Restructuring a subordinate property loan in Calgary involves replacing an existing secondary financing agreement with a new one to secure better interest rates, adjust repayment terms, or access additional home equity without altering the primary lending agreement. By leveraging accumulated property value, homeowners can consolidate high-interest debt, fund major renovations, or adapt to changing economic conditions while preserving the favorable terms of their first-position loan.

Key Takeaways

- Subordinate financing allows homeowners to preserve their original loan terms and rates while accessing up to 80% of their property’s appraised value.

- Restructuring your secondary debt can significantly lower monthly payments by consolidating high-interest unsecured liabilities into a single, secured payment.

- In 2026, lenders heavily weigh Loan-to-Value (LTV) ratios and Gross Debt Service (GDS) metrics when approving new financing terms.

- Properly timing your application with market interest rate shifts can save thousands of dollars over the lifespan of the loan.

- Working with local Calgary real estate and financial professionals ensures compliance with Alberta’s specific regulatory and legal frameworks.

The Mechanics of Subordinate Property Financing

Securing extra funds without altering your primary loan is a sophisticated strategy for property owners looking to maximize their financial leverage. This approach maintains your existing agreement while creating new avenues for capital deployment. In the dynamic 2026 Calgary housing market, understanding the hierarchy of property liens is crucial for making informed borrowing decisions.

A subordinate financing option uses your residence as collateral for additional borrowing. Unlike your original agreement, this loan holds a junior priority on your property title. In the event of a property sale or liquidation, the primary lender is compensated first. Because supplemental lenders assume greater risk due to this subordinate position, their qualification requirements and interest rate structures differ significantly from first-position loans.

Your primary and supplemental agreements coexist entirely independently. Each carries distinct rates, repayment schedules, and contractual conditions. This separation is the primary benefit of the strategy: it protects the favorable terms on your initial financing while enabling access to accumulated property value. For homeowners who locked in historically low rates on their primary residence years ago, avoiding a complete contract break is a financial necessity.

Calculating Your 2026 Home Equity Position

Understanding your property’s equity unlocks powerful financial opportunities. This accumulated value represents your true ownership stake, calculated by subtracting all existing loan balances from the current market worth of the property. It serves as the absolute foundation for strategic decisions about leveraging your residence’s financial potential.

Accurate valuation starts with professional appraisals and a rigorous analysis of recent neighborhood sales. According to recent data from the Alberta Real Estate Association, market trends significantly influence these figures, especially in rapidly developing urban quadrants of Calgary. In Canada, your maximum usable equity typically equals 80% of the appraised value minus any existing secured debts.

Consider a practical 2026 scenario: A Calgary property is appraised at $750,000. Under standard lending guidelines, 80% of this value is $600,000. If the homeowner currently holds a primary loan balance of $450,000, they have $150,000 in accessible equity available for subordinate financing. Principal reductions from consistent monthly payments gradually increase this available amount over time. Homeowners looking to accelerate this process often explore various principal reduction strategies to maximize their borrowing power.

Analyzing 2026 Interest Rates and Market Conditions

Financial decisions become substantially clearer when you grasp the underlying mechanics of borrowing costs. Interest rates directly impact your long-term payments, overall loan affordability, and the speed at which you build wealth. Calgary’s housing market presents unique opportunities to leverage favorable terms if you closely monitor macroeconomic indicators.

Supplemental financing options inherently carry higher rates than primary agreements due to the lender’s increased risk exposure. However, these rates typically remain vastly superior to unsecured credit products like credit cards or personal loans. When evaluating offers, borrowers must look beyond the advertised percentages. It is vital to consider administrative fees, repayment flexibility, and early termination penalty structures.

As Dr. Michael Chen, Chief Economist at the Canadian Real Estate Research Institute, explains: “Restructuring subordinate debt in a fluctuating rate environment allows homeowners to optimize their cash flow without sacrificing the historically low rates they may hold on their primary residence. The key is calculating the exact break-even point where interest savings outpace the administrative costs of the new loan.”

Borrowers must also be aware of the hidden costs of borrowing, as compounding frequency can silently increase the total debt burden over the loan’s lifecycle. Tools provided by the Bank of Canada help anticipate market shifts, allowing borrowers to choose between fixed and variable rate structures intelligently.

