When the Canada Revenue Agency registers a tax lien against your property, it can feel like your financial future has been locked down. However, a second mortgage can be an effective tool to discharge that lien and regain control of your real estate assets. By accessing the equity in your home, you can pay off the CRA’s claim, stop accumulating interest penalties, and avoid more severe enforcement measures like seizure or forced sale. This guide walks you through exactly how this process works, when it makes sense, and what pitfalls to watch for.

- A CRA property lien is a government claim registered against your real estate for unpaid taxes, giving the agency legal rights to recover debts from property sales or refinances

- Second mortgages allow you to borrow against your home’s equity to pay off tax debts and discharge the lien, often at lower interest rates than CRA penalties

- The process typically takes 2-6 weeks and requires lender approval based on your creditworthiness and property value

- Alberta homeowners should understand both provincial and federal tax obligations that can trigger liens

- Failure to address a CRA lien can result in wage garnishment, bank levies, or forced property seizure

- Alternatives include installment agreements, taxpayer relief programs, or selling the property outright

- Working with mortgage professionals and tax advisors simultaneously is essential for a successful resolution

Understanding CRA Property Liens: What Homeowners Need to Know

A property lien registered by the Canada Revenue Agency is a legal claim against your real estate that secures payment of outstanding tax obligations. Unlike a mortgage registered at the land titles office—which you voluntarily agree to when borrowing—a tax lien is imposed by the government when you fail to pay amounts owed after formal demand. According to the Canada Revenue Agency’s technical publications, liens can be registered for unpaid income taxes, GST/HST debts, Canada Pension Plan contributions, or employment insurance premiums.

The CRA has broad powers under the Income Tax Act and Excise Tax Act to collect debts. Once a lien is registered at your provincial land titles office, it appears on your property’s title, effectively preventing you from refinancing or selling without satisfying the debt first. Research from the Fraser Institute indicates that tax collection enforcement actions in Canada increased by approximately 23% between 2020 and 2025, making understanding these mechanisms more critical than ever for property owners.

In Alberta specifically, the Land Titles Act governs how federal liens are registered and prioritized. A CRA lien typically ranks behind existing mortgages and encumbrances but ahead of most other creditors. This means if you sell your property, the CRA gets paid from the proceeds before many other claimants. The lien remains registered until the debt is paid in full, plus accumulated interest and any applicable penalties.

How Second Mortgages Work in the Context of Tax Liens

A second mortgage is a loan that uses your property as collateral, sitting behind your existing first mortgage in priority. If you already have a primary mortgage, any additional borrowing secured by the same property becomes a second charge. When the proceeds from a second mortgage are used specifically to pay off a CRA lien, you’re essentially refinancing your way out of the government’s claim.

The process works because second mortgage lenders focus primarily on the property’s value and your equity position rather than the lien itself. Once the second mortgage funds, you can use those proceeds to pay the CRA in full, at which point the agency issues a Certificate of Discharge or Release of Lien. You then register the second mortgage at land titles, effectively taking the place of the CRA’s claim.

Interest rates on second mortgages are typically higher than first mortgage rates, but they remain substantially lower than the compounded penalties the CRA charges on outstanding balances. The CRA’s prescribed interest rate for overdue taxes compounds monthly, meaning unpaid balances can grow significantly over time. A second mortgage at 8-12% annually often costs less than the CRA’s accumulated penalties over a multi-year period.

When Using a Second Mortgage for CRA Liens Makes Sense

This strategy isn’t right for everyone, but certain situations make it particularly effective. You should consider a second mortgage to address CRA liens when you have sufficient equity in your property—generally at least 15-20% of the home’s current market value—to qualify for a loan large enough to cover the tax debt plus closing costs. If your first mortgage balance plus the proposed second mortgage stays below 80% of the property value, you’ll have access to better rates and terms.

Homeowners facing immediate enforcement actions, such as a Notice of Assessment indicating the CRA intends to garnish wages or levy bank accounts, often benefit from acting quickly with a second mortgage. The threat of losing access to your bank accounts or having wages reduced makes the certainty of a second mortgage preferable to waiting for installment arrangements that may never be approved.

Additionally, if you have a strong income stream but poor credit history, second mortgage lenders may be more willing to work with you than traditional banks. Many private and alternative lenders focus on property equity over credit scores. As mortgage broker Sarah Mitchell, principal at Calgary Equity Mortgages, explains: “We’ve helped numerous clients use second mortgages to resolve tax liens. The key is acting before the CRA escalates to seizure proceedings—once that happens, options narrow dramatically.”

