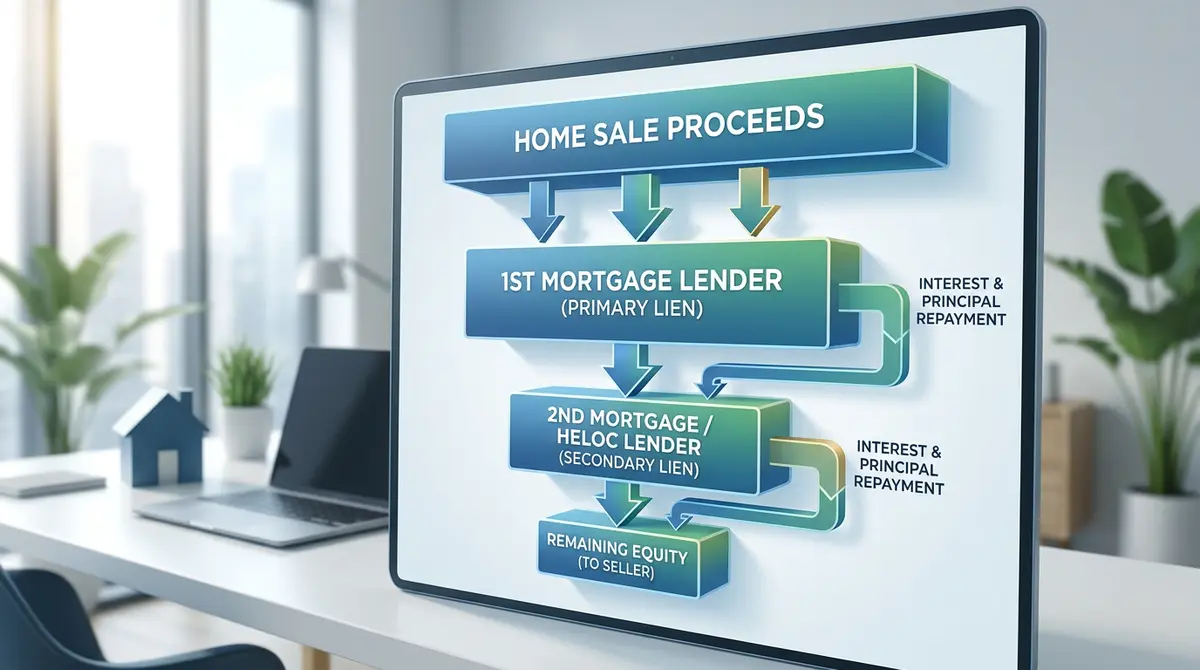

When you sell a property in Calgary, the proceeds from the sale are legally required to pay off your primary mortgage first, followed immediately by your second mortgage or home equity line of credit (HELOC). If your home’s sale price exceeds the combined total of both debts, the remaining equity is transferred to you as profit. However, if the local market has dipped and the sale proceeds cannot cover the secondary loan, you remain legally responsible for the shortfall and must negotiate a repayment plan or settle the balance out of pocket.

Key Takeaways

- Lien Priority Dictates Payouts: Primary lenders hold senior lien priority and are always paid first from sale proceeds.

- Automatic Discharges: Real estate lawyers handle the automatic payout and discharge of both mortgages during the closing process.

- Shortfall Responsibility: If sale proceeds fall short, the secondary mortgage balance becomes an unsecured debt that you must still repay.

- Prepayment Penalties Apply: Paying off a secondary loan early often triggers a 3-month interest penalty or an Interest Rate Differential (IRD) fee.

- Porting Options: In some cases, you may be able to port your secondary financing to a new property to avoid discharge fees.

The Mortgage Hierarchy: Who Gets Paid First?

Understanding the legal hierarchy of property debt is crucial when preparing for a sale. In Alberta, mortgages are registered on your property title in chronological order. The first mortgage registered holds “first position” or senior lien priority. Any subsequent financing, such as a home equity loan or HELOC, sits in “second position” as a subordinate lien.

