When deciding between a credit union and a major bank for secondary financing in Calgary, the optimal choice depends entirely on your income structure and borrowing needs. Credit unions excel at providing lower interest rates and flexible underwriting for self-employed individuals, while traditional banks offer superior liquidity, higher loan limits, and advanced digital platforms for standard W2 employees. Making the right choice in 2026 requires a deep understanding of how these distinct institutions evaluate risk, structure their fees, and operate under entirely different regulatory frameworks.

Key Takeaways for 2026 Borrowers

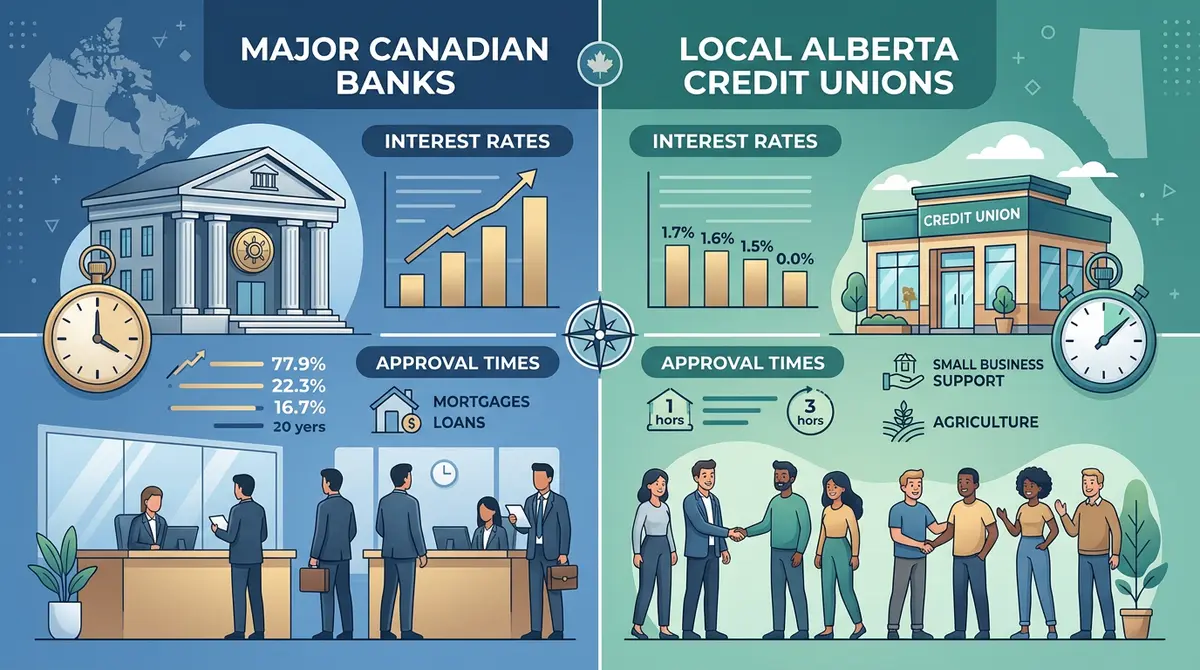

- Interest Rate Variances: Credit unions typically offer rates 0.25% to 0.75% lower than major banks due to their not-for-profit, member-owned cooperative structure.

- Regulatory Differences: Banks must adhere to strict federal OSFI B-20 stress tests, whereas Alberta credit unions operate under provincial guidelines, allowing for common-sense underwriting.

- Approval Speed: Local decision-making at credit unions often results in approvals within 3 to 5 business days, compared to the 7 to 14 days typically required by national bank underwriting centers.

- Lending Limits: Traditional banks maintain a distinct advantage for high-net-worth borrowers, frequently approving secondary loans exceeding $500,000 on luxury properties.

- Income Verification: Entrepreneurs and contractors generally face fewer hurdles at credit unions, which utilize alternative documentation to verify actual cash flow.

