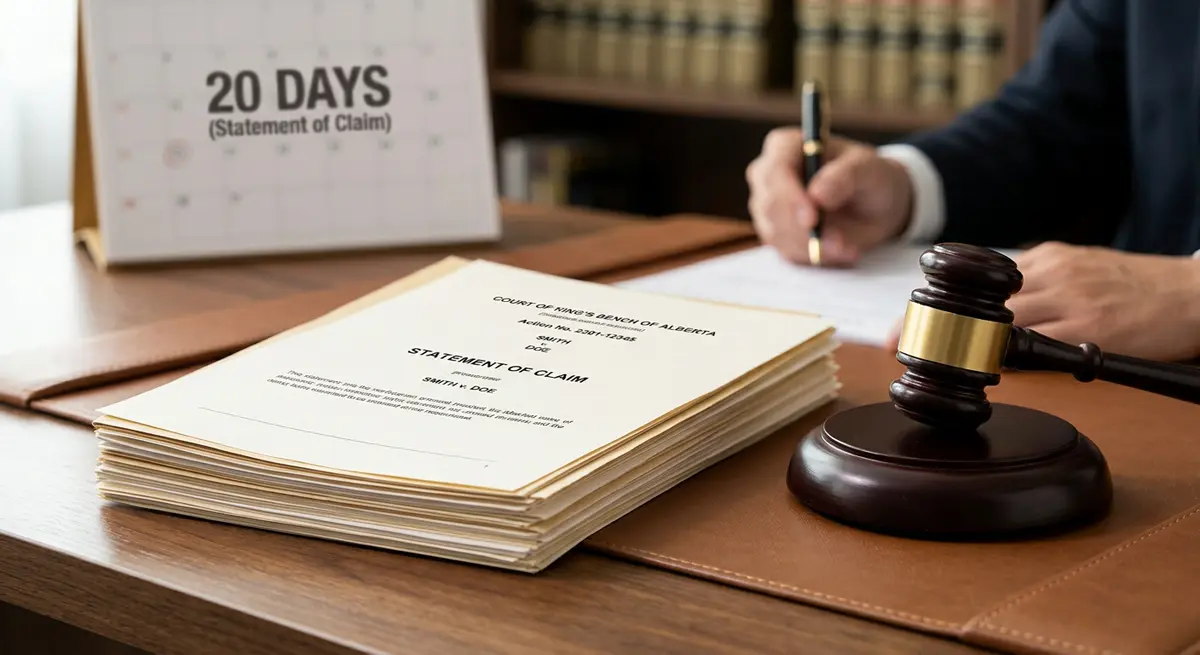

When you receive a Statement of Claim for foreclosure in Alberta, you have exactly 20 calendar days to file a formal legal response with the Court of King’s Bench. Failing to submit a Statement of Defence or Demand of Notice within this strict timeframe allows your lender to obtain a default judgment, accelerating the forced sale or transfer of your property. Immediate, documented action is the only way to preserve your legal rights and keep negotiation channels open.

Key Takeaways

- 20-Day Deadline: You have exactly 20 calendar days from the date you are served to file a formal response with the Alberta courts.

- Formal Response Required: Informal phone calls with your bank do not pause the legal clock; you must file specific court forms.

- Two Main Options: Homeowners typically file either a Statement of Defence (to dispute the claim) or a Demand of Notice (to stay informed of proceedings).

- Redemption Period: Alberta law generally provides a 6-month redemption period to pay arrears and halt the foreclosure.

- Credit Impact: A completed foreclosure will severely impact your credit score for up to seven years.

- Professional Help: Engaging legal and financial experts early increases your chances of retaining your home or minimizing financial damage.

Understanding the Statement of Claim in Alberta’s Legal System

The arrival of a Statement of Claim marks the official transition of your mortgage default from a private contractual dispute into a public legal proceeding. In Alberta, lenders initiate this process through the Court of King’s Bench. This document outlines the lender’s allegations, including the exact amount of arrears, the total outstanding mortgage balance, and their formal request to the court to seize or sell your property.

According to 2026 data from the Financial Consumer Agency of Canada, over 60% of homeowners facing legal action wait too long to act, operating under the false assumption that the initial paperwork is merely another warning letter. It is not. The Statement of Claim is a binding legal document that demands an immediate, structured response.

Simultaneously, the lender will register a Certificate of Lis Pendens (CLP) against your property’s title. This serves as a public notice to any other creditors or potential buyers that the property is subject to active litigation. Understanding the difference between a default notice and formal claim is crucial, as the latter triggers irreversible legal timelines.

