Private second mortgages in Calgary are equity-based financial instruments provided by individual investors, syndicates, or Mortgage Investment Corporations (MICs) rather than traditional federally regulated banks. In 2026, these alternative lending solutions prioritize a property’s appraised value and available equity over a borrower’s credit score or traditional income verification. They are designed to provide rapid capital—often funded within 7 to 14 days—allowing homeowners to consolidate high-interest debt, fund business operations, or manage emergency expenses when they cannot pass the strict federal mortgage stress tests.

Key Takeaways

- Equity is the Primary Metric: Approvals are based on your home’s available equity, typically allowing you to borrow up to 75% to 80% of the property’s Loan-to-Value (LTV) ratio.

- Rapid Processing: Unlike traditional banks that take 30 to 60 days, private lenders can issue approvals in 24 to 72 hours, with funding completed in 1 to 2 weeks.

- Flexible Income Verification: Self-employed individuals and gig workers can utilize alternative documentation, such as business bank statements, to prove cash flow.

- Short-Term Bridge Solutions: These are 6- to 24-month loans designed to solve immediate financial hurdles while you transition back to prime lending.

- Mandatory Exit Strategy: Borrowers must have a clear, realistic plan to repay or refinance the principal balance at the end of the mortgage term.

The Rise of Alternative Mortgage Lending in Calgary’s 2026 Market

The Calgary real estate market has experienced dynamic shifts throughout the mid-2020s. With traditional financial institutions tightening their underwriting guidelines under federal mandates, alternative lending sources have surged in popularity. According to 2026 data from the Canada Mortgage and Housing Corporation (CMHC), alternative and private lending now accounts for over 12.4% of the national mortgage market, with Alberta seeing some of the highest adoption rates.

As property values in Calgary have stabilized and grown, homeowners are sitting on unprecedented levels of untapped equity. Private individual investors recognize this opportunity, pooling capital to offer secured loans that yield higher returns than traditional fixed-income investments. This symbiotic relationship provides investors with real estate-backed security while giving borrowers access to much-needed liquidity.

As Dr. Sarah Jenkins, Senior Economist at the Canadian Real Estate Research Institute, explains: “The tightening of the OSFI B-20 stress tests in 2026 has pushed highly qualified but non-traditional borrowers out of the prime lending space. Private capital is no longer a last resort; it is an essential, strategic pillar of Calgary’s housing and economic ecosystem.”

How Private Lenders Differ from Traditional Banks

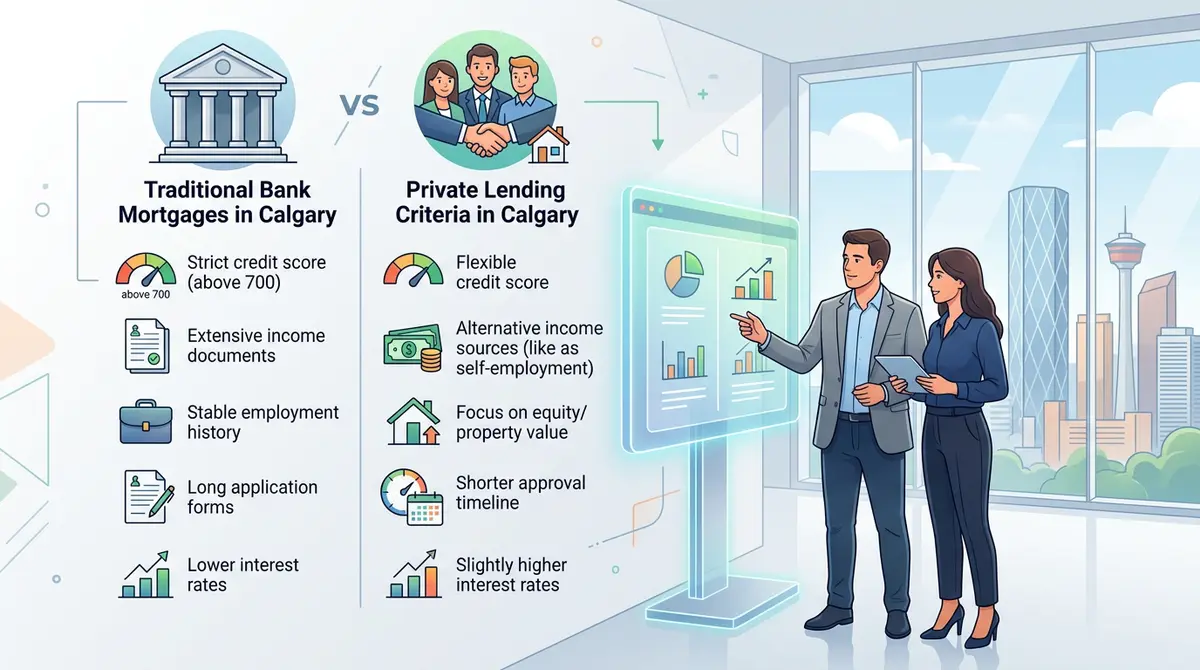

Understanding the fundamental differences between institutional banks and private lenders is crucial for any borrower. While banks operate under strict federal regulations overseen by the Office of the Superintendent of Financial Institutions (OSFI), private lenders in Alberta operate under provincial frameworks regulated by organizations like the Real Estate Council of Alberta (RECA). This jurisdictional difference allows for significantly more flexibility in underwriting.