Understanding the 2026 Calgary Lending Landscape

The local real estate market has evolved significantly, and the demand for secondary financing has reached unprecedented levels. According to recent 2026 data from the Canada Mortgage and Housing Corporation (CMHC), secondary financing volume in Alberta increased by 14.2% in the first quarter of the year alone. This surge is primarily driven by homeowners leveraging their accumulated equity for debt consolidation, extensive property renovations, and commercial investment opportunities.

As property values fluctuate across different quadrants of the city, lenders have meticulously adjusted their Loan-to-Value (LTV) maximums. Both credit unions and traditional banks typically cap combined LTV at 80%, but their methods for calculating property value and assessing borrower risk diverge sharply. Understanding these institutional philosophies is critical before submitting your application to any lender.

The Regulatory Divide: OSFI vs. Provincial Oversight

The most profound difference between these financial institutions lies in their regulatory oversight. Major Canadian banks are federally regulated by the Office of the Superintendent of Financial Institutions (OSFI). This federal mandate means they must strictly enforce the B-20 stress test, requiring borrowers to qualify at a rate significantly higher than their actual contract rate—typically 2% higher. This severely restricts maximum borrowing power.

Conversely, local credit unions are governed provincially by the Alberta Treasury Board and Finance. This provincial oversight grants them the autonomy to bypass the federal stress test in specific scenarios. For homeowners with substantial equity but non-traditional income structures, this regulatory flexibility is often the deciding factor between a swift approval and a frustrating decline.

The Credit Union Advantage: Flexibility and Community Focus

Credit unions operate on a cooperative model where borrowers are also member-owners. This fundamental structural difference shifts the institution’s primary goal from maximizing shareholder dividends to delivering tangible member value. In the context of secondary financing, residents often find that this translates directly into superior financial benefits.

As Sarah Jenkins, Senior Mortgage Economist at the Alberta Financial Institute, explains: “Credit unions in 2026 are leveraging their provincial regulatory flexibility to capture 34% of Calgary’s alternative lending market. Their ability to look beyond automated credit scores and evaluate the holistic financial health of a borrower is unparalleled.”

Lower Interest Rates and Favorable Fee Structures

Without the relentless pressure to generate massive corporate profits, credit unions consistently undercut bank interest rates. In the current 2026 economic climate, it is common to see credit union rates sitting 0.25% to 0.75% below comparable bank products. On a standard $100,000 loan amortized over 10 years, this rate differential can save a homeowner between $1,500 and $4,500 over the term.

Furthermore, credit unions generally impose lower administrative burdens. Application fees, appraisal costs, and legal disbursements are frequently subsidized or entirely waived for long-standing members. They also tend to offer more generous prepayment privileges, which is vital for borrowers implementing aggressive principal reduction strategies to pay down their debt faster.

Common-Sense Underwriting for Entrepreneurs

The local economy boasts a robust entrepreneurial ecosystem. For self-employed individuals, contractors, and seasonal workers in the energy sector, traditional banks often present insurmountable income verification hurdles. Credit unions excel in this arena by utilizing reasonability tests and accepting alternative documentation, making them the premier choice for stated income second mortgages. By reviewing corporate bank statements rather than relying solely on personal tax returns, they accurately assess a business owner’s true cash flow.

The Traditional Bank Advantage: Liquidity and Technology

While credit unions dominate in underwriting flexibility, traditional major banks—such as RBC, TD, Scotiabank, BMO, and CIBC—wield massive institutional power. Their extensive capital reserves, sophisticated technological infrastructure, and diverse product suites make them highly attractive to specific demographics of borrowers.

According to David Chen, Director of Lending at Calgary Home Finance: “Major banks offer unparalleled liquidity, allowing them to fund secondary loans exceeding $500,000 with highly structured variable products. For high-net-worth individuals with complex portfolios, the major banks remain the gold standard.”

