When you make the final payment on a secondary property lien in Calgary, the lender is legally obligated to issue a Discharge of Charge to the Alberta Land Titles Office. This administrative action removes the encumbrance from your property title, instantly freeing up monthly cash flow, lowering your debt-to-income (DTI) ratio, and granting you unencumbered access to your accumulated home equity. However, achieving a zero balance does not automatically clear your title. Homeowners must actively verify the legal discharge process, navigate potential tax implications, and strategically deploy their reclaimed capital to transition from high-interest debt management to accelerated wealth accumulation.

Key Takeaways

- Verification is Mandatory: A zero balance does not mean a clear title. You must ensure the Discharge of Mortgage is officially registered with the Alberta Land Titles Office.

- Instant Liquidity: Eliminating a secondary lien instantly reclaims hundreds or thousands of dollars in monthly cash flow, providing a powerful buffer against inflation.

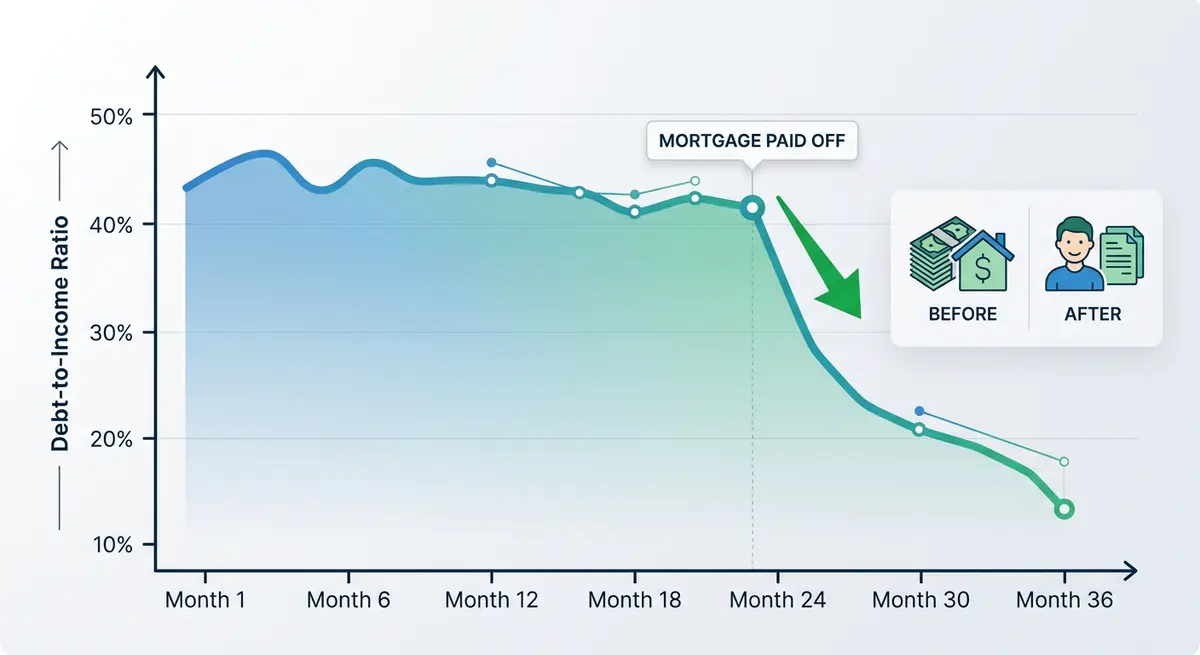

- DTI Transformation: Your Debt-to-Income ratio will drop significantly (typically by 10% to 15%), restoring your borrowing power for prime lending rates.

- Tax Deductions: If the borrowed funds were used for investment purposes, paying off the principal eliminates your ability to claim the interest as a tax deduction.

- Strategic Reinvestment: To maximize financial momentum, immediately redirect your former payment amount into compounding assets like TFSAs or RRSPs.

The Administrative Reality: How the Legal Discharge Process Works in Alberta

Making your final payment is a monumental financial achievement, but it does not automatically clear your property title. The legal process of removing a secondary encumbrance requires specific administrative steps governed by provincial law. Until the lien is officially discharged, the lender technically maintains a legal claim against your property, which can severely complicate future sales or refinancing efforts.

As David Chen, Lead Real Estate Attorney at Alberta Property Law Group, explains: “A common misconception among homeowners is that a zero balance equals a clear title. In reality, the lender must actively register a Discharge of Mortgage with the provincial registry. Homeowners must verify this step to prevent title complications during future real estate transactions.”