| Feature | Traditional Banks | Private Lenders |

|---|---|---|

| Primary Approval Metric | Credit score & Income (GDS/TDS ratios) | Property Equity (LTV ratio) |

| Approval Speed | 30 to 60 days | 24 to 72 hours |

| Credit Score Requirement | Typically 680+ | Flexible (Often 550+) |

| Income Verification | T4s, NOAs, Pay Stubs | Bank statements, Stated income |

| Interest Rates (2026) | Prime + 1% to 3% | 8% to 15% (Risk-adjusted) |

| Loan Terms | 3 to 5 years | 6 months to 2 years |

Because private lenders assume a higher level of risk by taking a subordinate (second) position on the property title, they charge higher interest rates. However, for borrowers facing time-sensitive opportunities or temporary financial hurdles, the speed and accessibility of these alternative options far outweigh the premium costs.

Qualification Requirements: Equity Over Credit

The qualification process for alternative financing flips the traditional banking model upside down. Instead of scrutinizing your past financial mistakes, private lenders focus on your current asset wealth. The most critical metric is the Loan-to-Value (LTV) ratio.

Most private lenders in Calgary require a maximum LTV of 75% to 80%. This means the total combined debt of your first and second mortgages cannot exceed 80% of your home’s current appraised value. For example, if your Calgary home is appraised at $600,000, 80% of that value is $480,000. If your current first mortgage balance is $350,000, you have $130,000 of available equity to borrow against.

Beyond equity, private lenders offer immense flexibility regarding income. Self-employed individuals, gig economy workers, and business owners often struggle to prove their net income to banks due to legitimate tax deductions. Private lenders frequently offer stated income second mortgages, allowing borrowers to verify their cash flow through alternative means like 6 to 12 months of business bank statements rather than traditional tax returns.

Step-by-Step: The 2026 Application and Approval Process

Securing funding through alternative channels is designed to be highly efficient. When working with an experienced mortgage brokerage, the process typically follows these five streamlined steps:

- Initial Equity Assessment: The broker evaluates your property’s estimated market value against your current mortgage balance to determine your available borrowing power.

- Document Gathering: While less intensive than a bank, you still need basic paperwork. Reviewing a comprehensive second mortgage document checklist ensures you have your property tax statements, primary mortgage statements, and valid identification ready.

- Property Appraisal: Because the loan is entirely equity-based, the lender will require a professional appraisal from a certified appraiser to confirm the exact current market value of the home.

- Lender Matching & Term Sheet: Your broker presents your file to their network of private investors and MICs. Once a lender issues a term sheet (commitment letter), you review the interest rate, fees, and conditions.

- Legal Review & Funding: Independent legal counsel reviews the mortgage documents with you. Once signed, the lender registers the mortgage on the title and funds are disbursed, often within 7 to 14 days of the initial application.

Interest Rates, Fees, and Cost Structure in 2026

Transparency is vital when navigating the alternative lending space. The cost of borrowing from private sources is higher than prime lending, reflecting the increased risk of holding a second-position lien behind a primary bank. In 2026, interest rates for these loans typically range from 8% to 15% annually, depending heavily on the Bank of Canada’s overnight rate and the specific LTV of the property.

Borrowers must also account for the setup costs, which are usually deducted directly from the gross loan amount rather than paid out-of-pocket. These fees include:

- Lender Fee: Typically 1% to 3% of the loan amount, compensating the private investor for setting up the facility and assuming the risk.

- Brokerage Fee: Usually 1% to 2%, compensating the mortgage broker for sourcing, underwriting, and structuring the deal.

- Legal Fees: Both the borrower and the lender require legal representation, usually totaling between $1,500 and $2,500.

- Appraisal Fee: Approximately $350 to $500, paid upfront by the borrower to an independent appraisal firm.

It is also crucial to understand how interest is calculated. Many borrowers overlook the math behind their payments. Understanding how compounding frequency impacts your total debt load can save you thousands of dollars over the term of the loan. Most private mortgages are structured as interest-only payments, which keeps the monthly cash flow manageable but requires the principal to be paid in full at the end of the term.

