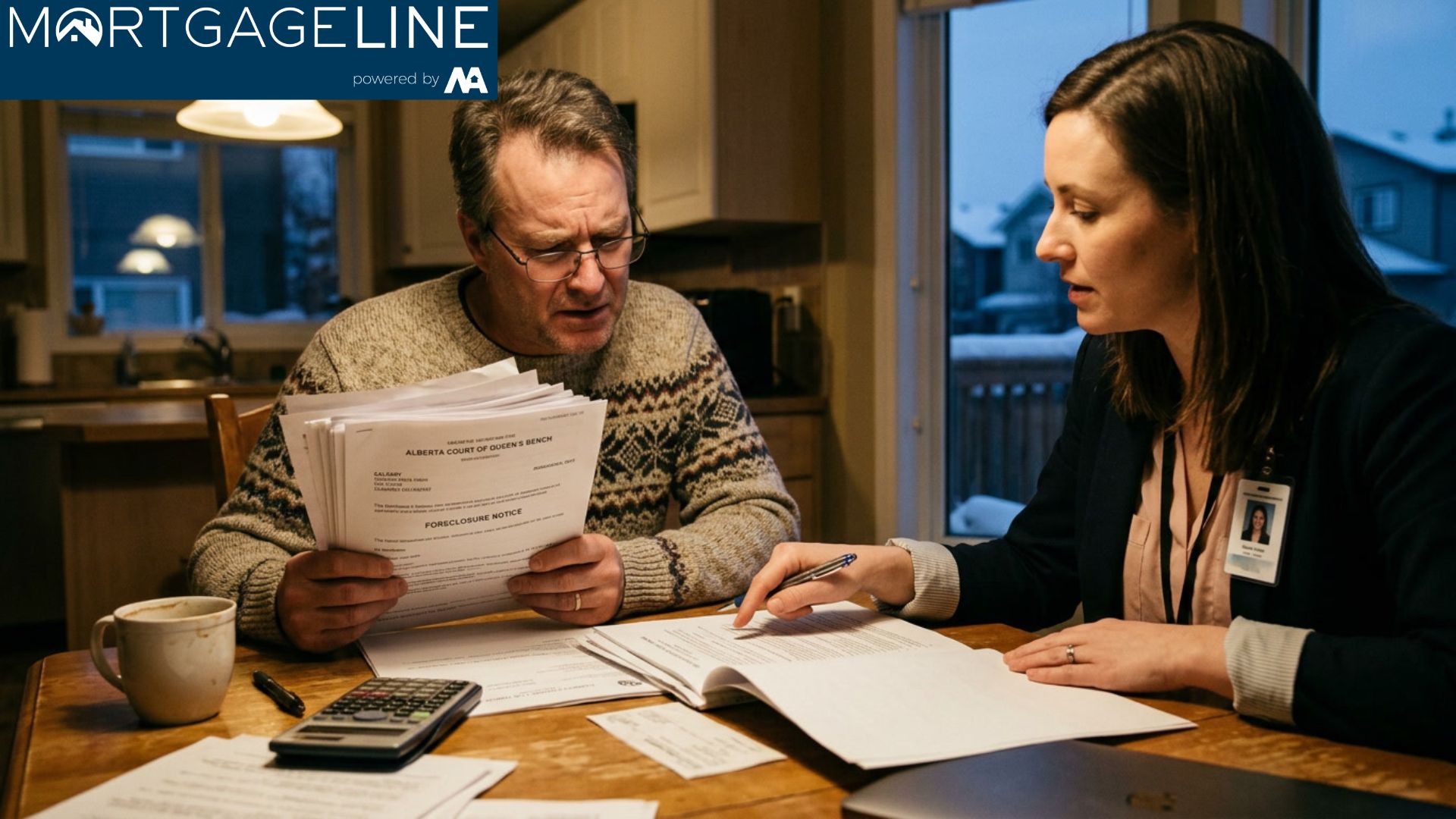

Facing a sudden mortgage default notice in Calgary can be one of the most stressful experiences a homeowner encounters. When lenders move quickly to initiate legal proceedings, homeowners often feel they have no options—but this couldn’t be further from the truth. With the right knowledge and immediate action, Calgarians can mount effective defenses against expedited foreclosure proceedings and potentially keep their homes.

