Co-signing a mortgage in Alberta legally binds you to 100% of the property’s debt, meaning if the primary borrower defaults, lenders will pursue you for the entire unpaid balance, accrued interest, and legal fees. A foreclosure will immediately devastate your credit score by up to 150 points, trigger potential wage garnishments, and severely restrict your future borrowing capacity for up to seven years. Because Alberta utilizes a judicial foreclosure process, co-signers remain financially exposed throughout a lengthy court procedure unless proactive legal and financial interventions are taken.

Key Takeaways

- Equal Liability: Co-signers are fully responsible for the entire mortgage balance, not just a portion of it.

- Immediate Credit Damage: A single missed payment impacts both the borrower’s and the co-signer’s credit reports equally.

- Asset Vulnerability: Lenders can target a co-signer’s personal savings, investments, and wages to recover deficiency judgments.

- Long-Term Consequences: A foreclosure notation remains on your Equifax and TransUnion credit reports for six to seven years.

- DTI Ratio Impact: The full mortgage amount is calculated into your debt-to-income ratio, often blocking your ability to secure personal loans or vehicle financing.

- Early Intervention is Crucial: Negotiating with lenders before a Statement of Claim is filed is the most effective way to mitigate financial damage.

The Legal Reality of Co-Signing a Mortgage in Alberta

Many Albertans mistakenly believe that adding their name to a family member’s or friend’s mortgage is merely a character reference or a temporary boost to help them qualify. In reality, Canadian mortgage contracts operate under the principle of joint and several liability. This legal doctrine stipulates that the financial institution can demand the full repayment of the debt from any party listed on the mortgage, regardless of who actually resides in the property or makes the monthly payments.

As David Chen, Lead Analyst at the Canadian Mortgage and Housing Corporation (CMHC), explains:

“Co-signing is not a character reference; it is a legally binding assumption of 100% of the debt risk. In 2026, we are seeing a significant rise in co-signers being caught off guard when primary borrowers face insolvency, suddenly realizing their own financial foundations are on the line.”

When a loan goes into arrears, the lender does not care about the personal agreements made between the borrower and the co-signer. Their primary objective is capital recovery. If the primary borrower loses their job or faces financial hardship, the lender will immediately look to the co-signer to make the account current. Understanding guarantor liability for mortgages is the first step in recognizing the gravity of this financial commitment.

Immediate Financial Consequences of a Missed Payment

The financial unraveling begins long before a judge issues a final foreclosure order. In Alberta, the consequences of a missed payment are swift and unforgiving. Most homeowners assume lenders jump straight to legal action after one missed payment, but the reality involves multiple checkpoints that systematically degrade your financial standing.

According to 2026 data from the Financial Consumer Agency of Canada (FCAC), approximately 62% of co-signers are unaware that a primary borrower has missed a payment until the lender initiates formal collection efforts. By this time, late fees have accrued, and the delinquency has already been reported to the credit bureaus.

The timeline typically unfolds as follows:

- Day 1-15: The payment is missed. The lender attempts to contact the primary borrower.

- Day 30: The missed payment is officially reported to Equifax and TransUnion, damaging both parties’ credit scores.

- Day 45-60: The lender issues a formal Demand Letter, requiring immediate payment of arrears plus administrative penalties.

- Day 90+: The lender transitions from administrative collection to legal action, filing a Statement of Claim in the Court of King’s Bench of Alberta.

It is vital to understand the distinction between early warning signs and formal legal action. Navigating the difference between a Notice of Default and a Statement of Claim dictates how much negotiating power you have left with the financial institution.

Foreclosure vs. Power of Sale: What Alberta Co-Signers Must Know

Property debt recovery varies drastically across Canadian provinces. While Ontario primarily utilizes the Power of Sale process, Alberta is a judicial foreclosure province. This distinction significantly alters the timeline, costs, and legal exposure for co-signers.

Dr. Emily Rostova, Professor of Property Law at the University of Calgary, notes:

“Alberta’s judicial foreclosure process provides a redemption period designed to protect homeowners, but for co-signers, this simply extends the duration of their financial exposure. A drawn-out court process means mounting legal fees, all of which are added to the total debt the co-signer is liable for.”

| Feature | Judicial Foreclosure (Alberta) | Power of Sale (e.g., Ontario) |

|---|---|---|

| Legal Oversight | Requires court approval at every step. | Administrative process; no court required. |

| Timeline | Lengthy (typically 12 to 24 months). | Rapid (often completed in 3 to 6 months). |

| Property Ownership | Title transfers to the lender upon Final Order. | Borrower retains title until the property is sold. |

| Co-Signer Stress | Prolonged exposure to accumulating legal fees. | Faster resolution, but less time to intervene. |