During a property disposition, the Real Estate Council of Alberta (RECA) mandates a strict distribution of funds. Your real estate lawyer receives the buyer’s funds in trust. From this pool, they first pay real estate commissions and legal fees, then clear the primary mortgage balance. Only after the primary lender is fully satisfied do the remaining funds flow to the secondary lender. This structural hierarchy is exactly why secondary financing carries higher interest rates—the lender assumes a higher risk of not being fully compensated if property values decline.

Calculating Your Calgary Home Equity in 2026

Your home’s equity is the true measure of your financial leverage. To calculate your available equity, subtract the combined balances of your primary and secondary mortgages from the current market value of your home. According to the Calgary Real Estate Board (CREB) 2026 market forecast, average detached home prices have stabilized at $745,000. If you owe $400,000 on your first mortgage and $100,000 on your second, your gross equity stands at $245,000.

However, gross equity is not net profit. You must account for closing costs, which typically consume 4% to 6% of the sale price. Data from Statistics Canada indicates that 22% of Alberta homeowners carry secondary financing, making accurate equity calculations a widespread necessity. Regularly reviewing your principal reduction strategies can help maximize the funds available to you at closing.

Scenario 1: Sufficient Equity to Clear All Debt

In a healthy real estate market, most homeowners experience the ideal scenario: the sale price comfortably covers all outstanding property debts, closing costs, and penalties. When this happens, the transaction proceeds seamlessly. Your lawyer requests a “payout statement” from both lenders, which details the exact amount required to discharge the loans on the closing date.

Once the funds are distributed and the lenders are paid, they issue a discharge document. This legal document is filed with the Alberta Land Titles Office, officially removing the liens from your property. The remaining balance is then deposited directly into your bank account. It is highly recommended to focus on retaining your mortgage documents even after the sale is complete, as proof of discharge is vital for future financial endeavors.

Scenario 2: Dealing with a Mortgage Shortfall

Market volatility can sometimes leave homeowners “underwater,” meaning the home’s value is less than the total debt secured against it. If your sale proceeds cover the first mortgage but only partially cover the second, you face a shortfall. Because the secondary lender’s lien must be removed for the sale to close, you cannot simply ignore the remaining balance.

As Sarah Jenkins, Senior Real Estate Attorney at Alberta Legal Partners, explains: “Secondary lenders are acutely aware of their subordinate position. In a shortfall scenario, proactive communication often yields favorable settlement terms rather than forced litigation.”

Homeowners in this situation have a few options. You can pay the difference out of pocket using savings, or you can negotiate with the secondary lender to convert the remaining balance into an unsecured personal loan. If the lender refuses to discharge the mortgage without full payment, the sale could collapse. Understanding deficiency judgment calculations is critical if you are forced to sell under financial duress.

Navigating Prepayment Penalties and Discharge Fees

Selling your home before your mortgage term expires almost always triggers prepayment penalties. Because secondary loans often have shorter terms (typically 1 to 5 years), breaking them early can be costly. The Financial Consumer Agency of Canada requires lenders to clearly outline these fees in your contract.

For fixed-rate secondary mortgages, lenders usually charge the greater of three months’ interest or the Interest Rate Differential (IRD). For variable-rate mortgages, the penalty is almost universally three months of interest. Additionally, lenders charge administrative fees to physically remove their claim from your property title.

| Fee Type | Typical Cost in Alberta (2026) | Description |

|---|---|---|

| Discharge Fee | $250 – $400 per mortgage | Administrative cost to remove the lien from the provincial property title. |

| Prepayment Penalty (Variable) | 3 Months Interest | Standard penalty for breaking a variable-rate secondary loan early. |

| Prepayment Penalty (Fixed) | Greater of 3 Months Interest or IRD | Compensates the lender for lost interest income over the remaining term. |

| Legal Fees | $1,200 – $1,800 | Lawyer fees for handling the trust funds and executing the payouts. |

It is important to understand how compounding frequency impacts your final payout amount, as daily compounding can slightly inflate the final balance required on closing day.

Step-by-Step Guide: Selling a Home with Multiple Mortgages

To ensure a smooth transaction and protect your financial interests, follow this structured approach when listing a property encumbered by multiple loans:

- Request Payout Statements: Contact both your primary and secondary lenders to request preliminary payout statements. This will give you the exact figures required to clear your debt, including estimated penalties.

