Securing a second mortgage during a Calgary oil and gas downturn requires bypassing traditional A-lenders, who enforce strict federal stress tests, and partnering with equity-based private lenders. These alternative institutions focus primarily on your property’s Loan-to-Value (LTV) ratio, allowing laid-off energy workers and independent contractors to access vital capital based on remaining home equity rather than a continuous two-year T4 income history. By leveraging the intrinsic value of your real estate, you can consolidate high-interest debt, bridge employment gaps, and protect your home from foreclosure even when commodity prices drop.

Key Takeaways

- Equity Over Employment: Private lenders prioritize your home’s remaining equity (up to 80% LTV) rather than your current employment status or recent layoffs.

- Algorithmic Penalties: Traditional banks automatically strip away variable, overtime, and bonus income for energy sector workers during macroeconomic slumps.

- Alternative Documentation: Self-employed contractors can bypass strict T4 requirements by utilizing business bank statements and active contracts.

- Proactive Consolidation: Securing a second mortgage before severance runs out preserves your credit score and lowers monthly obligations.

- Foreclosure Prevention: Equity extraction can provide a 6-to-12-month payment holiday on your primary mortgage, stopping legal action in its tracks.

The 2026 Petro-Dollar Effect on Calgary Real Estate

Living in Calgary means living with the rhythm of the global energy sector. When oil prices surge, the city buzzes with construction, new trucks on the Deerfoot, and widespread economic optimism. When prices drop, corporate budgets tighten, and financial uncertainty creeps into households. For homeowners in 2026, this volatility directly impacts your most valuable asset and your ability to leverage it.

In Alberta, real estate valuations and natural resources are inextricably linked. When the energy sector contracts, corporate layoffs and reduced operational hours inevitably lead to a spike in mortgage arrears. Financial institutions possess decades of historical data tracking this exact correlation. Consequently, they view Calgary properties—and the borrowers who own them—through a lens of extreme caution during market corrections.

According to the Alberta Economic Dashboard, approximately 30% of Calgary’s workforce is directly or indirectly tied to the energy sector. When capital spending pauses, the ripple effect touches every neighborhood. For you, this means the automatic approval you expect based on a 750+ credit score is no longer guaranteed. Lenders heavily scrutinize the stability of your income, especially if your employer operates in the energy service sector.

Why Traditional Banks Tighten Lending Criteria

Major banks, known as A-lenders, are fundamentally risk-averse. They operate under strict federal guidelines established by the Office of the Superintendent of Financial Institutions (OSFI), specifically the B-20 stress test. These regulations require them to rigorously evaluate a borrower’s ability to service debt at inflated interest rates. During a downturn, these algorithms become highly restrictive.

The Single-Industry Risk Factor

Banks classify Calgary as a resource-dependent market. When global energy markets struggle, risk models flag the entire region as a high-risk lending zone. Even if your specific job in healthcare or tech is perfectly secure, the bank’s automated underwriting system might penalize your application simply because you live in a postal code heavily affected by recent corporate layoffs.

“Lenders view Calgary’s real estate through a macroeconomic lens. When Western Canadian Select (WCS) crude drops below $70 a barrel, algorithmic risk models automatically tighten debt-service ratios for energy sector workers,” explains Dr. Aris Thorne, Professor of Real Estate Economics at the University of Calgary.

This systemic tightening leaves many highly qualified homeowners stranded without access to capital. If you work in the oil sands or for a specialized service company, a significant portion of your annual earnings likely comes from overtime, performance bonuses, or field allowances. In a booming economy, traditional lenders happily include this variable income in your debt-service calculations. In a downturn, underwriters aggressively strip it away, calculating your affordability based strictly on your guaranteed base salary.

The Solution: Equity-Based Private Lending

This is where the alternative lending market shines. Unlike major banks that fixate on your T4s or T1 Generals, private lenders focus almost entirely on the hard asset. If you have built up substantial equity in your home, they are willing to overlook temporary gaps in contract work or recent credit blemishes.

