Homeowners take out secondary financing to access accumulated property wealth in a lump sum without altering the favorable interest rate or terms of their primary home loan. This capital is primarily deployed for high-interest debt consolidation, value-adding property renovations, and funding significant life events like education or business expansion. By leveraging the property as collateral, borrowers secure significantly lower interest rates than unsecured credit options, transforming dormant equity into active financial leverage.

Key Takeaways

- Secondary financing allows you to access up to 80% of your home’s appraised value without touching your primary mortgage.

- Consolidating unsecured debt through property equity can reduce monthly interest obligations by an average of $300 to $800.

- Strategic home renovations funded by equity typically yield a 10% to 25% return on investment in the current housing market.

- Lenders evaluate approval based on loan-to-value (LTV) ratios, creditworthiness, and verifiable income streams.

- Secondary loans hold a subordinate lien position, meaning they carry slightly higher rates than first mortgages but remain cheaper than credit cards.

- Proper structuring of repayment terms is essential to mitigate the risks of equity depletion and potential default.

Understanding the Mechanics of Secondary Property Financing

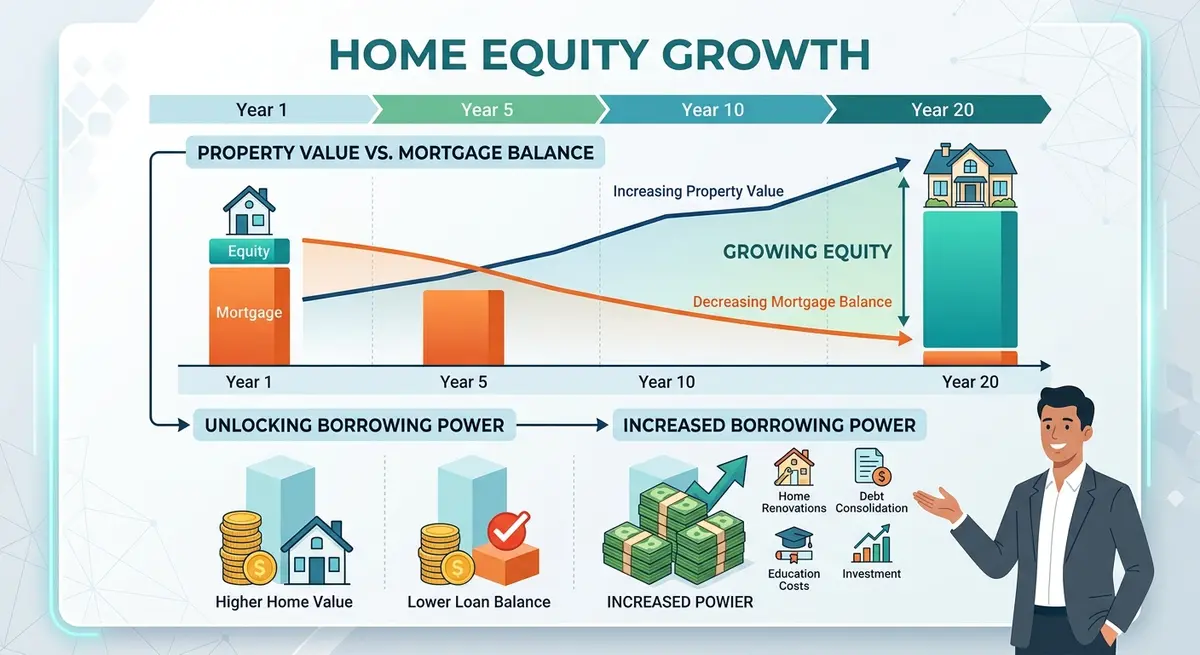

Your property’s growing value creates lucrative opportunities that extend far beyond your initial purchase agreement. Equity accumulates naturally as you make regular principal payments and as local real estate market values appreciate over time. This accumulated wealth forms the foundation for strategic borrowing solutions.

A secondary loan allows you to borrow directly against this equity while keeping your existing home loan completely intact. Unlike unsecured personal loans, this financial instrument uses your physical house as collateral. You receive a lump sum of funds based on the calculated difference between your home’s current appraised market value and your remaining primary mortgage balance.