Real-World Scenarios: When to Leverage Private Capital

Private mortgages are specialized financial tools designed for specific, short-term goals. They are not meant to be 25-year solutions. Here are two common scenarios where Calgary homeowners successfully leverage alternative lending in 2026:

Scenario 1: High-Interest Debt Consolidation

With consumer credit card rates hovering around 20% to 24%, a Calgary homeowner with $50,000 in unsecured debt is losing thousands to interest every year. Their credit score has dropped to 580 due to high credit utilization, resulting in a bank decline for traditional cash-out refinancing. A private lender provides a $50,000 equity loan at 10%. The borrower pays off the credit cards, immediately improving their monthly cash flow and rapidly boosting their credit score. After 12 months, their score reaches 680, allowing them to refinance the entire amount back into a traditional, low-rate bank mortgage.

Scenario 2: The Self-Employed Business Investment

An entrepreneur needs $80,000 for retail inventory financing to expand their business. Traditional banks require two years of strong net income on Notice of Assessments (NOAs), but the business owner heavily writes down their income for tax purposes. A private lender approves the loan based on the $200,000 of equity in the borrower’s home. The new inventory generates an additional $15,000 in monthly revenue, making the 12% interest rate on the private loan a highly profitable business expense.

Risks, Edge Cases, and Common Mistakes to Avoid

While alternative lending offers immense benefits, it carries inherent risks that must be actively managed. The most significant risk is the lack of a clear exit strategy. Because these mortgages typically have 1-to-2-year terms, borrowers must know exactly how they will pay off the principal when the term matures. Failing to renew or refinance can lead to aggressive collection actions or foreclosure.

Borrowers should actively implement principal reduction strategies if their loan allows for prepayment without severe penalties. Additionally, it is vital to be aware of your legal rights. Under specific provincial regulations, borrowers have consumer protections. For instance, understanding when you can legally rescind a high-interest private mortgage can protect you from predatory lending practices if terms were misrepresented during the signing process.

Another common mistake is using private funds for non-productive assets, such as luxury vacations or depreciating vehicles. Private capital should be deployed strategically: to consolidate higher-interest debt, invest in a business, renovate a property to increase its value, or provide a bridge down payment for another real estate acquisition.

Working with a Fiduciary Mortgage Broker

Navigating the alternative lending landscape requires specialized expertise. The private market is highly fragmented, consisting of hundreds of individual investors, MICs, and syndicate groups. Approaching them directly is nearly impossible for the average consumer, as most reputable investors only accept applications through licensed brokers.

A fiduciary mortgage broker acts as your advocate. By analyzing your unique financial situation, they match you with reputable, vetted lenders who offer the fairest terms. They negotiate interest rates, minimize lender fees, and ensure the mortgage contract aligns with your long-term exit strategy. Their deep understanding of the 2026 Alberta regulatory environment ensures your transaction is secure, compliant, and structured for your ultimate financial success.

Conclusion

In 2026, private second mortgages have evolved into a mainstream financial tool for Calgary homeowners. Whether you are a self-employed entrepreneur needing capital to scale, or a homeowner looking to consolidate high-interest debt and rebuild your credit, leveraging your home’s equity through alternative lending can provide the fast, flexible solution you need. The key to success lies in understanding the costs, working with reputable professionals, and having a rock-solid exit strategy. If you are ready to explore your equity options, contact our team today for a confidential assessment.

Frequently Asked Questions

What is a private individual lender?

A private individual lender is a person or group of private investors who use their own capital to fund mortgages. Unlike banks, they are not federally regulated financial institutions, allowing them to offer more flexible, equity-based underwriting criteria.

How fast can I get approved and funded in Calgary?

In 2026, the approval process typically takes 24 to 72 hours once your application is submitted. Complete funding and legal registration usually occur within 7 to 14 days, assuming all documentation and appraisals are provided promptly.

Do I need a good credit score to qualify?

No, a high credit score is not required. Private lenders focus primarily on the equity in your property, meaning borrowers with credit scores in the 500s can still be approved if they have sufficient home equity.

What are the typical interest rates in 2026?

Interest rates currently range from 8% to 15%. The exact rate depends on your property’s location, the loan-to-value (LTV) ratio, and the perceived risk of the overall application.

Can I pay off my mortgage early?

This depends on the specific terms of your contract. Many lenders charge a prepayment penalty (often 3 months of interest) if you break the term early, while others offer fully open terms.

What happens if I cannot pay back the loan at the end of the term?

If you cannot pay off the principal at maturity, you must either negotiate a renewal with the current lender or refinance with a different lender. Failure to do either will result in the lender initiating foreclosure proceedings to recover their investment.