To ensure your title is completely cleared, you must follow a strict sequential process. First, you must request an official payout statement from your lender. This document details the exact final balance, including any accrued interest, administrative penalties, and discharge fees. Once you remit the final funds before the statement’s expiration date, the lender prepares a formal Discharge of Charge document.

Step-by-Step Guide to Clearing Your Property Title

- Request a Payout Statement: Contact your lender 15 to 30 days before your intended payoff date to request a legally binding payout statement.

- Review the Fees: In 2026, discharge fees in Alberta typically range from $250 to $400. This covers the lender’s legal preparation costs and the provincial registration fees.

- Remit the Exact Funds: Transfer the exact amount specified on the statement. Even a discrepancy of a few cents can halt the discharge process.

- Monitor the Registration: The lender submits the document to the Alberta Land Titles Office. Processing times at the registry currently average 30 to 45 days.

- Obtain a Certified Copy: Once completed, pull a fresh copy of your property title to verify the secondary charge has been completely removed.

Sarah Jenkins, Senior Title Specialist at the Alberta Land Titles Office, notes: “We process thousands of discharges monthly, but delays often occur when lenders submit incomplete paperwork. Homeowners should always follow up 45 days after their final payment to ensure the registration was successful.” After the process is complete, understanding the rules around retaining your mortgage paperwork is vital for your personal records and future audits.

Immediate Financial Impact: Cash Flow and Debt-to-Income Improvements

The most immediate and tangible benefit of eliminating secondary debt is the dramatic improvement in your monthly liquidity. Secondary financing typically carries higher interest rates than primary mortgages. According to 2026 data from the Bank of Canada, alternative lending rates average between 8.5% and 12.9% depending on the borrower’s risk profile.

Eliminating a $75,000 secondary loan at a 10% interest rate instantly frees up approximately $990 per month in cash flow. This sudden surplus provides a powerful buffer against economic fluctuations and unexpected expenses. Before reaching this finish line, many proactive homeowners utilize specific principal reduction methods to accelerate their payoff date and minimize total interest paid.

Financial Profile Comparison: Before vs. After Payoff

| Financial Metric | Active Secondary Lien | After Full Payoff |

|---|---|---|

| Debt-to-Income (DTI) | Elevated (often near 40-43% maximums) | Significantly Reduced (drops by 10-15%) |

| Monthly Cash Flow | Constrained by dual payments | Maximized and available for investment |

| Property Title | Encumbered by multiple legal liens | Clear (subject only to the primary mortgage) |

| Borrowing Power | Limited strictly to alternative lenders | Restored for prime lending rates |

Successfully completing a major debt obligation fundamentally restructures your credit profile. While you might experience a temporary 5 to 15 point dip in your credit score due to the closure of an active credit account, the long-term benefits to your borrowing capacity are immense. The most critical improvement is the reduction of your Debt-to-Income (DTI) ratio.

Marcus Thorne, Chief Credit Strategist at Calgary Financial Analytics, notes: “Prime lenders care significantly more about your available monthly cash flow than a slightly older credit age. Eliminating a secondary payment drops your DTI, instantly qualifying you for Tier 1 lending products that were previously out of reach.” This improved DTI is particularly crucial if you are weighing a cash-out refinance for your primary mortgage to consolidate other debts at a lower interest rate.

Tax Implications for Calgary Homeowners After Payoff

The tax consequences of paying off your secondary financing depend entirely on how the borrowed funds were originally deployed. The Canada Revenue Agency (CRA) allows homeowners to deduct interest carrying charges if the borrowed money was used to generate investment income. This strategy, commonly known as the Smith Maneuver, involves using home equity to purchase dividend-paying stocks or rental properties.

If your loan was used for investment purposes, paying off the principal eliminates your ability to claim that interest as a tax deduction against your investment income. You are effectively trading a tax deduction for increased monthly cash flow and reduced financial risk. Homeowners must weigh the after-tax cost of the debt against the expected return of their investments.

Conversely, if the funds were used for personal reasons—such as home renovations, funding a wedding, or consolidating consumer credit cards—the interest was never tax-deductible. In this scenario, paying off the loan provides a 100% net positive financial benefit with zero negative tax implications. Understanding the mathematical realities of your loans is critical, especially when considering how compounding frequency impacts your debt over time. Eliminating a daily-compounding high-interest loan always yields a guaranteed, tax-free return equivalent to the loan’s interest rate.

Strategic Wealth Building: What to Do With Your Reclaimed Capital

Once you officially clear your title in Calgary, you must decide how to deploy your reclaimed cash flow and newly accessible home equity. Financial complacency is the enemy of wealth generation. Allowing your newly freed $990 per month to be absorbed by lifestyle inflation is a critical error.

