To successfully protect your Calgary property from foreclosure rescue fraud, you must absolutely refuse to pay upfront fees, never sign over your property title to an unverified third party, and strictly authenticate all advisory credentials through official provincial regulatory bodies. Legitimate loss mitigation requires direct, documented communication with your primary mortgage lender and consulting a licensed real estate attorney before executing any legal documents. Relying on unsolicited rescue offers rather than verified legal channels often accelerates the loss of your home and strips you of your remaining equity.

Key Takeaways

- Zero Upfront Fees: Legitimate foreclosure assistance programs and credit counselors will never demand thousands of dollars before providing services.

- Protect Your Title: Never sign a quitclaim deed or temporarily transfer your property title to a “rescue” agency under any circumstances.

- Direct Lender Contact: Maintain open communication with your bank; scammers thrive by isolating you from your primary lender.

- Verify Credentials: Always cross-reference professionals with the Real Estate Council of Alberta (RECA) or the Law Society of Alberta.

- Understand the Timeline: Alberta law provides mandatory redemption periods and court oversight, meaning you cannot be legally evicted overnight.

The Rise of Foreclosure Fraud in Calgary’s 2026 Market

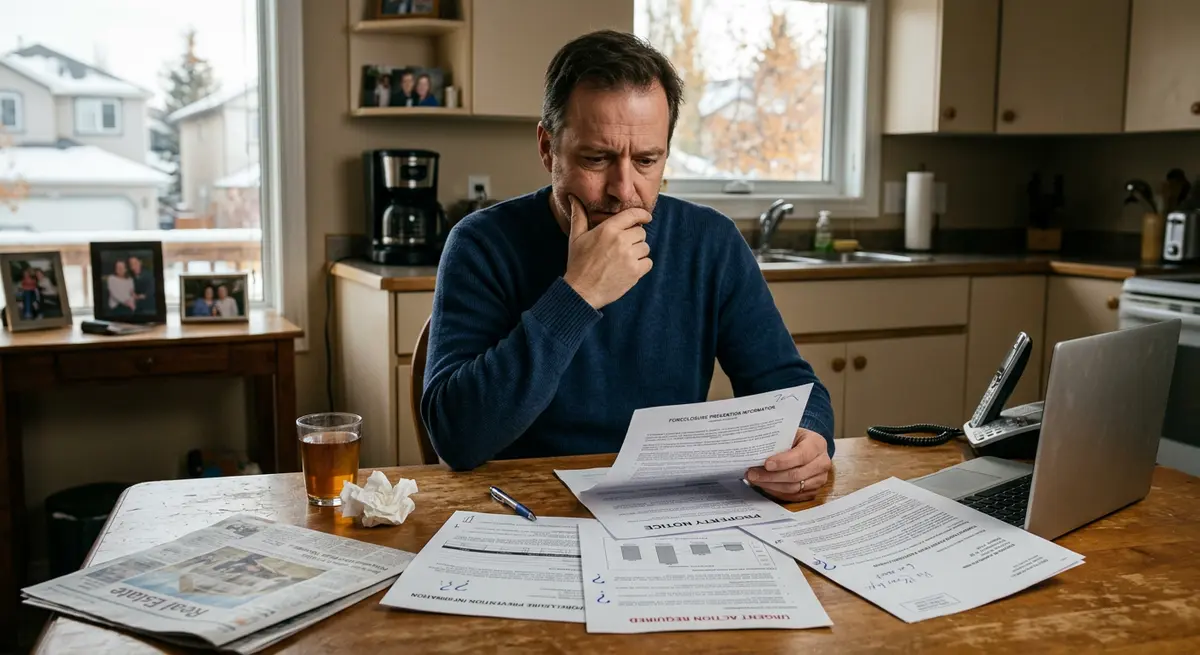

Facing the potential loss of a home is arguably one of the most stressful financial crises a family can endure. In Calgary’s dynamic 2026 real estate market, economic pressures, inflation, and shifting interest rates have unfortunately created a fertile breeding ground for predatory schemes. Desperation often clouds judgment, making vulnerable property owners prime targets for unscrupulous actors promising miraculous solutions.

The landscape of property fraud has shifted dramatically over the past few years. In Q1 2026, the Canadian Anti-Fraud Centre reported a 22% surge in property-related fraud across Western Canada. Scammers actively monitor public registries, identifying homeowners who have recently fallen behind on payments. Data indicates that within 48 hours of a public default notice being filed, up to 45% of targeted homeowners report receiving unsolicited rescue offers via text, email, or door-to-door visits.