High Lending Limits and Product Diversity

Banks are exceptionally well-equipped to handle high-value transactions. If you own a $2.5 million property in Mount Royal and wish to extract $600,000 in equity, a major bank has the immediate liquidity to facilitate this without syndicating the loan. They offer a wider array of products, including Home Equity Lines of Credit (HELOCs) integrated directly into your primary checking accounts, fixed-rate closed terms, and hybrid financial products.

Relationship Banking and Technological Superiority

For borrowers who already maintain extensive portfolios with a major bank—including mutual funds, primary mortgages, and corporate accounts—relationship pricing can yield significant discounts. These bundled discounts can sometimes neutralize the inherently lower base rates offered by credit unions.

Additionally, the digital experience provided by major banks in 2026 is vastly superior. Real-time application tracking, instant document uploads via mobile apps, and seamless fund transfers appeal heavily to tech-savvy consumers who demand 24/7 access to their financial instruments.

Head-to-Head Comparison Table

To clearly illustrate the differences, review this comprehensive breakdown of how these institutions compare in the current market:

| Feature / Metric | Local Credit Unions | Traditional Major Banks |

|---|---|---|

| Average Interest Rate | Highly competitive (often 0.25% – 0.75% lower) | Standard market rates (relationship discounts available) |

| Regulatory Oversight | Provincial (Alberta Treasury Board) | Federal (OSFI B-20 Stress Test required) |

| Approval Speed | Fast (3 to 5 business days) | Moderate (7 to 14 business days) |

| Income Verification | Flexible (ideal for self-employed/stated income) | Rigid (requires standard T4s and NOAs) |

| Maximum Loan Limits | Moderate (capped around $250,000 – $350,000) | High (can exceed $500,000+ for qualified borrowers) |

| Digital Infrastructure | Functional but basic | Advanced (mobile apps, instant transfers, 24/7 access) |

Step-by-Step: How to Apply for Secondary Financing in Calgary

Securing additional financing requires meticulous preparation, regardless of which institution you choose. Follow these actionable steps to streamline your 2026 application process:

- Calculate Your Available Equity: Determine your home’s current market value and multiply it by 0.80 (the standard 80% LTV limit). Subtract your primary mortgage balance to find your maximum available secondary equity.

- Gather Comprehensive Documentation: Compile your recent pay stubs, T4s, Notices of Assessment (NOAs), property tax statements, and existing mortgage statements. Self-employed borrowers must focus on verifying self-employed mortgage income by preparing 6-12 months of business bank statements.

- Evaluate Your Income Structure: If you are a standard W2 employee with a high credit score, a bank may offer the convenience you desire. If you are self-employed or have a unique financial situation, target a local credit union.

- Submit Applications and Appraisals: Engage a licensed mortgage broker to submit your file. Expect the lender to order a full interior appraisal to verify the property’s condition and 2026 market value.

- Review the Commitment Letter: Carefully analyze the terms, focusing specifically on how compounding frequency impacts your total cost of borrowing over the term.

Real-World Case Studies: Calgary Homeowners in 2026

To demonstrate how these theoretical differences play out in reality, consider these two recent scenarios from the local market.

Case Study 1: The Self-Employed Entrepreneur

Marcus, a freelance software developer living in Evanston, needed $80,000 to renovate his basement into a legal suite. Despite having $200,000 in home equity and a stellar 740 credit score, his primary bank declined his application. Because Marcus aggressively writes down his corporate income to minimize taxes, his personal Notice of Assessment (NOA) showed an income too low to pass the federal OSFI stress test.

Marcus pivoted to a local credit union. The underwriter utilized a reasonability test, reviewing his corporate bank statements to verify his true cash flow. Because they were not bound by federal stress tests, the credit union approved his $80,000 loan at a competitive 8.4% fixed rate within four business days.

Case Study 2: The High-Net-Worth Investor

Elena, a senior executive residing in Aspen Woods, wanted to extract $400,000 from her primary residence to purchase a commercial investment property. She possessed standard, highly verifiable T4 income and maintained over $1 million in investments with a major “Big Five” bank.

