A secondary mortgage is strategically viable when the return on the borrowed funds—such as eliminating 24% credit card debt or funding a high-ROI home renovation—outweighs the cost of the new loan’s interest rate. In Calgary’s 2026 real estate market, homeowners should consider tapping into their equity when they have accumulated at least 20% equity, possess stable income, and need capital without disturbing the favorable interest rate of their primary mortgage.

Key Takeaways

- Calgary homeowners must retain a minimum of 20% equity in their property after securing additional financing.

- Secondary financing preserves your primary mortgage’s interest rate and terms, avoiding costly breakage penalties.

- Consolidating unsecured debt (averaging 21% APR in 2026) into a single, lower-interest equity loan can save thousands annually.

- Home equity lines of credit (HELOCs) offer revolving access up to 65% of your home’s appraised value.

- Alternative lenders focus more heavily on property equity than traditional credit scores, providing options for self-employed Albertans.

- Strategic renovations, like basement suites, can yield a 75-90% return on investment in the current Calgary housing market.

Understanding Calgary’s 2026 Home Equity Landscape

The economic climate in Alberta has shifted significantly, making property equity one of the most powerful financial tools available to homeowners. With property values in many Calgary neighborhoods stabilizing after recent growth periods, the amount of accessible capital has increased for long-term residents. According to data from the Canada Mortgage and Housing Corporation (CMHC), the average Albertan homeowner now holds more accessible equity than at any point in the last decade.

Leveraging this built-up value requires a clear understanding of local lending practices. Unlike unsecured personal loans, equity-based solutions are secured against your physical property. This collateralization reduces the lender’s risk, which translates to lower borrowing costs for you. However, timing is everything. Accessing these funds during periods of stable employment and clear financial objectives ensures the debt serves as a stepping stone rather than a burden.

“Leveraging home equity is not about borrowing more money; it is about restructuring your existing financial obligations to improve cash flow,” explains Sarah Jenkins, Senior Financial Analyst at the Alberta Economic Institute. “In 2026, the most successful borrowers are those who use their homes to consolidate high-interest liabilities or invest in income-generating assets.”

What Exactly is Secondary Financing?

Unlocking the value of your home requires navigating layered financial products. A secondary loan allows you to borrow against the appraised value of your property while keeping your original home loan completely intact. This is a crucial distinction for homeowners who secured historically low rates on their first mortgages and do not want to trigger massive prepayment penalties by refinancing.

When comparing secondary financing to cash-out refinancing, the primary benefit is preservation. You maintain your current amortization schedule and interest rate on the bulk of your debt, only paying the current market rate on the newly borrowed amount.

Primary vs. Secondary Financing Mechanics

The term “secondary” refers strictly to the legal priority of the debt registered on your property title. Your original lender holds the first position. If a property is sold under duress, the first position lender is paid in full before the secondary lender receives any funds. Because of this subordinate position, secondary lenders take on slightly more risk.

To compensate for this increased risk, interest rates on subordinate debt are typically higher than prime mortgage rates. However, they remain significantly lower than unsecured credit cards or personal loans. Understanding this hierarchy is vital when evaluating your total cost of borrowing.

Strategic Timing: When Does Leveraging Equity Make Sense?

Financial decisions should never be made in a vacuum. For Calgary residents, deciding to borrow against property value should align with specific, measurable life goals. Here are the three most common scenarios where this strategy proves highly effective in 2026.

1. High-Interest Debt Consolidation

The most mathematically sound reason to access property value is to eliminate toxic debt. In 2026, the average retail credit card carries an annual percentage rate (APR) of 21% to 24%. Carrying a $20,000 balance at these rates can cost over $4,000 annually in interest alone. By leveraging home equity versus unsecured credit, homeowners can consolidate these balances into a single payment at a fraction of the interest rate.

This strategy immediately improves monthly cash flow and accelerates the timeline to becoming debt-free. Lenders look favorably upon debt consolidation applications because the new loan does not increase your overall debt load; it simply reorganizes it into a more manageable structure.

2. Value-Adding Property Renovations

Reinvesting in your primary residence is another excellent trigger for equity borrowing. However, not all renovations are created equal. In the competitive Calgary housing market, projects that add livable square footage or modernize essential spaces offer the best returns. Developing a legal basement suite, for instance, not only increases the property’s resale value by an estimated 75-90% of the project cost but also provides potential rental income to offset the loan payments.

Before funding a renovation, it is highly recommended to consult with local real estate professionals to ensure your planned upgrades align with neighborhood standards. Over-improving a property beyond what the local market can support is a common pitfall.

3. Business and Investment Opportunities

Many Albertan entrepreneurs use their homes to fund business expansion or bridge cash flow gaps. Traditional commercial loans can be notoriously difficult to secure, especially for newer enterprises. Accessing personal property value provides a fast, flexible injection of capital.