As Sarah Jenkins, Senior Fraud Investigator at the Canadian Anti-Fraud Centre, explains: “Scammers in 2026 are using highly sophisticated AI-generated documents that mimic official bank letterheads perfectly. They create a false sense of urgency, forcing homeowners into catastrophic financial decisions before they can consult legal counsel.”

Calgary’s economy remains heavily tied to the cyclical energy sector. When job losses occur, mortgage defaults inevitably follow. Understanding the actual legal timeline is your strongest defense against artificial urgency. Familiarize yourself with the difference between a Notice of Default and a Statement of Claim to know exactly where you stand in the legal process before a scammer tries to convince you that eviction is imminent.

Recognizing the Most Common Predatory Schemes

To effectively shield your assets, you must recognize the specific methodologies employed by these fraudulent operations. They typically fall into two primary categories, each meticulously designed to strip equity or extract cash from desperate homeowners.

Equity Stripping and Title Transfer Fraud

Equity stripping remains the most devastating form of property fraud in Alberta. In this scenario, a rescue company offers to pay off your mortgage arrears if you temporarily transfer the property title to them. They promise you can rent the home and buy it back later once your credit improves. In reality, once they hold the title, they extract the remaining equity through new loans and eventually evict you.

Victims of this scam lose up to 60% of their accumulated home equity instantly. According to Marcus Thorne, Lead Real Estate Attorney at the Alberta Legal Defense Network: “Never sign a quitclaim deed under the guise of a temporary title transfer. Legitimate loss mitigation does not require you to surrender your property rights. Once the title is transferred, recovering your home becomes a complex legal battle where legal fees for recovery average $15,000.”

Phantom Help and Fake Government Programs

Phantom help scams involve companies charging exorbitant upfront fees for services they never intend to provide. They often claim affiliation with the Financial Consumer Agency of Canada or invent fake provincial relief programs. They instruct you to stop communicating with your bank and send “trial mortgage payments” directly to them instead.

The average scam of this nature costs Calgary homeowners $8,500 in phantom fees before they realize no negotiations have taken place. If you are facing legal action, you must respond through proper channels. Learn about responding to a foreclosure statement of claim rather than trusting an unverified third party to handle your legal defense.

7 Undeniable Red Flags of a Foreclosure Scam

Recognizing the warning signs is your first line of defense against financial predators. Industry data shows that 78% of fraudulent companies demand upfront fees before providing any tangible service. If you encounter any of the following red flags, immediately cease communication:

- Demands for Upfront Fees: Legitimate credit counselors and loss mitigation experts do not charge thousands of dollars in advance. It is illegal in many jurisdictions to charge upfront for foreclosure rescue services.

- Guarantees to Stop Foreclosure: No one can guarantee a specific outcome in a legal proceeding. Only a judge or your lender can officially halt the process.

- Instructions to Ignore Your Lender: Scammers want to isolate you. Always maintain contact with your bank.

- Pressure to Sign Unread Documents: High-pressure tactics, such as refusing to let you read a contract thoroughly, are a hallmark of fraud.

- Unsolicited Contact: Be highly wary of door-to-door visitors or aggressive telemarketers claiming they can save your home immediately after a missed payment.

- Requests for Direct Payment: Never send mortgage payments to anyone other than your official loan servicer.

- Title Transfer Requests: Never surrender your property deed under any circumstances.

Understanding your rights during the foreclosure questioning process can prevent you from being intimidated by scammers claiming they can bypass the courts entirely.

Step-by-Step: How to Protect Your Home and Equity

Taking proactive, documented steps is essential for protecting your property. Follow this definitive 2026 guide to navigate financial distress safely and legally.

- Contact Your Lender Immediately: The moment you anticipate missing a payment, call your bank’s loss mitigation department. Research shows that 93% of successful loss mitigation cases involve direct, early lender communication. They offer legitimate forbearance and modification programs.

- Verify All Credentials: Cross-reference any advisory company with the Law Society of Alberta or the Real Estate Council of Alberta (RECA). If they are not licensed, do not engage.

- Seek Independent Legal Counsel: Hire your own real estate lawyer. Do not use the “in-house” attorney provided by a rescue company, as their primary fiduciary duty is to the scammer, not you.

- Document Every Interaction: Keep meticulous records of all phone calls, emails, and letters. Note the dates, times, and names of representatives you speak with.

- Report Suspicious Activity: If you suspect fraud, report it to the authorities immediately to protect yourself and others in your community.

According to David Ross, Director of the Canadian Mortgage Protection Coalition: “The most effective defense against foreclosure fraud is direct, documented communication with your primary lender. Scammers thrive in the silence between a borrower and their bank.” Be aware of the timeline you are working against by reviewing the final order of foreclosure timeline for Calgary homeowners.