This comprehensive guide walks you through exactly what to do when you receive a short notice foreclosure in Calgary, from understanding Alberta’s legal timeline to exploring every available defense strategy and alternative solution.

- Alberta homeowners typically have 6-12 months from first notice to final foreclosure—time to act

- Responding to a Statement of Claim within 20 days is critical for preserving defense options

- Legal remedies include setting aside the order, redemption periods, and court applications

- Alternative financing like second mortgages can stop foreclosure proceedings entirely

- Early intervention dramatically improves outcomes—don’t wait to seek help

Understanding Calgary’s Foreclosure Timeline

Unlike some provinces, Alberta operates under a judicial foreclosure process, which means lenders must obtain a court order to complete the sale of a defaulted property. This actually works in homeowners’ favor, as it creates multiple opportunities to defend against loss.

The process typically begins when a homeowner misses mortgage payments. The lender will send notices requiring payment, and if the debt remains unpaid, they may file a foreclosure application with the Court of King’s Bench of Alberta. According to the Alberta Courts website, once a Statement of Claim is issued, the defendant has just 20 days to respond before the lender can seek a default judgment.

Research from the Canada Mortgage and Housing Corporation indicates that the average Calgary foreclosure timeline from initial default to final order spans approximately 8-14 months, though this varies significantly based on court schedules and whether the homeowner mounts any defense. The key insight: even when homeowners receive what feels like a “short notice,” the legal process has built-in timelines that provide meaningful windows for intervention.

Immediate Steps Upon Receiving Short Notice

When you receive any foreclosure notice in Calgary, your first 72 hours are critical. Here’s what you must do immediately:

- Read every document carefully. Note the dates, amounts owed, and any response deadlines. Missing a deadline can severely limit your options.

- Contact a real estate lawyer immediately. The Law Society of Alberta maintains a referral service for qualified real estate litigation lawyers. Legal aid may be available for qualifying individuals.

- Calculate your exact financial position. Know your equity, your monthly shortfall, and what you’d need to bring the mortgage current.

- Gather all financial documentation. Bank statements, pay stubs, tax returns, and expense records will be essential for any negotiation or court application.

- Do not ignore any court documents. A Statement of Claim requires a formal response—failure to file one results in automatic judgment against you.

As Jennifer Morrison, a Calgary real estate litigation attorney, explains: “Many homeowners make the mistake of ignoring foreclosure notices because they’re embarrassed or hope the problem will resolve itself. This is precisely the wrong approach. Every day of inaction narrows your options.”

Legal Defense Strategies in Alberta Courts

Alberta’s judicial foreclosure process provides several genuine legal defenses that homeowners can pursue. Understanding these options is essential for mounting an effective response.

Setting Aside Default Judgments

If a homeowner fails to respond to a Statement of Claim within the required timeframe, the lender can seek a default judgment. However, Alberta courts have discretion to set aside such judgments if the homeowner can demonstrate a reasonable explanation for the delay and a genuine defense to the claim. According to case law from the Alberta Court of Appeal, courts balance the lender’s right to proceed against fairness to the homeowner, particularly where the homeowner has equity in the property.

Redemption Period Applications

Even after a foreclosure order is granted, Alberta courts can extend redemption periods to allow homeowners additional time to arrange financing or sell the property themselves. The Alberta Land Titles Act provides that courts may grant redemption periods of up to six months or longer in appropriate circumstances. Homeowners who can demonstrate a credible plan to bring the mortgage current often succeed in obtaining these extensions.

Challenging the Lender’s Conduct

In limited circumstances, homeowners have successfully defended against foreclosure by demonstrating that the lender violated the Financial Consumer Agency of Canada guidelines or breached the mortgage contract’s terms. This might include failures to properly apply payments, assess hardship situations, or comply with prepayment terms.

