert team today to discuss your specific situation and explore tailored strategies to protect your home and your financial future.

Frequently Asked Questions (FAQ)

Can a second mortgage lender force a foreclosure if my first mortgage is in good standing?

Yes. A secondary lender has the legal right to initiate foreclosure proceedings to recover their debt, regardless of the status of your primary loan. However, they must ensure the primary lender is paid out first from the proceeds of any judicial sale.

How long does the foreclosure process take in Calgary in 2026?

The timeline varies based on property equity and court backlogs, but a typical uncontested foreclosure in Alberta takes between four to six months from the first missed payment to the final order. Contested cases or those with lengthy redemption periods can extend beyond a year.

Will I go to jail for defaulting on a mortgage?

No. Defaulting on a loan is a civil matter, not a criminal offense. You cannot be imprisoned for failing to pay your debts in Canada. However, you can face severe civil penalties, including asset seizure and wage garnishment.

What is a cross-default clause?

A cross-default clause is a provision in many primary mortgage contracts stating that a default on any other registered encumbrance (like a secondary loan) automatically constitutes a default on the primary loan. This allows the first lender to also call their loan due.

Can I sell my house while in default?

Yes, you can voluntarily sell your property before the court issues a Final Order of Foreclosure. In fact, a voluntary sale often yields a higher purchase price than a forced judicial sale, allowing you to preserve more of your residual equity.

Does bankruptcy stop a foreclosure in Alberta?

Filing for bankruptcy or a Consumer Proposal triggers an automatic stay of proceedings, which temporarily halts all legal actions, including foreclosure. However, because a mortgage is a secured debt, the lender can eventually apply to the court to lift the stay and proceed with seizing the property.

How can I rebuild my credit after a default?

Rebuilding credit requires time and consistent financial discipline. Start by securing a secured credit card, maintaining low utilization ratios, and ensuring all other bills are paid on time. It typically takes 24 to 36 months of flawless payment history to begin seeing significant score improvements.