The mandatory waiting period to reapply for secondary financing in Calgary ranges from 30 days to 12 months, depending entirely on the specific reason for your initial denial and the lender’s risk classification tier. Traditional major banks typically enforce a strict 180-day cooling-off period to allow financial metrics to stabilize, whereas alternative lenders and private mortgage investment corporations (MICs) may accept a new application in as little as 30 to 90 days if measurable financial rehabilitation is proven. Understanding how underwriters calculate this timeline is the critical first step to successfully unlocking your home equity after a rejection.

Key Takeaways

- Credit-based denials require the longest wait: Expect a 6 to 12-month rehabilitation window to rebuild your score after derogatory marks.

- Debt-to-Income (DTI) issues are faster to fix: Waiting periods for high Total Debt Service (TDS) ratios typically span 3 to 6 months.

- Lender tiers dictate timelines: A-lenders demand 180 days, B-lenders require 90-180 days, and private lenders need only 30-90 days.

- Multiple immediate applications damage credit: Submitting identical files to different banks triggers hard inquiries, resetting your waiting clock.

- Documentation must be updated: Never reuse the exact paperwork from a denied file; underwriters require fresh, current financial data.

Decoding the Reapplication Timeline for Calgary Homeowners

When an underwriter declines your application, the resulting waiting period is not an arbitrary punishment. It is a highly calculated window designed by institutional risk models to allow negative credit events to age, debt-to-income (DTI) ratios to stabilize, and property values to appreciate. Navigating the 2026 lending landscape requires a strategic approach to this waiting period, transforming what feels like lost time into a proactive financial rehabilitation phase.

According to 2026 guidelines published by the Financial Consumer Agency of Canada (FCAC), federally regulated institutions must adhere to strict stress-test protocols. These regulations directly influence mandatory waiting periods. Borrowers who attempt to bypass these timelines by immediately submitting identical applications to different traditional banks often trigger multiple hard credit inquiries. This reactionary approach further damages credit scores, signals financial distress to other institutions, and effectively resets the waiting clock.

Categorizing Your Denial: How Rejection Reasons Dictate Your Wait

To accurately project your specific reapplication timeline, you must dissect the underwriter’s formal denial letter. Denials generally fall into three primary categories: credit deficiencies, income verification hurdles, and property valuation shortfalls. Each category carries a distinct rehabilitation requirement.

Credit-Related Denials: The 6 to 12-Month Horizon

Credit score inadequacies and derogatory marks demand the longest rehabilitation windows. If your application was rejected due to a recent consumer proposal, bankruptcy discharge, or a cluster of missed payments, traditional lenders require a minimum of 12 months of flawless repayment history before reconsidering your file. For minor credit infractions, such as high utilization rates, the waiting period typically spans 3 to 6 months.

As Sarah Jenkins, Senior Underwriter at Alberta Financial Group, explains: “The waiting period for credit-related denials is strictly enforced. We need to see a minimum of 180 days of clean repayment data to confirm the borrower has permanently corrected their financial habits. A quick 30-day fix does not satisfy institutional risk models in 2026.”

Income and DTI Rejections: The 3 to 6-Month Window

Debt-to-Income (DTI) ratio issues are the leading cause of financing rejections in the current economic climate. Research from the Bank of Canada indicates that approximately 68% of secondary financing rejections stem from Total Debt Service (TDS) ratios exceeding the maximum 42% to 44% threshold. If your denial was DTI-based, the waiting period is directly tied to how quickly you can pay down revolving debt or increase your verifiable income.

For self-employed Calgarians, income verification presents unique challenges. If your application failed due to insufficient tax documentation, you must wait until your next Notice of Assessment (NOA) is filed. During this time, reviewing the reasonability test for verifying self-employed income is crucial for preparing a bulletproof reapplication.

Appraisal and Equity Shortfalls: Variable Timelines

Property-related denials occur when your home’s appraised value does not support the requested Loan-to-Value (LTV) ratio. In 2026, most traditional lenders cap secondary LTVs at 80%. If your appraisal comes in low, your waiting period depends entirely on local market appreciation or the completion of value-adding renovations.

According to Q1 2026 housing data from the Canada Mortgage and Housing Corporation (CMHC), Calgary property values appreciate at an average annualized rate of 4.2%. Therefore, borrowers relying solely on passive market appreciation to build sufficient equity may face a waiting period of 9 to 12 months before reapplying.