Alternative Solutions: Stopping Foreclosure Through Financing

While legal defenses are important, the most effective way to stop foreclosure proceedings in Calgary is often by bringing the mortgage current or paying off the lender entirely. Several financing options can accomplish this:

Refinancing Your Existing Mortgage

If you have equity in your home and reasonable credit, refinancing with your current lender or a new financial institution may allow you to consolidate arrears and reset your payment schedule. Banks and credit unions offer various hardship programs specifically designed for homeowners facing temporary financial difficulties.

Second Mortgages for Emergency Situations

For Calgary homeowners with significant equity but damaged credit, a second mortgage can provide the funds needed to stop foreclosure proceedings. Unlike traditional refinancing, private second mortgage lenders often approve applications based primarily on property equity rather than credit scores. The funds from a second mortgage can be used to bring the primary mortgage current, pay off the existing lender entirely, or provide cash for other needs.

As mortgage broker David Chen notes: “We’ve helped numerous Calgary homeowners use their home equity to avoid foreclosure. A second mortgage of $50,000-$100,000 can often satisfy the arrears and give families breathing room to recover financially.”

Consumer Proposals and Bankruptcy Considerations

For homeowners with overwhelming debt beyond their mortgage, a consumer proposal administered by a Licensed Insolvency Trustee can temporarily halt all creditor actions, including foreclosure proceedings. According to the Office of the Superintendent of Bankruptcy Canada, once a consumer proposal is filed, creditors cannot proceed with legal action. This can provide the time needed to negotiate with the mortgage lender or arrange alternative financing.

Working With Your Lender

Many homeowners don’t realize that lenders generally prefer to avoid foreclosure whenever possible. The process is expensive, time-consuming, and often results in the lender recovering less than the full loan amount. This creates leverage for homeowners willing to negotiate.

When approaching your lender about alternatives to foreclosure, preparation is essential. Bring documentation showing your income, expenses, and a realistic budget. Propose specific solutions: a payment plan for arrears, a temporary payment reduction, or an extension of your amortization. Lenders are significantly more receptive to homeowners who demonstrate both need and the ability to move forward responsibly.

The Financial Consumer Agency of Canada requires federally regulated lenders to consider homeowners facing financial hardship and explore alternatives before initiating foreclosure. Document every communication with your lender and follow up verbal conversations with written confirmations. For specific guidance on your bank’s foreclosure process, you may want to review resources on stopping an RBC foreclosure in Alberta or managing a BMO foreclosure in Alberta.

When to Seek Professional Help

While some Calgary homeowners successfully navigate short notice foreclosure situations on their own, professional guidance significantly improves outcomes. Consider seeking help in these situations:

- You receive a Statement of Claim and don’t understand the legal process

- You’re unsure whether you have valid defenses to the foreclosure

- You need to explore financing options quickly

- The foreclosure timeline seems accelerated

- You have multiple creditors pursuing you simultaneously

The Law Society of Alberta offers a referral service matching homeowners with qualified real estate litigation lawyers. Many lawyers offer free initial consultations, and legal aid may be available for qualifying individuals. Additionally, financial advisors specializing in mortgage issues can help explore alternative financing solutions.

Common Mistakes to Avoid

Understanding common pitfalls can help you avoid them during an already stressful situation:

- Ignoring legal documents. Court documents require formal responses. Failure to respond results in automatic judgment.

- Waiting too long to act. Every day of delay reduces your options. Start immediately upon receiving any foreclosure notice.

- Accepting the first lender offer. Initial offers are often negotiable. Explore all alternatives before agreeing.

- Borrowing from predatory lenders. High-interest loans may solve the immediate problem but create long-term financial disaster.

- Neglecting other debts. Even stopping foreclosure, if you have overwhelming consumer debt, you may face other legal actions.