Comparison: Legitimate Loss Mitigation vs. Fraudulent Rescue Offers

Distinguishing between genuine assistance and a scam can be difficult when under extreme stress. This comparison table highlights the stark differences in their operational models.

| Feature | Legitimate Assistance | Fraudulent Scheme |

|---|---|---|

| Fee Structure | Free or low-cost post-service fees | High upfront fees demanded in cash or wire |

| Communication | Encourages direct lender contact | Demands you cut off all lender contact |

| Guarantees | Explains risks and legal options realistically | Guarantees to save your home completely |

| Documentation | Provides ample time for legal review | High-pressure, sign-immediately tactics |

| Property Title | Title remains securely in your name | Requires you to sign over the property deed |

Understanding Alberta’s Legal Protections for Homeowners

Alberta’s legal framework provides robust protections for distressed borrowers. The Law of Property Act strictly regulates how lenders can recover debts. Scammers often lie about these laws to create artificial panic and force hasty decisions. For instance, understanding the redemption period calculation in Alberta proves that you have a legally mandated window (typically six months) to sell your property or refinance, regardless of what a scammer tells you about immediate eviction.

Furthermore, the courts oversee the entire process. A lender cannot simply seize your home overnight. There are mandatory notice periods, court hearings, and redemption periods. Unfortunately, statistics show that only 12% of victims recover their funds once they willingly transfer title or pay fraudulent fees, making prevention your only true safeguard.

If the property is eventually sold for less than what you owe, you must understand the deficiency judgment calculation, a legal reality which scammers often falsely promise to eliminate entirely. Knowledge of these mechanisms strips scammers of their primary weapon: fear of the unknown.

Where to Find Genuine Foreclosure Assistance in 2026

If you are struggling to make payments in 2026, legitimate help is readily available. Start by contacting non-profit credit counseling agencies approved by the provincial government. These organizations provide free financial assessments and can help negotiate with your creditors ethically and legally.

Additionally, consult with licensed mortgage brokers who can explore legitimate refinancing options. Sometimes, a regulated second mortgage or a debt consolidation loan can provide the necessary capital to cure mortgage arrears. Always ensure any broker is registered with provincial authorities.

In some complex legal situations involving title disputes or predatory lending claims, you might need to understand the difference between foreclosure and quiet title actions to protect your ownership rights fully. Always rely on licensed professionals rather than unsolicited “rescue” agencies.

Frequently Asked Questions (FAQ)

What is the most common foreclosure scam in Calgary?

The most common scheme in 2026 is the phantom help scam, where fraudulent companies charge large upfront fees while falsely promising to negotiate a loan modification with your bank. They ultimately provide no service, leaving the homeowner closer to losing their property.

Can a company legally guarantee to stop my foreclosure?

No. It is illegal and practically impossible for any third-party company to guarantee they can stop a legal foreclosure proceeding. Only a court order or a direct, formalized agreement with your primary mortgage lender can halt the process.

Should I sign a quitclaim deed to save my home?

Absolutely not. Signing a quitclaim deed transfers your ownership rights to another party while leaving you entirely responsible for the mortgage debt. This is a primary tactic used in devastating equity stripping scams.

How can I verify if a foreclosure prevention company is legitimate?

You should verify the company’s credentials through the Better Business Bureau, the Real Estate Council of Alberta (RECA), and the Law Society of Alberta. Legitimate agencies will never demand upfront fees or pressure you into immediate decisions.

What should I do if I suspect I am being scammed?

Immediately cease all communication with the suspected scammers and do not sign any further documents. Report the activity to the Canadian Anti-Fraud Centre and consult with a licensed real estate lawyer to protect your remaining assets.

Does the Alberta government offer foreclosure relief programs?

While the provincial government provides resources for financial counseling and consumer protection, there are no secret government grants that instantly pay off mortgage arrears. Always verify any claimed government program directly through official Service Alberta channels.

Conclusion

Protecting your home from predatory schemes requires vigilance, a solid understanding of Alberta real estate law, and a steadfast refusal to be rushed into catastrophic financial decisions. By recognizing the red flags of equity stripping and phantom help, and by maintaining direct communication with your lender, you can navigate financial distress safely. Remember, legitimate help is always transparent, verifiable, and never demands exorbitant upfront fees.

If you are facing mortgage difficulties and need trustworthy, licensed guidance to explore your financing options, do not face it alone. Get in touch with our team today to discuss safe, regulated strategies to protect your home equity.