Elena Rostova, Wealth Manager at Prairie Capital, advises: “The day you pay off your secondary financing is the day you transition from debt management to wealth accumulation. Automate that old payment amount into an index fund or retirement account immediately, before lifestyle creep consumes the surplus.”

With benchmark home prices in the city stabilizing near $615,000 in early 2026, according to the Calgary Real Estate Board (CREB), your unencumbered equity represents a massive asset. Redirecting your former monthly payment into a Tax-Free Savings Account (TFSA) or redirecting funds into retirement accounts like an RRSP can yield exponential long-term growth. By capturing 100% of future property appreciation as personal wealth, rather than having it offset by high-interest debt service, you dramatically accelerate your net worth trajectory.

Navigating Edge Cases and Common Administrative Pitfalls

While paying off a major loan is a cause for celebration, homeowners must remain vigilant to avoid administrative pitfalls. A frequent mistake is assuming the lender will automatically handle the discharge without any prompting or fees. Always request a final payout statement in writing and follow up 45 days later to ensure the lien has been removed from the provincial registry.

What Happens if Your Private Lender Disappears?

In rare edge cases, a private lender or individual investor might cease operations, pass away, or become unresponsive before discharging the lien. If this occurs, the encumbrance remains frozen on your title, preventing you from selling or refinancing the property.

To resolve this, you may need to hire a specialized real estate lawyer to file a court application proving the debt was satisfied. This process involves obtaining a judge’s order to clear the title, often requiring you to explore pursuing a quiet title action. Furthermore, if the property was previously distressed, you might also need to look into discharging a lis pendens if legal actions were previously threatened against the estate.

Leveraging Your Unencumbered Home Equity in 2026

After clearing the secondary lien, many homeowners choose to establish a safety net using their newly unencumbered equity. A common strategy is opening a Home Equity Line of Credit (HELOC) in the secondary position to serve as a low-cost emergency fund. Because the HELOC sits at a zero balance until used, it costs nothing monthly but provides immediate liquidity for emergencies or investment opportunities.

Homeowners often debate whether to keep a zero-balance HELOC or transition to relying on an unsecured line of credit. A HELOC generally offers significantly lower interest rates (often prime plus 0.5%), but requires a registered charge on your title. An unsecured line of credit carries higher interest rates (often prime plus 4% to 8%) but keeps your property title completely clear of any secondary encumbrances. The choice depends entirely on your risk tolerance and future borrowing needs.

Frequently Asked Questions (FAQ)

Does paying off my loan automatically clear my property title?

No, clearing your title does not happen automatically. Your lender must draft a formal Discharge of Mortgage document and register it with the Alberta Land Titles Office to legally remove the lien from your property.

Will my credit score drop when I pay off my secondary financing in Calgary?

You may experience a minor, temporary drop of 5 to 15 points because an active credit account has been closed. However, your significantly improved Debt-to-Income ratio will make you much more attractive to future lenders, outweighing the temporary dip.

How much does it cost to discharge a lien in Alberta in 2026?

Discharge and administrative fees typically range from $250 to $400. This covers the lender’s legal preparation costs and the provincial registration fees required by the Alberta Land Titles Office.

How long does the discharge process take after the final payment?

Once the final funds clear, it generally takes lenders 2 to 4 weeks to prepare the legal documents. The Alberta Land Titles Office then requires an additional 30 to 45 days to process the registration and update the title.

What happens to my tax deductions after I pay off the principal?

If the loan was used for investment purposes (like the Smith Maneuver), paying off the principal eliminates your ability to claim the interest as a tax deduction. If the funds were used for personal expenses, there are no negative tax implications.

What should I do if my private lender goes out of business before discharging the mortgage?

If a private lender dissolves or becomes unresponsive without discharging the lien, you will need to hire a real estate lawyer. They can file a court application to prove the debt was satisfied and obtain a judge’s order to clear the title.

Conclusion

Paying off your secondary financing in Calgary is a transformative financial milestone that shifts your economic trajectory from debt management to wealth accumulation. By understanding the administrative requirements of the Alberta Land Titles Office, anticipating the minor impacts on your credit score, and strategically reinvesting your reclaimed monthly cash flow, you can maximize the benefits of your unencumbered home equity. Always verify that your discharge has been officially registered, and consult with financial professionals to optimize your tax strategy moving forward. If you need assistance navigating the complexities of property titles, discharges, or leveraging your home equity in 2026, contact us today to speak with our team of Calgary real estate experts.