Calgary Foreclosure Defense Timeline: What to Expect

Understanding the typical timeline helps homeowners plan their response:

| Stage | Typical Duration | Homeowner Actions |

|---|---|---|

| Missed Payments | 1-3 months | Contact lender, explore hardship options |

| Pre-Foreclosure Notices | 1-2 months | Gather documentation, seek legal advice |

| Statement of Claim | 20 days to respond | File formal response, explore all defenses |

| Court Proceedings | 3-8 months | Negotiate with lender, arrange financing |

| Redemption Period | Up to 6 months | Execute plan to bring mortgage current |

| Final Order / Sale | 1-2 months | Vacate property or appeal if applicable |

Conclusion

Receiving short notice of foreclosure in Calgary is undoubtedly stressful, but it’s far from hopeless. Alberta’s judicial foreclosure process provides meaningful opportunities to defend against loss—whether through legal challenges, extended redemption periods, or alternative financing. The keys are immediate action, professional guidance, and persistence.

If you’re facing a short notice foreclosure in Calgary, don’t navigate this alone. The stakes are too high, and the options too complex. Contact our team today to explore your options and develop a personalized defense strategy. Get in touch with our team to schedule a free consultation and learn how we can help you protect your home and your family’s future.

References

- Alberta Courts – Official information on judicial foreclosure processes

- Financial Consumer Agency of Canada – Guidelines for lenders and homeowner protections

- Law Society of Alberta – Lawyer referral services

- Office of the Superintendent of Bankruptcy Canada – Information on consumer proposals and bankruptcy

- Canada Mortgage and Housing Corporation – Housing research and statistics

Frequently Asked Questions

How quickly can foreclosure happen in Calgary?

While the complete foreclosure process in Alberta typically takes 8-14 months, homeowners must respond to legal documents within 20 days of receiving a Statement of Claim. Failure to respond can result in a default judgment and accelerated timeline. Early action is essential to preserve all defense options.

Can I stop a foreclosure after the court has issued a judgment?

Yes, in certain circumstances. Alberta courts have discretion to set aside default judgments if you can demonstrate a reasonable explanation for failing to respond and a genuine defense. Additionally, courts can extend redemption periods even after judgment to allow homeowners time to arrange financing or sell the property.

Will a second mortgage actually stop foreclosure proceedings?

Yes, if the funds are used to pay off or bring current the primary mortgage. When a homeowner pays the full amount owed to the primary lender, including all arrears and legal costs, the lender will typically discharge the mortgage and the foreclosure proceedings end. A second mortgage can provide these funds.

What happens if I can’t afford my mortgage but have significant equity?

Homeowners with significant equity have several options beyond foreclosure. You might sell the property yourself (often for more than a foreclosure auction price), refinance with a new lender, or take out a second mortgage to access equity while keeping the property. Each option has different implications for your credit and financial future.

Should I file a consumer proposal to stop foreclosure?

A consumer proposal can temporarily halt all creditor actions, including foreclosure, but it’s a significant financial decision with long-term consequences. It should be considered when other options aren’t available and when you have significant unsecured debt beyond your mortgage. Consult with a Licensed Insolvency Trustee and a lawyer to understand all implications.

How do I find a good lawyer for foreclosure defense in Calgary?

The Law Society of Alberta offers a lawyer referral service that matches individuals with qualified real estate litigation lawyers. Many lawyers offer free initial consultations. Look for lawyers with specific experience in real estate litigation and foreclosure defense. Check credentials and ask about their experience with similar cases.

Can the lender foreclose while I’m negotiating with them?

Yes, lenders can and sometimes do proceed with foreclosure while negotiations are ongoing. This is why it’s important to document all communications, respond to legal documents promptly, and have backup plans in place. Never rely solely on negotiations—always maintain your legal options simultaneously.

What are my rights under Alberta’s foreclosure laws?

Alberta homeowners have the right to receive proper legal notice, respond to court proceedings, present defenses, request redemption periods, and have cases heard fairly. Federally regulated lenders must also comply with the Financial Consumer Agency of Canada guidelines, which require consideration of homeowner hardship situations before initiating foreclosure.