Private lenders understand that the Alberta oil and gas industry is inherently cyclical. They know that a lull in 2026 does not equate to zero income forever. They are primarily concerned with one question: Is there enough equity in the property to cover the loan if a default forces a sale? If the answer is yes, they can approve a second mortgage regardless of your current employment status.

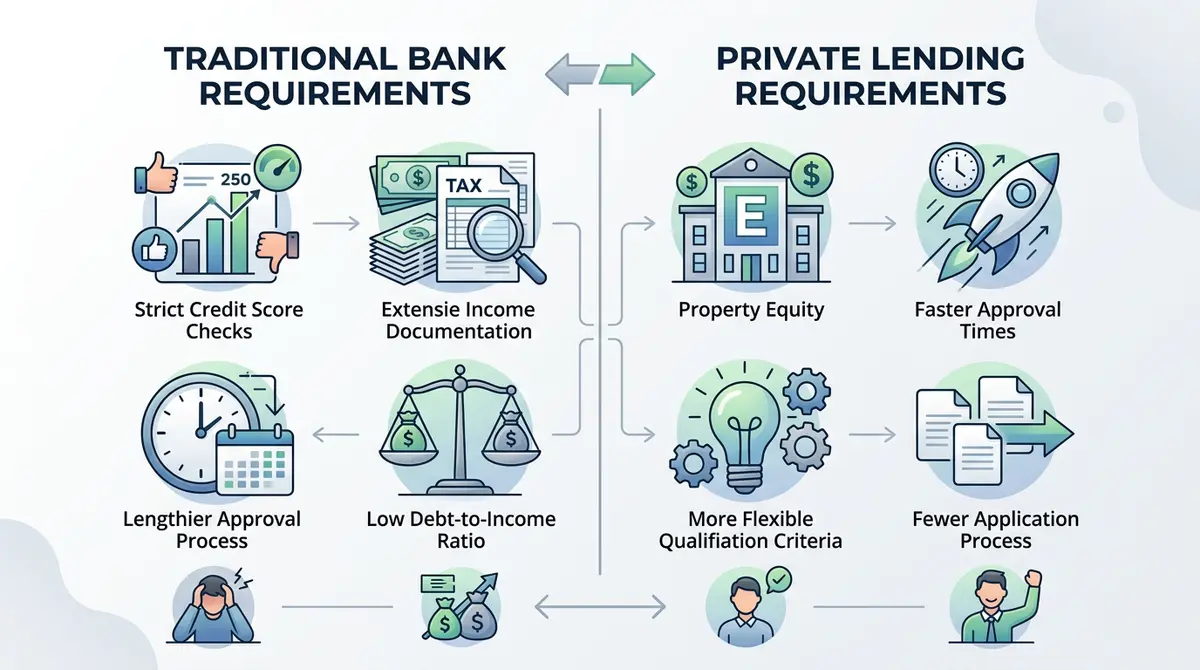

Comparing Lenders During an Economic Slump

To highlight the stark differences in lending approaches during a 2026 market correction, review the comparison table below. It outlines exactly what to expect from different financial institutions.

| Lending Metric | Traditional Banks (A-Lenders) | Private Equity Lenders |

|---|---|---|

| Income Verification | Strict 2-year continuous T4 history | Stated income or business bank statements |

| Maximum LTV | Typically capped at 65-70% in downturns | Up to 80% (sometimes 85% in urban zones) |

| Approval Speed | 3 to 4 weeks with heavy scrutiny | 5 to 10 business days |

| Credit Score Focus | Minimum 680+ required | Flexible; focuses on property equity |

| Employment Status | Must be currently employed full-time | Laid-off or contract workers accepted |

Step-by-Step: How to Secure a Second Mortgage in a Downturn

Navigating alternative lending requires a proactive, strategic approach. Waiting until your severance package runs dry is the most dangerous financial mistake a homeowner can make. Follow these steps to secure funding efficiently.

- Calculate Your True LTV: Determine your home’s realistic current value (not the boom-time peak) and subtract your first mortgage balance. You can typically borrow up to 80% of this value. Remember that appraisers use conservative comparables during a slump.