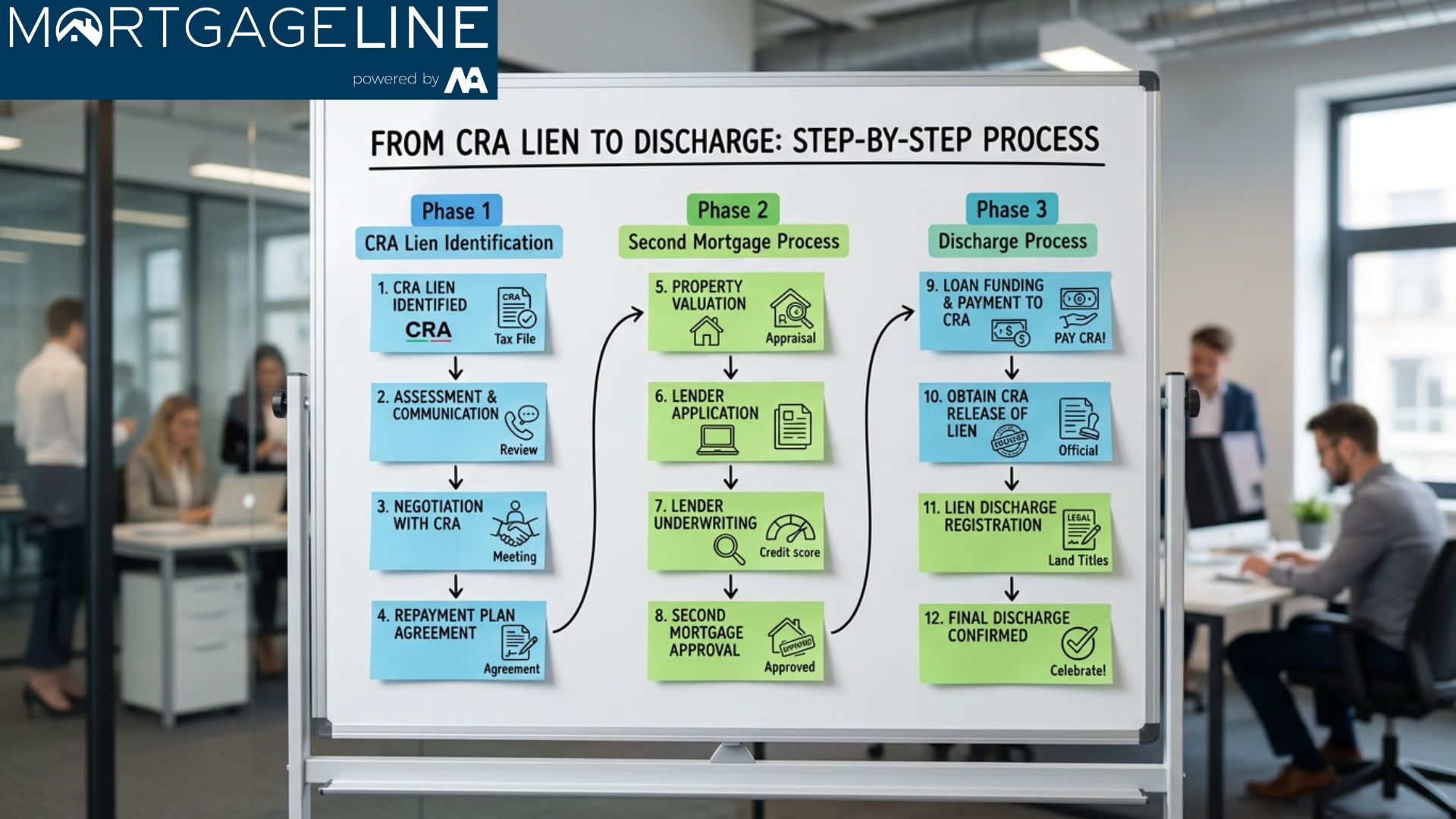

Step-by-Step Process: Getting a Second Mortgage to Discharge Your CRA Lien

The following steps outline the typical path from identifying a CRA lien to successfully discharging it through a second mortgage:

- Obtain a tax clearance search: Request a certified copy of the lien from your provincial land titles office to confirm the exact amount owed, including accumulated interest and penalties to date.