- Calculate Net Proceeds: Work with your real estate agent to estimate your home’s selling price. Deduct the payout amounts, real estate commissions (typically 7% on the first $100,000 and 3% on the balance in Alberta), and legal fees.

- Assess Shortfall Risks: If your net proceeds are negative, immediately consult a financial advisor to explore unsecured loan conversions or out-of-pocket settlement options.

- Hire a Real Estate Lawyer: Engage a lawyer early in the process. They will coordinate with both lenders to ensure the liens are discharged simultaneously upon closing.

- Review Porting Options: If you are buying a new home, ask your secondary lender if you can port the mortgage to the new property to avoid prepayment penalties.

Bridge Loans and Mortgage Portability

If you are purchasing a new home before the sale of your current home closes, you may need to navigate overlapping transactions. This is where bridge financing becomes invaluable. A bridge loan uses the equity in your current home to fund the down payment on your new property for a short period (usually 30 to 90 days).

According to David Chen, a Calgary-based mortgage broker: “In 2026, we are seeing more homeowners utilize bridge financing to protect their equity while navigating overlapping closing dates, especially when dealing with the complexities of secondary liens.”

Alternatively, some lenders allow you to “port” your secondary mortgage. Porting transfers your existing mortgage rate, terms, and balance to your new property. This strategy effectively bypasses prepayment penalties and is highly recommended if you secured a favorable interest rate prior to recent market shifts. If porting isn’t an option, you might want to compare your situation against cash-out refinancing options on the new property.

Alberta Real Estate Regulations Governing Property Sales

Alberta’s regulatory framework provides specific protections for both buyers and sellers during property transactions. When a property is sold, the seller is legally obligated to provide clear title to the buyer. This means all financial encumbrances, including primary mortgages, secondary mortgages, and builder’s liens, must be discharged.

Dr. Emily Carter, an economist at the University of Calgary, notes: “The 2026 housing inventory constraints have artificially inflated secondary lien recovery rates, benefiting homeowners who purchased prior to 2022 by ensuring sufficient equity to clear all registered debts.”

If a homeowner attempts to sell a property without disclosing a secondary lien, the transaction will be halted by the buyer’s lawyer during the title search phase. Furthermore, if the property is tied up in a marital dispute, you may need to pay out a partner and clear your title before the sale can legally proceed. In extreme cases of default prior to sale, understanding foreclosure redemption periods is vital to maintaining control over the sale process.

Frequently Asked Questions

Can I sell my house if my second mortgage is in default?

Yes, you can sell your house while in default, provided the lender has not yet finalized foreclosure proceedings. Selling voluntarily is often the best way to pay off the debt and avoid severe damage to your credit score, though the lender must agree to the payout terms.

Does the buyer take over my second mortgage?

No. In almost all residential real estate transactions in Alberta, the seller’s mortgages are paid off and discharged using the sale proceeds. The buyer secures their own financing and receives a clear property title.

What happens if I don’t have enough money to pay off the second mortgage?

If the sale proceeds fall short, the remaining balance does not disappear. You must either pay the difference out of pocket on closing day or negotiate with the lender to convert the remaining balance into an unsecured personal loan or promissory note.

Will my second mortgage lender stop the sale of my house?

A secondary lender cannot easily stop a sale if the primary lender is initiating it or if the sale price represents fair market value. However, they can refuse to discharge their lien if you do not provide a satisfactory plan to repay the outstanding balance, which can delay closing.

Are discharge fees negotiable?

Generally, discharge fees are fixed administrative costs outlined in your original mortgage contract and are not negotiable. However, prepayment penalties (like the IRD) can sometimes be negotiated or waived if you are porting the mortgage or securing a new loan with the same lender.

Conclusion

Selling a house with multiple mortgages in Calgary requires careful financial planning and a clear understanding of lien priority. By accurately calculating your equity, anticipating prepayment penalties, and working closely with a real estate lawyer, you can navigate the payout process smoothly. Whether you are dealing with a surplus of equity or managing a potential shortfall, proactive communication with your lenders is the key to a successful transaction.

If you are feeling overwhelmed by the complexities of property debt or need professional guidance on managing your secondary financing during a sale, contact our team today. We specialize in helping Calgary homeowners structure effective exit strategies and protect their hard-earned equity.