“Alternative lenders have revolutionized how self-employed Albertans access capital, focusing on the asset’s strength rather than traditional T4 income verification,” states Marcus Thorne, Chief Underwriter at Prairie Equity Solutions. For business owners, exploring stated income secondary financing options can bypass the rigid income tests required by major banks.

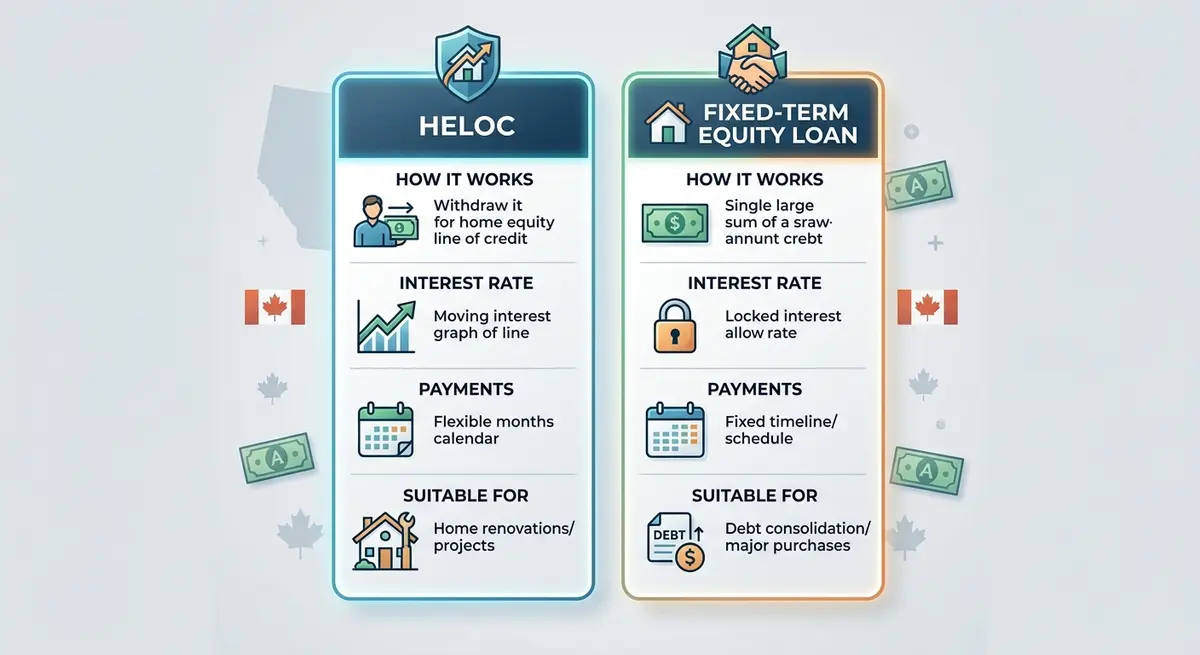

HELOC vs. Fixed-Term Equity Loans: A Comparison

Once you decide the timing is right, you must choose the appropriate financial vehicle. The Alberta market is dominated by two primary products: the Home Equity Line of Credit (HELOC) and the fixed-term lump sum loan. Each serves a distinct purpose.

A HELOC functions like a revolving credit card secured by your house. You are approved for a maximum limit (up to 65% of the home’s value) and only pay interest on the funds you actually draw. The interest rate is typically variable, fluctuating with the Bank of Canada’s prime rate. Conversely, a fixed-term loan provides a single lump sum upfront with a locked-in interest rate and a set repayment schedule spanning 5 to 25 years.

| Feature | HELOC (Revolving) | Fixed-Term Loan |

|---|---|---|

| Fund Disbursement | As needed, up to the credit limit | Single lump sum upfront |

| Interest Rate Type | Variable (tied to Prime) | Fixed for the duration of the term |

| Repayment Structure | Interest-only minimums allowed | Blended principal and interest payments |

| Best Used For | Ongoing renovations, emergency funds | Debt consolidation, single large purchases |

Step-by-Step: How to Evaluate Your Borrowing Position

Before approaching a lender, you need a realistic picture of your borrowing capacity. The Financial Consumer Agency of Canada (FCAC) mandates strict lending guidelines that all federally regulated institutions must follow. Here is how to calculate your standing:

- Determine Current Market Value: Obtain a professional appraisal or a comparative market analysis (CMA) from a local realtor. For example, assume your Calgary home is worth $600,000.

- Calculate the 80% Maximum LTV: Lenders typically allow you to borrow up to 80% of your home’s total value. Multiply $600,000 by 0.80 to get $480,000. This is your absolute maximum debt ceiling.