- Contact the CRA directly: Call the collections department to verify the debt balance and discuss payment options. Get a reference number and document all communications in writing.

- Assess your property equity: Get an appraisal or use a comparative market analysis to determine your home’s current value. Calculate your loan-to-value ratio by subtracting your first mortgage balance from the property value.

- Shop second mortgage lenders: Compare offers from banks, credit unions, and private lenders. Focus on those experienced with tax lien discharges in Alberta.

- Submit your application: Provide required documentation including property appraisal, mortgage statements, proof of income, tax returns, and CRA correspondence.

- Review and sign loan documents: Once approved, carefully review terms, rates, fees, and prepayment options before signing.

- Fund and pay the CRA: On closing day, the lender wires funds, and your lawyer or notary uses proceeds to pay the CRA directly.

- Obtain lien discharge: The CRA typically issues a Release of Lien within 10-15 business days after payment. Your lawyer registers the second mortgage at land titles.

- Keep records: Maintain copies of the lien release, mortgage documents, and all CRA correspondence indefinitely for tax purposes.

Comparing Your Options: Second Mortgage vs. Other Approaches

Before committing to a second mortgage, homeowners should understand the full range of alternatives available for addressing CRA tax liens. Each approach has distinct advantages and drawbacks depending on your financial situation, timeline, and long-term goals.

| Approach | Pros | Cons | Best For |

|---|---|---|---|

| Second Mortgage | Quick resolution, stops interest accumulation, preserves property ownership | Higher interest than first mortgage, adds another payment obligation | Homeowners with significant equity and stable income |

| CRA Installment Agreement | No new debt, preserves credit score | Interest continues accruing, may take years to pay off | Those with smaller debts who can afford modest monthly payments |

| Taxpayer Relief Program | Can reduce penalties and interest, potential principal reduction | Strict eligibility criteria, lengthy application process | Those experiencing financial hardship due to circumstances beyond control |

| Home Equity Line of Credit | Flexible borrowing, potentially lower rates than second mortgage | Requires good credit, may not cover full lien amount | Homeowners with strong credit and smaller tax debts |

| Property Sale | Eliminates all debts, clean slate | Loses property, may owe capital gains tax, relocation costs | Those unable to service any mortgage debt or who want to move anyway |

As tax specialist Michael Chen, CPA and partner at Chen & Associates in Calgary, notes: “Many clients don’t realize the CRA’s Taxpayer Relief provisions exist. If you’ve experienced illness, job loss, or other circumstances beyond your control, you may qualify to have penalties waived or reduced. However, the application takes 8-12 weeks minimum, so this isn’t an option when facing imminent seizure.”

Risks and Considerations Before Proceeding

While using a second mortgage to discharge a CRA lien can be highly effective, it introduces new financial obligations that must be carefully considered. The most significant risk is compounding your debt—you’re essentially replacing one debt (taxes owed) with another (mortgage debt) that must be repaid regardless of future circumstances.

Second mortgage lenders in Alberta typically charge origination fees of 1-3% of the loan amount, plus legal fees and land titles registration costs. These closing costs can add $3,000-$8,000 to the total expense, which should be factored into your comparison against simply paying the CRA over time. Additionally, some second mortgages carry prepayment penalties or balloon payment requirements that could catch unwary borrowers off guard.

There’s also the risk that your first mortgage contains a due-on-sale clause or other restrictions that could be triggered by registering a second mortgage. Review your existing mortgage documents carefully, or ask your lawyer to review them before proceeding. Some lenders may also charge fees for subordinate financing, though this is more common with certain institutional first mortgages.

Perhaps most importantly, if your underlying financial problems that caused the CRA debt aren’t addressed, you could find yourself with a second mortgage payment you can’t afford and new tax obligations building up again. Consider whether the second mortgage solves the symptom (the lien) without fixing the root cause (inadequate cash flow, business losses, or spending habits).

Working with Professionals: Building Your Support Team

Successfully navigating a CRA lien discharge through a second mortgage requires coordinating multiple professionals who specialize in different aspects of the problem. Attempting to handle this alone significantly increases the risk of mistakes that could cost you time, money, or even your property.

Your mortgage professional—whether a broker or lender—will help you find the best second mortgage terms for your situation. Look for someone experienced specifically with tax lien discharges in Alberta, as the process differs from standard refinances. They should understand how to structure the transaction so funds flow correctly to the CRA on closing day.