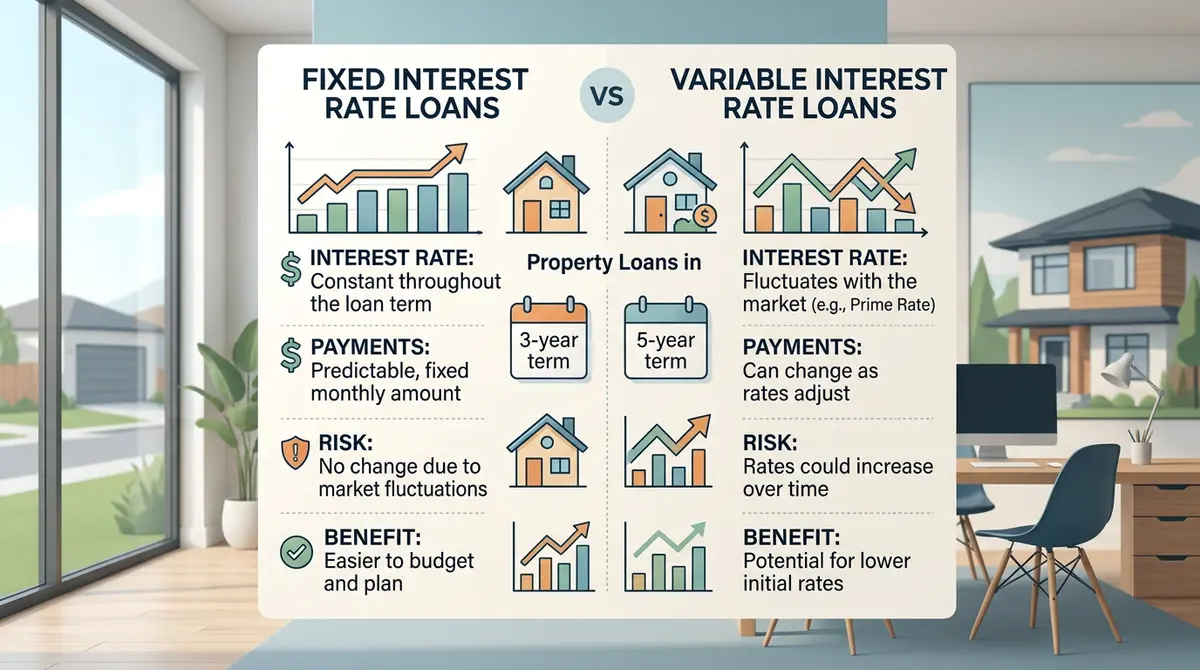

Comparing Financing Structures

| Financing Type | Interest Rate Structure | Repayment Flexibility | Best Use Case in 2026 |

|---|---|---|---|

| Fixed-Rate Subordinate Loan | Locked for the entire term (typically 1-5 years) | Predictable, fixed monthly payments | Long-term budgeting and debt consolidation |

| Variable-Rate Subordinate Loan | Fluctuates with the Bank of Canada prime rate | Payments may vary; potential for rapid principal paydown | Borrowers expecting interest rates to decline |

| Home Equity Line of Credit (HELOC) | Revolving credit, typically variable rate | Highly flexible; interest-only payment options | Ongoing renovation projects or emergency funds |

Step-by-Step Guide to Restructuring Your Loan

Optimizing your current lending arrangement requires methodical, strategic planning. Many property owners find immense value in reassessing their financial commitments when market conditions shift or personal financial goals evolve. Here is the definitive process for restructuring your supplemental loan agreement effectively in 2026.

- Evaluate Current Terms and Objectives: Review your existing agreement’s interest percentage, repayment timeline, and any associated prepayment penalties. Define precisely why you are restructuring—whether for debt consolidation, home improvements, or securing a lower rate.

- Calculate Your Available Equity: Obtain a preliminary estimate of your home’s current market value. Subtract your primary loan balance to determine your gross equity, keeping the 80% Loan-to-Value (LTV) maximum in mind.

- Gather Required Documentation: Lenders require comprehensive proof of financial stability. You will need recent pay stubs, T4 slips, Notice of Assessments (NOAs), a recent property tax bill, and statements for all existing debts. Utilizing a comprehensive document checklist for secondary financing ensures a smooth application process.

- Compare Lender Offers: Do not settle for the first offer. Compare terms from traditional banks, credit unions, and alternative lenders. Focus heavily on the Annual Percentage Rate (APR), which includes both the interest rate and all associated administrative fees.

- Finalize Appraisal and Legal Review: Once an offer is selected, the lender will mandate a professional property appraisal. Concurrently, you will need to engage a real estate lawyer to handle the title search, registration updates, and facilitate the disbursement of funds.

Strategic Benefits and Potential Drawbacks

What financial opportunities emerge when reviewing your property financing strategy? Calgary homeowners face a critical decision matrix when considering adjustments to their lending arrangements. Examining both sides of this financial equation is essential for long-term wealth preservation.