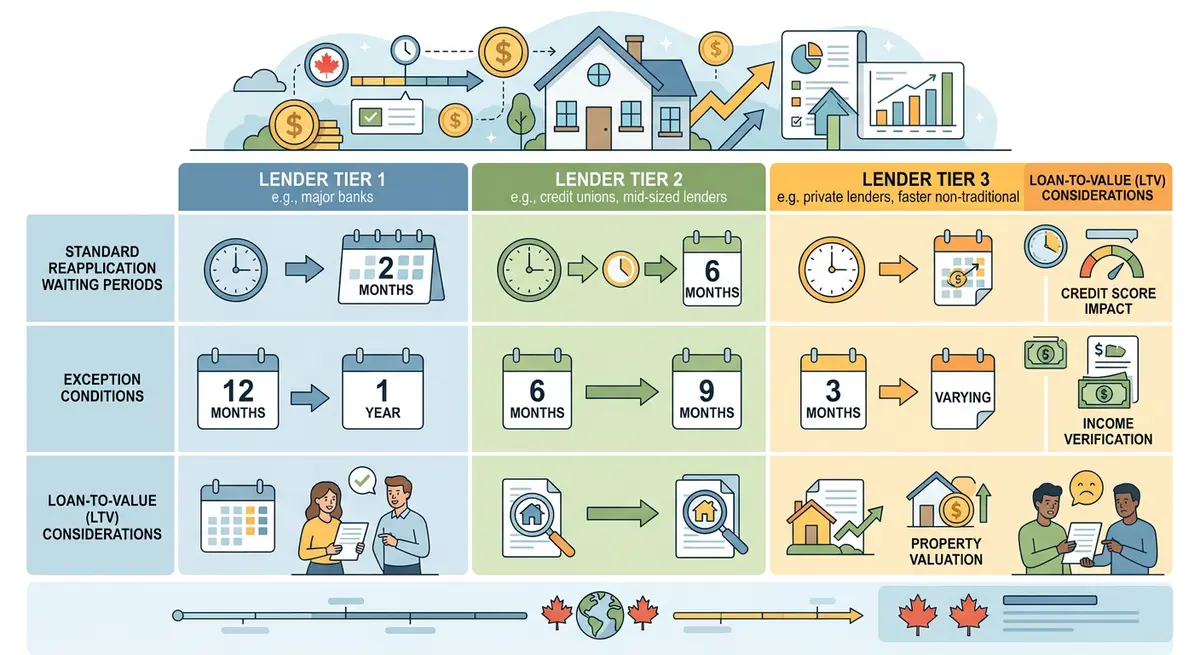

2026 Waiting Periods by Lender Tier

Different financial institutions operate under varying regulatory frameworks, resulting in drastically different reapplication timelines. The table below outlines the standard waiting periods across Calgary’s three primary lender tiers in 2026.

| Lender Tier | Typical Waiting Period | Primary Focus for Re-Approval | Flexibility Level |

|---|---|---|---|

| A-Lenders (Major Banks) | 6 to 12 Months | Strict DTI ratios, excellent credit, stress test compliance | Very Low |

| B-Lenders (Credit Unions) | 3 to 6 Months | Stable employment, localized community ties, moderate credit | Moderate |

| Private Lenders / MICs | 30 to 90 Days | Property equity (LTV below 75%), exit strategy viability | Very High |

If you are transitioning from an A-lender denial to a private lender application, you must understand how to properly document your file. Utilizing a comprehensive secondary financing document checklist ensures you do not face consecutive rejections across different lender tiers.

5 Strategic Steps to Guarantee Approval on Your Next Application

Treat the mandatory waiting period as an active financial rehabilitation phase. Passively waiting for the clock to run out guarantees a second rejection. Implement these five definitive steps to ensure your next application is approved.

- Obtain and Analyze the Denial Letter: Federal regulations mandate that lenders provide a specific reason for adverse credit decisions. Request the formal underwriter notes to pinpoint the exact metric (e.g., TDS ratio, credit utilization, or LTV) that triggered the rejection. It is also vital to retain your secondary financing documents for future reference.

- Audit Your Credit Reports: Pull your comprehensive files from Equifax Canada and TransUnion. Dispute any inaccuracies immediately. A successful dispute can artificially shorten your waiting period by boosting your score 30 to 50 points within 45 days.

- Aggressively Lower Your DTI Ratio: Focus all available capital on paying down high-interest revolving credit cards. Reducing your credit utilization below 30% is the fastest method to improve your Total Debt Service ratio. Exploring principal reduction strategies can accelerate this process.

- Draft a Compelling Letter of Explanation (LOE): Underwriters appreciate transparency. Prepare a detailed document addressing the previous denial and outlining the specific financial improvements you have made. Mastering the art of drafting a compelling letter of explanation significantly increases your credibility.

- Consult a Specialized Mortgage Broker: Do not navigate the reapplication process alone. A licensed broker can assess your rehabilitated profile and match you with a lender whose specific waiting period policies align with your timeline. Furthermore, they can help you explain recent credit inquiries to skeptical underwriters.