Your real estate lawyer or notary handles the legal aspects: reviewing title, preparing mortgage documents, coordinating with the CRA’s legal department, and ensuring the lien is properly discharged. This is not optional—even if using a lender’s in-house lawyer, you should have independent legal advice to protect your interests.

Finally, consider engaging a tax accountant or CPA who can help you understand why the tax debt occurred and whether any relief provisions apply. They can also advise on tax implications of the second mortgage itself—interest paid on a mortgage used for business purposes may be deductible, while personal residence interest typically is not.

For related guidance, explore our articles on using second mortgages to pay CRA tax arrears and home equity options after consumer proposals.

Conclusion

A CRA property lien doesn’t have to be the end of your property ownership or financial stability. By strategically using a second mortgage to access your home’s equity, you can discharge the government’s claim, stop accumulating interest penalties, and regain control of your real estate. The key is acting decisively before enforcement escalates, understanding all your options, and assembling the right professional team to guide you through the process.

If you’re facing a CRA lien and want to explore whether a second mortgage makes sense for your situation, the best first step is a no-obligation consultation with an experienced mortgage broker. They can review your equity position, explain available options, and help you understand the costs and timeline involved. Don’t wait until the CRA begins seizure proceedings—proactive homeowners have far more options available than reactive ones.

Browse our complete resource library for more guidance on home equity financing strategies, or learn about the importance of independent legal advice before signing any mortgage documents.

Frequently Asked Questions

How long does a CRA property lien stay on my record after I pay it off?

Once the CRA receives full payment, they typically issue a Release of Lien within 10-15 business days. The release should be registered at your provincial land titles office to remove the lien from your property title. While the debt is considered satisfied, the CRA may note the original assessment on your account for their records, though this doesn’t appear on credit reports or title searches once discharged.

Can I get a second mortgage if I already have a consumer proposal or bankruptcy?

Yes, it’s possible but more challenging. Second mortgage lenders typically require you to be discharged from any consumer proposal or bankruptcy before they’ll consider your application. Some alternative lenders specialize in these situations and may approve applications 12-24 months post-discharge, depending on other factors like equity position and income stability. Our article on early consumer proposal discharge and home equity covers this topic in detail.

What happens if I can’t afford the second mortgage payment after paying off the CRA lien?

This is a serious risk that should be modeled before proceeding. If you default on a second mortgage, the lender can initiate foreclosure proceedings similar to a first mortgage. However, second mortgage lenders are often more willing to work with borrowers on payment arrangements before foreclosing, since they’d need to satisfy the first mortgage holder’s position first in any sale. Consider whether your income is stable enough to service additional debt before committing.

Does the CRA automatically discharge the lien once I pay them?

No, you must request the discharge in writing and provide proof of payment. After receiving funds, the CRA processes the payment and issues a Certificate of Discharge or Release of Lien. Your lawyer typically handles this process as part of the closing, but you should follow up to confirm the release is registered at land titles. Without proper registration, the lien technically remains on title.

Can I negotiate the amount the CRA accepts to release the lien?

Under the Taxpayer Relief provisions, the CRA has limited authority to cancel penalties and interest, but they generally cannot reduce the actual principal tax debt owed. However, if you’re facing financial hardship, they may accept a payment arrangement that spreads the debt over time without requiring a second mortgage. The CRA rarely negotiates the principal balance itself, but their prescribed interest rate may be reduced in certain circumstances.

What’s the difference between a second mortgage and a home equity line of credit for this purpose?

A second mortgage is a lump-sum loan with fixed terms, interest rate, and payment schedule. A home equity line of credit (HELOC) functions more like a credit card—you can borrow up to a limit as needed, pay it back, and borrow again. HELOCs typically offer lower rates but require good credit and may not provide sufficient funds for large tax liens. Second mortgages are generally easier to qualify for and better suited to one-time large payoffs like CRA debts.

Will taking out a second mortgage affect my taxes or create new tax obligations?

Generally, mortgage debt itself is not taxable income. However, if you use the second mortgage proceeds for business purposes or investment properties, the interest may be tax-deductible. Using the funds for personal purposes, such as paying personal tax debts, typically makes the interest non-deductible. Consult a tax professional for advice specific to your situation, as tax rules around interest deductibility changed significantly in recent years.