- Subtract Existing Mortgage Balances: Deduct your current primary mortgage balance from the maximum debt ceiling. If you owe $350,000, subtract that from $480,000.

- Identify Available Equity: In this scenario, you have $130,000 in accessible equity available for secondary financing.

- Assess Debt-to-Income (DTI): Calculate your total monthly debt obligations (including the projected new loan payment) divided by your gross monthly income. Most traditional lenders require a DTI below 40%.

Qualification Criteria for Alberta Homeowners in 2026

Meeting the mathematical equity requirements is only the first half of the equation. Lenders also scrutinize your ability to service the new debt. The qualification landscape in 2026 is divided into traditional and alternative channels, each with distinct criteria.

Credit Scores and Income Verification

Traditional banks and credit unions offer the lowest interest rates but demand pristine financial profiles. A credit score of 680 or higher is generally required to secure prime rates. Furthermore, these institutions require rigorous income verification, typically demanding two years of T4 slips and recent pay stubs.

If you are a business owner or contractor, verifying self-employed income can be challenging due to corporate write-offs that lower your personal taxable income. In these cases, traditional lenders may decline the application despite massive property equity.

Alternative Lending Options

This is where the alternative lending market steps in. Private lenders and Mortgage Investment Corporations (MICs) operate under different regulatory frameworks. They prioritize the asset (your home) over the borrower’s credit history. If you have substantial equity—often requiring 25% to 30% remaining in the home—alternative lenders will approve loans for individuals with credit scores as low as 550.

While the interest rates and setup fees are higher in the alternative space, these loans are designed as short-term solutions (typically 12 to 24 months). They provide immediate capital while you work on preparing your mortgage paperwork and rehabilitating your credit for an eventual transition back to a traditional bank.

Common Mistakes to Avoid When Tapping Home Equity

Even with sound timing and clear goals, borrowing against your home carries inherent risks. The most severe consequence of defaulting on secured debt is the potential loss of the property. Therefore, disciplined financial management is non-negotiable.

“The biggest mistake homeowners make is treating their property like an ATM rather than a strategic wealth-building tool,” warns Dr. Emily Carter, Professor of Economics at the University of Calgary. “Borrowing equity to fund depreciating assets, like luxury vehicles or vacations, actively destroys your net worth.”

Another frequent error is ignoring the long-term cost of interest. Borrowers often focus solely on the monthly payment rather than understanding how compounding frequency impacts your total debt over a 20-year amortization period. Always ask your lender for a complete amortization schedule and explore principal reduction strategies to pay off the loan faster than required.

Frequently Asked Questions (FAQ)

What is the minimum equity required to get a secondary loan in Calgary?

Most traditional and alternative lenders in Calgary require you to maintain at least 20% equity in your home. This means your total combined mortgage debt cannot exceed 80% of the property’s appraised market value.

Will taking out additional financing affect my current mortgage rate?

No. One of the primary benefits of subordinate financing is that it leaves your original mortgage completely untouched. You keep your existing interest rate, terms, and amortization schedule on the primary loan.

How long does the approval process take in Alberta?

Traditional bank approvals for HELOCs can take 2 to 4 weeks due to rigorous stress testing and income verification. Alternative and private lenders can often appraise the property and fund the loan within 5 to 10 business days.

Can I use the funds to pay off CRA tax arrears?

Yes. Many alternative lenders specialize in providing equity loans specifically to clear Canada Revenue Agency (CRA) tax debts. Traditional banks, however, will typically decline applications if there are outstanding tax arrears.

What are the typical closing costs involved?

Closing costs generally include a property appraisal ($300-$500), legal fees for registering the new mortgage ($1,000-$1,500), and potential broker or lender fees if using alternative financing. These costs can often be rolled into the total loan amount.

Is it better to choose a fixed or variable interest rate?

This depends on your risk tolerance and the current economic climate. Variable rates (often tied to HELOCs) offer flexibility and lower initial costs, while fixed rates provide payment certainty, protecting you against future Bank of Canada rate hikes.

Conclusion

Deciding when to leverage your property’s value is a significant financial milestone. In Calgary’s 2026 economic environment, utilizing secondary financing is a powerful strategy for consolidating high-interest debt, funding value-adding renovations, or injecting capital into a business. By understanding the strict Loan-to-Value limits, the differences between revolving credit and fixed-term loans, and the distinct qualification criteria of traditional versus alternative lenders, you can make an informed decision that protects your most valuable asset.

Navigating the complexities of subordination, appraisals, and lender fees doesn’t have to be overwhelming. If you are ready to explore your borrowing options and want a clear, transparent assessment of your property’s potential, expert guidance is just a click away. Contact us today to speak with a licensed Alberta lending specialist and discover the best equity solution for your unique financial goals.