Lenders prioritize repayment based on the order the loans were registered on the property title. According to Investopedia’s analysis of lien priority, your original mortgage remains in the first position for claims if financial difficulties arise. This subordinate structure means secondary lenders assume a higher degree of risk, which translates to interest rates that are slightly higher than primary mortgages but substantially lower than unsecured credit.

The Financial Mathematics: Why 2026 is the Year of Equity

Recent economic shifts have fundamentally changed how Canadians manage their household balance sheets. With the Bank of Canada maintaining specific monetary policies, preserving low fixed rates on primary mortgages has become a top priority for property owners. Refinancing an entire mortgage to access cash often means sacrificing a historically low rate for a higher current market rate.

As Sarah Jenkins, Senior Financial Analyst at the Canadian Equity Institute, explains: “Leveraging secondary financing allows homeowners to preserve their historically low primary mortgage rates while accessing necessary capital. It is the most mathematically sound approach to liquidity in the 2026 economic landscape.”

Data indicates that nearly 30% of Canadian homeowners actively explored equity-based borrowing options over the past year. This surge reflects a growing financial literacy regarding how property assets can unlock immediate financial flexibility. When comparing comparing secondary financing to cash-out refinancing, the math heavily favors leaving the primary loan untouched.

Strategic Applications for Your Property’s Wealth

Your home’s equity is not merely a static number on a balance sheet; it is a dynamic financial tool. Built through years of disciplined payments, this asset offers highly flexible solutions for immediate capital requirements.

Eradicating High-Interest Unsecured Debt

Managing multiple high-interest credit accounts is a significant drain on household wealth. The average Canadian carries over $21,000 in non-mortgage consumer debt, often spread across credit cards with interest rates peaking at 21.99%. Consolidating these balances through secured property financing is a proven wealth-preservation strategy.

By merging multiple high-interest payments into one predictable monthly plan, borrowers drastically reduce their blended interest rate. The Financial Consumer Agency of Canada notes that secured consolidation loans can accelerate debt payoff timelines by years. For many homeowners, leveraging home equity instead of unsecured credit frees up hundreds of dollars in monthly cash flow.

Funding High-ROI Property Improvements

Strategic renovations funded through equity can boost your property’s overall market value by 10% to 25%. Focusing on high-return upgrades like kitchen modernizations, bathroom additions, or legal basement suites delivers exceptional long-term value. These projects modernize your living space while simultaneously building future wealth.

Research from the Canada Mortgage and Housing Corporation (CMHC) indicates that secondary suites in particular offer dual benefits: increased property value and potential rental income. “The biggest mistake homeowners make is using high-interest unsecured credit for renovations when their property already holds the necessary wealth,” notes David Chen, Director of Lending at Alberta Financial Partners.

Capitalizing Business Ventures and Education

Life’s pivotal moments frequently require substantial funding that liquid savings alone cannot cover. Entrepreneurs often require rapid capital injections to scale operations or purchase inventory. Securing alternative financing for entrepreneurs through property equity provides faster access to larger sums than traditional commercial loans.

Similarly, funding post-secondary education or specialized career training represents an investment in future earning potential. Equity solutions provide immediate, lump-sum access to funds, allowing families to avoid the restrictive limits and variable terms of standard student lines of credit.

Comparative Analysis: Secondary Mortgages vs. Alternative Lending

Homeowners possess multiple avenues to access capital, each carrying unique structural benefits and drawbacks. Understanding how these financial instruments interact with your property’s value is critical for long-term stability.

| Feature | Secondary Mortgage | HELOC | Unsecured Personal Loan |

|---|---|---|---|

| Funding Structure | Single lump-sum disbursement | Revolving credit line | Single lump-sum disbursement |

| Interest Rate Type | Typically fixed rate | Variable rate (tied to prime) | Fixed, but significantly higher |

| Collateral Required | Yes (Property Equity) | Yes (Property Equity) | No |

| Best Use Case | Debt consolidation, major one-time costs | Ongoing, unpredictable expenses | Small emergencies under $20,000 |

The 2026 Qualification Framework for Alberta Homeowners

Securing additional property financing requires navigating specific lender criteria. Institutions must ensure borrowers maintain financial stability while leveraging their real estate assets. Here is the step-by-step process for qualification:

- Calculate Available Equity: Lenders typically allow borrowing up to 80% of your home’s appraised value, minus the outstanding balance of your primary mortgage. A professional appraisal is mandatory to establish current market value.