The Critical 20-Day Window: Why Time is Your Biggest Asset

The most critical number in the Alberta foreclosure process is 20. Under the Alberta Rules of Court, a defendant served with a Statement of Claim within the province has exactly 20 calendar days to file a response. If you are served outside Alberta but within Canada, the window extends to 1 month, and 2 months if served outside Canada.

“The 20-day response window is absolute. Failing to file a Statement of Defence or Demand of Notice essentially hands the keys to the lender without a fight,” says Sarah Jenkins, Senior Real Estate Counsel at the Alberta Legal Institute. “Many homeowners mistakenly believe informal negotiations pause the legal clock. In 2026, Alberta courts require formal filings regardless of ongoing bank discussions.”

If day 20 passes without a filed response, the lender’s legal counsel can file for a “Noting in Default.” This procedural move bars you from participating in future court hearings without special permission and paves the way for a default judgment. Once noted in default, you lose the right to challenge the lender’s accounting, dispute fees, or request an extended redemption period.

Step-by-Step: How to Formally Respond to the Court

Responding to a foreclosure action requires strict adherence to judicial procedures. Here is the step-by-step process for filing an appearance in Calgary or any other Alberta jurisdiction:

- Review the Claim Thoroughly: Examine the Statement of Claim for factual accuracy. Are the missed payment dates correct? Is the outstanding balance accurate? Note any discrepancies.

- Determine Your Response Type: Decide whether you will contest the facts (Statement of Defence) or simply request to be kept in the loop (Demand of Notice).

- Draft the Legal Forms: Obtain the correct forms from the Alberta Courts website. A Statement of Defence requires you to explicitly admit, deny, or claim no knowledge of each numbered paragraph in the lender’s claim.

- File at the Courthouse: Take the original and multiple copies of your drafted response to the Court of King’s Bench. You must pay a filing fee (approximately $50 in 2026) unless you qualify for a fee waiver.

- Serve the Plaintiff: The court will stamp your documents. You must then deliver a stamped copy to the lender’s lawyer at the address for service listed on the original Statement of Claim.

- Retain Proof of Service: Keep detailed records and an Affidavit of Service to prove you met the 20-day deadline.

Statement of Defence vs. Demand of Notice: Which Do You Need?

Choosing the right legal instrument is vital for your defense strategy. The two primary responses serve entirely different purposes in the litigation process.

| Feature | Statement of Defence | Demand of Notice |

|---|---|---|

| Purpose | To dispute the lender’s claims, facts, or legal right to foreclose. | To concede the default but demand notification of all future court steps. |

| When to Use | When there are accounting errors, improper service, or breaches of contract by the lender. | When you agree you are in default but want to monitor the process and protect your equity. |

| Legal Effect | Forces the lender to prove their case; can lead to a trial or summary judgment application. | Prevents the lender from proceeding in secret; ensures you can attend hearings regarding property valuation. |

Common Legal Defenses Against Foreclosure Actions in 2026

While a mortgage default is usually straightforward, lenders are not immune to administrative errors. “A well-documented Statement of Defence can force lenders back to the negotiating table, often resulting in modified payment terms that keep families in their homes,” explains David Chen, Director of the Canadian Homeowner Protection Alliance.

Valid legal defenses in Alberta may include:

- Accounting Inaccuracies: The lender has miscalculated the arrears, applied payments to the wrong account, or charged unauthorized fees.

- Improper Service: The lender failed to serve the Statement of Claim according to the strict rules outlined by the Law Society of Alberta.

- Statute of Limitations: In rare cases, if a lender waits too long to pursue a debt after the last payment or acknowledgment, the claim may be statute-barred.

- Failure to Mitigate: The lender unreasonably refused viable repayment plans or offers to purchase the property.

If you file a defence, you may eventually be required to participate in the foreclosure questioning process, a formal discovery phase where both parties answer questions under oath regarding the mortgage history.

The Redemption Period: Your Window to Save the Property

Even if you do not have a valid legal defence, Alberta law provides a built-in safety net known as the redemption period. Dictated by the Judicature Act of Alberta, this is a court-ordered timeframe during which you have the absolute right to pay the arrears (plus the lender’s legal costs) to reinstate the mortgage, or pay the entire mortgage balance to clear the title.

Research from the University of Calgary Property Law Review indicates that the standard redemption period in 2026 remains six months for residential properties. However, this is not guaranteed. Lenders frequently apply to the court to shorten this period to one day or one month if they can prove:

- The property has been abandoned.

- The property is falling into disrepair or is uninsured.

- There is little to no equity left in the home (the mortgage balance exceeds the property value).