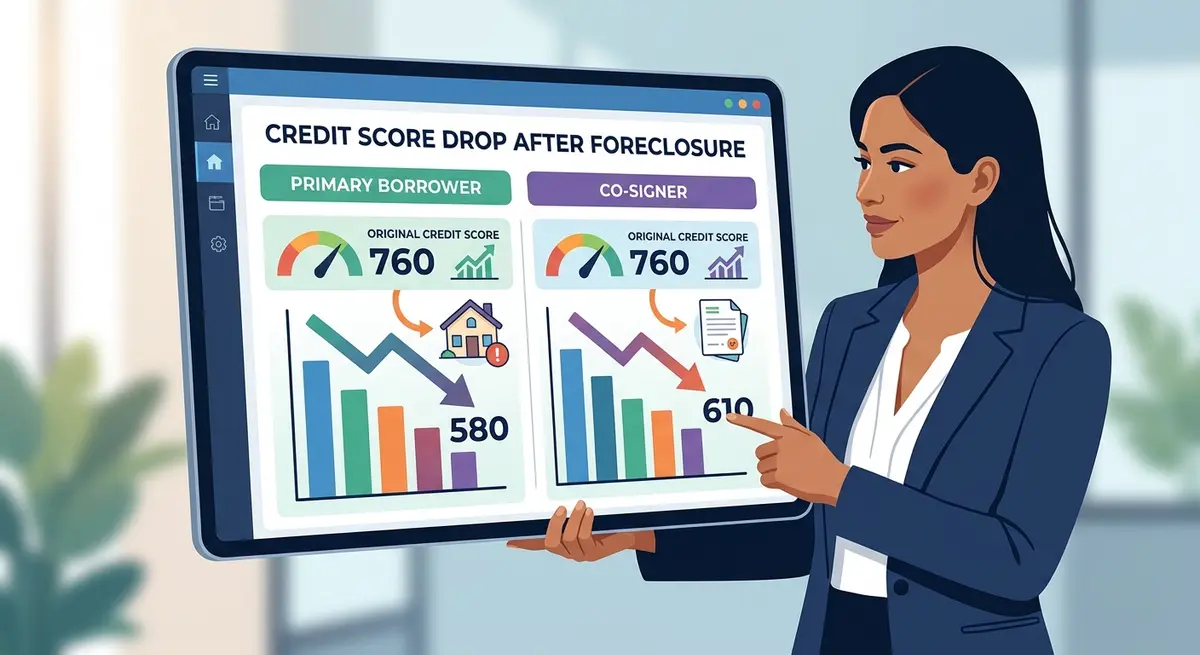

How Foreclosure Devastates a Co-Signer’s Credit Profile

Your credit health becomes shared property when you co-sign a mortgage. Because payment history accounts for 35% of your FICO score calculation, the primary borrower’s financial missteps become your permanent record.

As Marcus Thorne, Senior Credit Strategist at Equifax Canada, states:

“A foreclosure notation in 2026 will suppress a co-signer’s credit score by an average of 140 to 160 points within the first 60 days of default. Furthermore, this derogatory mark remains visible to future lenders for up to seven years, severely crippling borrowing capacity.”

Beyond the raw score drop, co-signers suffer from an artificially inflated Debt-to-Income (DTI) ratio. Lenders view the co-signed mortgage as your personal obligation. If the mortgage is $500,000, that entire amount counts against your borrowing limits. This instantly increases your DTI ratio, meaning new credit applications for car loans, credit cards, or your own primary residence may trigger automatic rejections. This credit entanglement is particularly dangerous in relationship breakdowns, highlighting how a divorced co-borrower can ruin your credit score if the property is not properly refinanced or sold.

The Alberta Foreclosure Process: A Step-by-Step Timeline

Understanding the sequence of legal events in Alberta empowers co-signers to take action before their options evaporate. The judicial process follows a strict, court-mandated pathway.

- Filing the Statement of Claim: The lender files a lawsuit in the Court of King’s Bench. Both the primary borrower and the co-signer are named as defendants. You have exactly 20 days to file a Statement of Defence or a Demand for Notice.

- The Redemption Order: If the court rules in favor of the lender, a judge will issue a Redemption Order. This grants the defendants a specific timeframe to pay the arrears and bring the mortgage into good standing. Understanding how Alberta foreclosure redemption periods are calculated is critical, as this is often the last window to save the property.

- Property Appraisal and Listing: During the redemption period, the court will order an independent appraisal to determine the fair market value of the home.

- Order for Sale: If the redemption period expires without payment, the court will order the property to be listed for sale, usually through a real estate agent chosen by the lender.

- Final Order of Foreclosure: If the property does not sell, or if the debt exceeds the property value, the lender may apply to take direct title to the home. Co-signers must be acutely aware of the final order of foreclosure timeline, as this represents the absolute termination of property rights.

Deficiency Judgments: When Losing the House Isn’t Enough

One of the most terrifying aspects of co-signing a mortgage in Alberta involves the concept of a deficiency judgment. If the court orders the sale of the property, and the sale price is not enough to cover the outstanding mortgage balance, accrued interest, and legal fees, a “deficiency” is created.