- Credit Profile Review: While secured loans are more forgiving than unsecured credit, your credit score dictates your interest rate tier. Scores above 680 unlock the most competitive institutional rates, while alternative lenders cater to scores below 620.

- Income Verification: You must demonstrate the capacity to service both mortgage payments simultaneously. Traditional employees provide T4s and pay stubs, while business owners must focus on verifying self-employed income through specialized documentation.

- Debt-to-Income (DTI) Assessment: Lenders calculate your total monthly debt obligations against your gross monthly income. The industry standard requires this ratio to remain below 43% to ensure sustainable repayment capacity.

- Document Assembly: Gathering paperwork proactively accelerates approval. Reviewing a comprehensive required documentation checklist ensures you have recent mortgage statements, tax records, and property insurance details ready.

Mitigating Risks: Protecting Your Primary Residence

Every financial decision carries potential consequences that demand rigorous evaluation. While accessing your property’s value offers immense flexibility, understanding the inherent trade-offs ensures you maintain control over your long-term economic stability.

Adding another monthly payment impacts your household budget immediately. You must account for this new obligation alongside existing utilities, property taxes, and unexpected maintenance costs. “In 2026, strategic debt consolidation through secured lending is the most effective shield against inflationary pressure, provided the borrower commits to strict budget adherence,” explains Dr. Marcus Thorne of the Calgary Economic Research Bureau.

The most severe risk is property loss. Missed payments on either the primary or secondary loan put your home at risk of legal action. If defaults occur, lenders can initiate legal proceedings. Understanding understanding foreclosure redemption periods is vital for any homeowner leveraging their property.

“Understanding lien priority is crucial; secondary lenders take on more risk, which is why transparency in the borrowing process is non-negotiable,” states Elena Rostova, a prominent Real Estate Attorney. To safeguard your investment, experts recommend implementing aggressive principal reduction strategies as soon as your cash flow improves.

Frequently Asked Questions

How does a secondary loan differ from a primary mortgage?

A secondary loan is secured against your property’s accumulated equity but sits in a subordinate lien position to your original mortgage. It operates entirely independently, featuring its own distinct interest rate, term length, and monthly payment schedule without requiring you to refinance your primary loan.

What are the mathematical advantages of using equity for debt consolidation?

Secured property loans typically offer interest rates that are 10% to 15% lower than standard credit cards or unsecured personal loans. By consolidating high-interest debts into a single secured payment, borrowers drastically reduce their monthly interest costs and accelerate their path to becoming debt-free.

Can I use equity financing to fund a business venture?

Yes. Because the loan is secured by your real estate asset, lenders place very few restrictions on how the disbursed funds are utilized. Many entrepreneurs use this capital to purchase inventory, fund expansions, or manage cash flow during seasonal business fluctuations.

What happens if property values decline after I secure the loan?

Your loan terms and balance remain unchanged even if the local real estate market experiences a downturn. However, a drop in property value reduces your remaining equity, which could limit your ability to refinance or sell the home profitably until market conditions recover.

How do credit inquiries impact my application?

While lenders require a hard credit pull to assess your risk profile, a single inquiry has a minimal and temporary impact on your overall score. It is highly recommended to work with a dedicated broker who can shop your profile to multiple lenders using a single credit report.

Is a HELOC better than a lump-sum equity loan?

It depends entirely on your capital deployment schedule. A HELOC is ideal for ongoing, phased projects where you only want to pay interest on the funds you actively draw. A lump-sum loan is superior for immediate, fixed costs like debt consolidation or a major single-phase renovation.

Conclusion

Leveraging your property’s equity through secondary financing is a powerful wealth management strategy in 2026. Whether your objective is to eliminate high-interest consumer debt, execute value-adding home renovations, or capitalize a new business venture, this financial instrument provides unparalleled access to affordable capital. By understanding the mechanics of lien priority, qualification requirements, and risk mitigation, you can transform your home from a simple residence into an active financial asset.

Navigating the complexities of property lending requires expert guidance to ensure you secure the most favorable terms while protecting your primary mortgage. If you are ready to explore how your property’s equity can serve your financial goals, contact our team today for a comprehensive, confidential assessment.