The primary benefit is the preservation of your original loan terms. If you secured a highly favorable rate on your primary residence years ago, breaking that contract could trigger early termination fees ranging from 3% to 6% of your remaining balance. By restructuring only the subordinate portion, you avoid these massive penalties. Furthermore, many homeowners utilize this strategy to evaluate cash-out refinancing alternatives, allowing them to extract capital for investments or business ventures.

However, potential drawbacks exist. Supplemental loans carry higher interest percentages than primary agreements. Legal fees, appraisal costs, and administrative charges might add $1,500 to $3,500 to your total expenses. Additionally, increasing your total debt load affects your debt-to-income ratio, potentially impacting future credit applications. According to the Financial Consumer Agency of Canada, borrowers must rigorously verify that new obligations align with their long-term financial capacity before committing to increased leverage.

Consolidating Debt and Managing Payments

Juggling multiple financial obligations can quickly become overwhelming, leading to missed payments and damaged credit scores. Strategic planning simplifies this process while unlocking substantial monthly savings. Aligning your property financing with other debts creates a clearer, more manageable path toward financial stability.

Rolling high-interest balances into your property financing drastically cuts borrowing costs. In 2026, standard credit card rates often exceed secured loan percentages by 12% to 18%. By consolidating these unsecured debts into a single subordinate loan, homeowners can reduce their monthly cash outflow by hundreds of dollars. This strategy frees up liquid capital for other priorities while simultaneously improving credit utilization ratios.

When leveraging home equity versus unsecured credit, the math heavily favors secured financing. However, Marcus Thorne, a Calgary-based certified financial planner, notes: “Borrowers often overlook the behavioral aspect of debt consolidation. Freeing up credit card limits is only beneficial if the homeowner commits to not running those balances back up. Discipline is the invisible requirement of successful debt restructuring.”

Navigating Alberta’s Regulatory Landscape

Navigating property financing adjustments requires acute awareness of both national lending standards and local provincial practices. Lenders evaluate applications through strict federal criteria, while Alberta’s specific regulations shape the legal obligations of all parties involved.

Legal requirements in Alberta mandate thorough title searches to confirm ownership and ensure no outstanding liens impede the new financing. Registration updates must be meticulously filed with the Alberta Land Titles Office. Furthermore, borrowers are often required to obtain Independent Legal Advice (ILA) to ensure they fully comprehend the terms and risks associated with subordinate financing.

According to data from Statistics Canada, over 28% of property owners in the province utilize some form of secondary financing. This high prevalence has led to robust consumer protection laws. For instance, understanding common law property rights and spousal consent requirements is mandatory under Alberta legislation before any new encumbrance can be registered against a primary residence.

Frequently Asked Questions

What is a subordinate property loan in Calgary?

A subordinate property loan is financing secured against your home’s accumulated equity that sits in second position behind your primary mortgage. It allows you to access capital for renovations, investments, or debt consolidation without altering the rate or terms of your first mortgage.

How does restructuring affect my primary lending agreement?

Restructuring a secondary loan operates entirely independently of your primary agreement. Your first mortgage’s interest rate, amortization schedule, and monthly payments remain completely unchanged, protecting any favorable terms you previously secured.

What is the maximum amount of equity I can access in 2026?

Under current Canadian lending guidelines, homeowners can typically borrow up to 80% of their property’s appraised market value, minus the outstanding balance of their primary mortgage. Some alternative lenders may offer slightly higher thresholds, though these come with significantly higher interest rates.

Are there penalties for paying off a subordinate loan early?

Yes, many lenders enforce prepayment penalties if you break the term early. These penalties usually amount to three months of interest or are calculated using an Interest Rate Differential (IRD), depending on whether the loan is fixed or variable.

Can self-employed individuals qualify for this type of financing?

Absolutely. While traditional banks may require extensive tax documentation, many alternative lenders in Calgary specialize in stated-income or alternative documentation loans specifically designed for self-employed professionals and business owners.

How long does the restructuring process typically take?

The entire process, from initial application to the final disbursement of funds, generally takes between two to four weeks. This timeline depends heavily on how quickly the property appraisal is completed and how fast the borrower provides the required documentation.

Conclusion

Restructuring your subordinate property financing in Calgary is a powerful financial maneuver when executed correctly. By understanding your true equity position, analyzing current 2026 market rates, and carefully navigating Alberta’s regulatory landscape, you can optimize your debt, lower your monthly payments, and achieve your broader financial objectives. Whether your goal is to consolidate high-interest credit cards or fund a major life event, leveraging your home’s value provides unparalleled flexibility.

However, the complexities of loan-to-value ratios, legal registrations, and lender negotiations require expert guidance to ensure you secure the most advantageous terms possible while avoiding hidden fees. If you are ready to explore your equity options and structure a plan tailored to your unique financial situation, professional assistance is just a click away. Contact our team today to schedule a comprehensive review of your property financing strategy.