While a credit union could have offered a slightly lower base rate, they lacked the appetite for a $400,000 secondary position. Elena’s bank leveraged her existing relationship, offering her a massive HELOC at Prime + 0.50%. The bank’s advanced digital platform allowed her to instantly transfer the funds to her commercial holding company, proving that for high-liquidity needs, traditional banks remain unmatched.

Navigating Edge Cases and Common Pitfalls

When evaluating your borrowing options, you must also consider complex legal and structural edge cases that can derail an application if not handled correctly.

Spousal Consent and Guarantor Complexities

In Alberta, the Dower Act plays a crucial role in real estate transactions. Even if only one spouse is on the property title, the non-titled spouse must provide written consent for any new encumbrance on the homestead. Navigating spousal consent requirements is mandatory at both banks and credit unions, but major banks tend to have more rigid, standardized legal departments that will halt funding if a single signature is misplaced.

Similarly, if your debt service ratios are too high, you may need a co-signer. Using a parent as guarantor is a common strategy. Credit unions are generally more receptive to non-occupant co-borrowers and guarantors, taking a holistic view of the family’s combined net worth, whereas banks strictly input the guarantor’s liabilities into their automated underwriting software.

The Refinance Alternative

Before committing to secondary financing, homeowners must mathematically compare it against breaking their first mortgage. Depending on your current primary rate and the penalty to break it, a second mortgage vs cash out refinance analysis is absolutely essential.

As Dr. Emily Rostova, Real Estate Analyst at the University of Calgary, notes: “In the 2026 rate environment, 68% of Calgary homeowners are choosing secondary loans over refinancing to preserve the ultra-low rates they secured on their primary mortgages between 2021 and 2023. Breaking those primary terms right now is mathematically devastating for most households.”

Conclusion

The decision between a credit union and a traditional bank ultimately hinges on your unique financial profile. If you value personalized service, require flexible income verification, and want the lowest possible interest rate, a credit union is your optimal choice. However, if you need a loan exceeding $300,000, possess standard verifiable income, and demand cutting-edge digital banking tools, a traditional major bank will serve you best.

Always consult with a licensed Alberta mortgage professional who can shop your file to both types of institutions to ensure you secure the most advantageous terms for your specific situation. Ready to explore your equity options? Contact our team today to get started on your customized 2026 financing strategy.

Frequently Asked Questions (FAQ)

Do credit unions have stricter appraisal requirements than banks?

No, credit unions generally have more flexible appraisal requirements. While major banks often demand full interior appraisals from a restricted list of national appraisal management companies, credit unions frequently accept drive-by appraisals or work with a broader network of local independent appraisers.

Can I get secondary financing from a bank if my primary mortgage is with a credit union?

Yes, you can absolutely mix institutions. A major bank will gladly register a secondary position behind a credit union’s primary loan, provided there is sufficient equity in the property and you meet their strict federal debt-service ratio requirements.

Why do credit unions offer lower interest rates?

Credit unions are not-for-profit cooperatives owned by their members. Instead of paying dividends to external corporate shareholders like traditional banks do, credit unions return their profits to members in the form of lower interest rates and significantly reduced administrative fees.

Will borrowing from a credit union affect my credit score differently than a bank?

No, both credit unions and traditional banks report your payment history to major Canadian credit bureaus like Equifax and TransUnion. Consistent, on-time payments to either institution will positively impact your credit score in the exact same manner.

How does the OSFI B-20 stress test impact my bank application?

The OSFI B-20 stress test requires federally regulated banks to qualify you at a rate typically 2% higher than your actual contract rate. This significantly reduces your maximum borrowing power, which is why many homeowners turn to provincially regulated credit unions that can legally bypass this test.

Is it faster to get approved by a credit union or a bank in 2026?

Credit unions are generally faster, often providing approvals within 3 to 5 business days. Because their underwriters and decision-makers are located locally rather than in centralized national hubs, they can review and approve files much more efficiently than major banks.