How 2026 Calgary Market Conditions Impact Lending Criteria

The macroeconomic environment heavily influences how strictly lenders enforce their waiting periods. In 2026, the Calgary real estate market continues to experience localized volatility, prompting financial institutions to adjust their risk tolerance dynamically. When central banks hold interest rates steady, traditional lenders often rigidify their 180-day waiting periods to hedge against potential defaults.

David Chen, Chief Economist at the Calgary Real Estate Institute, notes: “In the 2026 lending environment, institutional risk aversion is at a five-year high. Lenders are not just looking at the borrower’s current snapshot; they are demanding a sustained, verifiable trajectory of financial stability over a minimum 6-month period.”

Elena Rostova, Senior Policy Analyst at the FCAC, adds that regulatory oversight has tightened regarding how banks evaluate recurring debt. This heightened scrutiny means that document retention and historical proof of income stability are more critical than ever to satisfy stringent 2026 underwriting audits.

Common Mistakes to Avoid During the Waiting Period

Many homeowners inadvertently sabotage their future approval chances while waiting out their mandatory cooling-off period. The most detrimental mistake is taking on new consumer debt. Financing a vehicle, opening a new credit card, or co-signing a loan for a family member will immediately alter your Gross Debt Service (GDS) and TDS ratios, often extending your waiting period by an additional six months.

Another frequent error is changing employment. Lenders prioritize income stability. Moving from a salaried position to a commission-based role, or starting a new business during your waiting period, resets the employment verification clock. Most A-lenders require a minimum of two years of consistent income history in the same industry. If you must change jobs, ensure there is no gap in employment and that your base salary remains equal to or higher than your previous role.

Alternative Financing to Bridge the Gap

If your mandatory reapplication timeline extends beyond your immediate capital needs, alternative financing solutions can bridge the gap. While waiting for traditional A-lender eligibility, many homeowners pivot to alternative products that feature less stringent qualification criteria.

Home Equity Lines of Credit (HELOCs) sometimes utilize different underwriting algorithms than lump-sum loans. However, if your DTI is the primary issue, an unsecured product might be necessary. Comparing home equity loans against unsecured credit helps determine which interim solution best protects your long-term financial health without jeopardizing your future reapplication.

For self-employed individuals or entrepreneurs who cannot wait six months for traditional bank approval, the private market offers immediate liquidity. Exploring stated income alternative loans allows Calgary business owners to bypass traditional NOA requirements, effectively reducing the waiting period to zero, albeit at higher interest rates.

Frequently Asked Questions (FAQ)

Does a denied application hurt my credit score?

The denial itself does not appear on your credit report and does not directly lower your score. However, the hard inquiry generated by the lender during the application process typically reduces your credit score by 3 to 5 points temporarily.

Can I apply with a different bank immediately after being denied?

While legally permissible, applying with a different traditional bank immediately is highly discouraged. Multiple hard inquiries within a short timeframe signal financial distress to underwriters, almost guaranteeing a subsequent denial and extending your overall waiting period.

How long must I wait to reapply if my home appraisal was too low?

If your denial was strictly LTV-based due to a low appraisal, there is no mandatory regulatory waiting period. You can reapply as soon as you complete value-adding renovations or when verifiable local market data shows sufficient property appreciation.

Will paying off a collection account shorten my waiting period?

Paying off a collection account demonstrates financial responsibility, but traditional A-lenders still typically require a 6-month seasoning period after the zero-balance is reported. Private lenders, however, may approve your reapplication immediately upon proof of payment.

Do credit unions have shorter waiting periods than major banks in Calgary?

Yes, Calgary-based credit unions generally offer more flexible reapplication timelines than federally regulated major banks. Because they evaluate community ties and overall financial character, credit unions often reduce the standard 180-day wait to 90 days for existing members.

Can a mortgage broker bypass the waiting period?

A broker cannot bypass a specific lender’s internal policies, but they can redirect your application to a different lender tier. If an A-lender requires a 6-month wait, a broker might successfully place your file with a B-lender or private MIC immediately, provided you meet their specific criteria.

Conclusion

The waiting period following a financing denial is not the end of your home equity journey; it is a vital window for financial rehabilitation. By understanding the specific reasons behind your rejection—whether rooted in credit history, debt-to-income ratios, or property valuation—you can strategically align your next steps with the appropriate lender tier. Taking proactive measures to audit your credit, aggressively pay down revolving debt, and prepare a comprehensive letter of explanation will transform a temporary setback into a guaranteed future approval.

If you are currently navigating a mandatory waiting period and need expert guidance to prepare your file for a successful reapplication, do not leave your next attempt to chance. Contact our team today to speak with a licensed Calgary specialist who can help you rebuild your profile and unlock the equity in your home.