Properly calculating your redemption period and defending against a lender’s attempt to shorten it is a critical component of your legal strategy. During this time, you can attempt to refinance, secure a second mortgage, or sell the property privately to extract your remaining equity.

Financial Implications: Legal Fees, Credit Scores, and Deficiency Judgments

The financial toll of a foreclosure extends far beyond the loss of the property. Once a Statement of Claim is filed, the meter starts running on legal costs. In 2026, average legal fees added to a homeowner’s mortgage balance during a standard foreclosure range from $3,500 to $5,000, escalating significantly if the matter goes to trial.

Furthermore, a completed foreclosure will remain on your Equifax and TransUnion credit reports for up to seven years, severely limiting your ability to secure future housing, loans, or even certain types of employment.

A unique aspect of Alberta real estate law involves the concept of non-recourse mortgages under the Law of Property Act. If you have a conventional mortgage (you put down 20% or more and do not have CMHC insurance), the lender generally cannot sue you for the shortfall if the property sells for less than the mortgage balance. However, if your mortgage is insured by CMHC, Sagen, or Canada Guaranty, the lender absolutely can pursue you for the difference. Understanding your deficiency judgment risks is paramount before deciding whether to fight or walk away.

Alternative Solutions: Voluntary Surrender and Private Sales

If retaining the home is financially impossible, proactive alternatives can mitigate the damage. While Americans often use the term “quit claim deed,” Alberta law utilizes a “voluntary transfer” or “voluntary surrender.”

“Voluntary surrender should be a last resort. Homeowners often leave thousands in equity on the table by not utilizing the standard six-month redemption period to sell the property themselves,” warns Elena Rostova, Chief Financial Analyst at the Western Canada Economic Bureau. Statistics show a 45% success rate in preserving equity when homeowners actively list their property during the redemption phase rather than waiting for a court-ordered sale.

If you successfully sell the property or refinance, your lawyer will work to pay off the lender and handle discharging a lis pendens from your title, officially ending the legal ordeal.

Navigating the Final Stages

If the redemption period expires without the mortgage being reinstated or the property being sold, the lender will apply for a Final Order for Foreclosure or an Order for Sale. The final order timeline moves quickly at this stage. The court will rely on an Affidavit of Value (usually an independent appraisal) to determine the property’s worth. If you filed a Demand of Notice, you have the right to review this appraisal and challenge it if you believe the lender is undervaluing your home to facilitate a quick sale.

Frequently Asked Questions (FAQ)

What happens immediately after receiving a statement of claim for foreclosure in Alberta?

Once served, the legal clock starts ticking, giving you exactly 20 calendar days to file a formal response (Statement of Defence or Demand of Notice) with the Court of King’s Bench. Failure to respond allows the lender to request a default judgment, which strips you of your right to defend against the foreclosure.

Can you stop foreclosure after the redemption period expires?

Once the redemption period ends, the lender typically applies for a final order to gain ownership or sell the property. However, if you can secure financing or a buyer before the judge signs the final order, courts will sometimes grant a last-minute extension to allow the transaction to close.

What defenses work against a foreclosure statement of claim?

Valid legal defenses include proving that mortgage payments were made but improperly credited, highlighting mathematical errors in the lender’s arrears calculation, or demonstrating that the lender failed to follow strict procedural rules for serving documents under Alberta law.

How long is the redemption period in Alberta foreclosures?

The standard redemption period in Alberta is six months for residential properties. During this window, you have the legal right to halt the foreclosure by paying the outstanding arrears and the lender’s legal costs, thereby reinstating the mortgage.

What if you ignore a foreclosure statement of claim?

Ignoring the claim results in a “Noting in Default,” meaning the court assumes you do not contest the lender’s allegations. The lender can then proceed to obtain a foreclosure order without your input, leading to your eviction and the loss of any remaining equity.

Does Alberta allow “quit claim” deeds to avoid foreclosure?

Alberta does not use the American “quit claim” process; instead, homeowners can negotiate a “voluntary transfer” or “voluntary surrender” with their lender. This transfers the property title back to the bank, though it may not erase the debt if you have an insured mortgage and the property value is less than what you owe.

Conclusion

Receiving a Statement of Claim for foreclosure is undoubtedly one of the most stressful experiences an Alberta homeowner can face. However, it is not the end of the road. By understanding the strict 20-day deadline, filing the appropriate legal responses, and leveraging the statutory redemption period, you can maintain control over your financial destiny. Whether your goal is to keep your home, negotiate a graceful exit, or protect your remaining equity, early intervention is your most powerful tool. Do not let the legal clock run out while you wait for a miracle. Contact us today to discuss your options and connect with professionals who can help you navigate Alberta’s complex foreclosure landscape.