For conventional mortgages (where the down payment was 20% or more), Alberta’s Law of Property Act generally protects borrowers from deficiency judgments. However, this protection is highly nuanced. If the mortgage is insured by the CMHC, Sagen, or Canada Guaranty (meaning the down payment was less than 20%), the insurer will pay the lender the shortfall, but they will then subrogate the claim. This means the insurer will aggressively pursue both the borrower and the co-signer for the deficiency.

If a deficiency judgment is granted, the courts can authorize severe collection methods. This includes freezing your bank accounts, seizing non-exempt personal assets, and garnishing your wages. Co-signers must consult legal professionals to understand deficiency judgment calculations after foreclosure to accurately assess their financial exposure.

Strategic Defense: How Co-Signers Can Protect Themselves in 2026

Hope is not lost if a primary borrower begins missing payments. Co-signers have several strategic avenues to protect their credit and assets, provided they act swiftly.

1. Establish Open Communication with the Lender

Do not wait for the Statement of Claim. Contact the lender’s loss mitigation department immediately. Financial institutions prefer performing loans over costly legal battles. You may be able to negotiate a temporary forbearance, an interest-only payment period, or an extension of the amortization schedule to lower the monthly burden.

2. Cure the Default Personally

While frustrating, the most direct way to protect your credit is to make the missed payments yourself. Treat this as an emergency loan to the primary borrower. It is significantly cheaper to cover a few months of mortgage payments than to absorb a 150-point credit drop and thousands in foreclosure legal fees.

3. Force a Property Sale

If the primary borrower is permanently unable to afford the home, the most logical step is to sell the property voluntarily before the courts intervene. A traditional real estate sale preserves equity and avoids the stigma and cost of a judicial sale.

4. Explore Refinancing Options

If there is sufficient equity in the property, refinancing might provide a lifeline. You could consolidate other debts to lower the primary borrower’s overall monthly obligations. In some cases, exploring cash-out refinancing options can provide the liquidity needed to bring the mortgage current and stabilize the situation.

Frequently Asked Questions (FAQ)

How does being a co-signer affect my credit score if the borrower defaults?

If the primary borrower misses payments or faces foreclosure, it directly impacts your credit report equally. Late payments, defaults, and legal actions appear on your history, lowering your score by up to 150 points and severely affecting future loan approvals.

What immediate financial risks do co-signers face in Alberta?

You become 100% responsible for overdue payments, legal fees, and the remaining mortgage balance. Lenders can pursue you for repayment immediately, which strains your debt-to-income ratio and can lead to asset seizure or wage garnishment.

Can a foreclosure in Alberta impact my ability to get loans later?

Yes. A foreclosure notation stays on your Equifax and TransUnion credit reports for six to seven years. This makes traditional lenders highly hesitant to approve new mortgages, car loans, or personal lines of credit during that period.

How does foreclosure differ from a power of sale in Canada?

Foreclosure is a judicial process requiring court approvals at every stage, ultimately transferring property ownership to the lender. Power of sale is an administrative process that lets lenders sell the home faster without court orders, though the borrower retains title until the sale closes.

What steps do lenders take after missed mortgage payments?

Lenders typically issue a demand letter after 30 to 60 days of missed payments. If the arrears remain unresolved, they will file a Statement of Claim in the Alberta courts to initiate formal foreclosure proceedings.

How can co-signers protect their credit reports?

Monitor your credit report regularly using services like Equifax or TransUnion. If the primary borrower struggles, intervene early by negotiating payment plans with the lender, covering the shortfall yourself, or exploring refinancing options before legal action begins.

Does co-signing a mortgage affect my debt-to-income ratio?

Absolutely. The total loan amount counts toward your existing personal debts, drastically lowering your borrowing capacity. Lenders assess this ratio when approving new credit, and a high DTI will disqualify you from favorable interest rates.

What is a redemption order in Alberta’s foreclosure process?

A redemption order is a court mandate giving the borrower and co-signer a set period (often six months) to repay overdue amounts and reclaim the property. If the debt remains unpaid after this period, the court will order the property to be sold or transferred to the lender.

Conclusion

Co-signing a mortgage in Alberta is a profound financial commitment that carries severe risks if the primary borrower defaults. From immediate credit score devastation to the looming threat of deficiency judgments and wage garnishments, the consequences of foreclosure are far-reaching. The judicial foreclosure process in Alberta provides a window of opportunity through the redemption period, but relying on the courts is a costly and stressful strategy. Early intervention, open communication with lenders, and a clear understanding of your legal liabilities are your best defenses against financial ruin.

If you are a co-signer facing potential default, or if you need to explore alternative financing strategies to save your property, do not wait for a Statement of Claim to arrive in the mail. Professional guidance can help you navigate these complex legal and financial waters. Get in touch with our team today to discuss your options and protect your financial future.