- Gather Alternative Documentation: Skip the T4s. Prepare your corporate bank statements, future contract letters, and a detailed list of assets. Reviewing a comprehensive document checklist for second mortgages ensures you don’t delay the underwriting process.

- Apply Proactively: Submit your application while your credit score remains above 680 and before you miss any unsecured debt payments. Proactivity gives you negotiating power.

- Define Your Exit Strategy: Private lenders want to know how you will pay them back. Outline your plan to return to work, sell the property, or transition to cash-out refinancing alternatives with an A-lender in 12 to 24 months.

Strategic Debt Consolidation and Foreclosure Prevention

An economic downturn inevitably brings a severe cash flow crunch. You might be asset-rich with $200,000 of equity in your home, but entirely cash-poor on a month-to-month basis. High-interest credit card debt can spiral out of control if you use it to supplement lost income.

“The biggest mistake homeowners make is waiting until severance packages run out. Proactive equity extraction preserves your credit score when you need it most,” says Sarah Jenkins, Senior Underwriter at Alberta Private Capital.

A second mortgage can consolidate 24% credit card debt into a single, manageable monthly payment at 10-12%. By drastically lowering your monthly obligations, you reduce the pressure on your diminished household income. It is crucial to understand how compounding frequency affects your debt, as swapping daily compounding credit cards for semi-annual compounding mortgages saves thousands in interest over a 12-month period.

Protecting Your Home from Foreclosure

The fear of foreclosure is a terrifying reality during a prolonged recession. If you have already fallen behind on your primary mortgage, a second mortgage can be used to bring your first mortgage current. This strategy stops the legal bleeding immediately.

Securing these funds buys you critical time—typically a 12-month payment holiday. This window allows you to sell the property on your own terms or secure new employment, rather than being forced out by the bank. Understanding the timeline of a foreclosure in Calgary highlights exactly why acting early is imperative to protect your accumulated wealth.

Navigating Alternative Income Verification for Contractors

Calgary is home to thousands of incorporated consultants, engineers, and independent contractors. You might boast a decade-long history of high six-figure earnings, but a market downturn instantly classifies you as a variable risk in the eyes of a traditional underwriter.

If the downturn causes a three-month gap between your contracts, a bank views your income as fundamentally unstable. To overcome this, self-employed borrowers must present alternative documentation. Lenders will look at your corporate bank statements, active contracts, and overall business health rather than relying solely on a Notice of Assessment. Exploring stated income options for entrepreneurs becomes a necessary alternative for those whose tax returns do not reflect their true cash flow.

Furthermore, alternative lenders apply a common-sense approach to underwriting. They understand how to properly verify self-employed income by looking at gross business deposits rather than net taxable income after aggressive corporate write-offs.

Contrarian Investing: Leveraging Equity During a Slump

While many panic during a downturn, contrarian investors view market corrections as generational buying opportunities. According to Reuters energy market reports, prolonged commodity dips suppress regional housing demand, causing property values to stagnate or retreat by an average of 5-10%.

If you hold a stable job outside the energy sector—such as in healthcare, education, or government—you are in a prime position to capitalize on lower property valuations. You can leverage a second mortgage on your primary residence to fund the down payment on a discounted rental property. With competition scarce and prices suppressed, acquiring assets now ensures significant appreciation when the oil cycle inevitably turns upward again.

Conclusion

Calgary is a remarkably resilient city, and so are its homeowners. While securing a second mortgage during an oil and gas downturn requires more careful navigation than during a boom, it remains a highly effective tool for financial survival. By separating your home’s intrinsic value from the daily fluctuations of the energy market, you can secure the funds needed to bridge the gap, consolidate debt, and protect your family’s financial future.

If you are facing a cash flow crunch or need to access your home equity without traditional bank hurdles, do not wait until your options run out. Get in touch with our team today to explore your private lending options and secure your financial foundation.

Frequently Asked Questions

Will a bank give me a second mortgage if I am currently laid off?

It is highly unlikely. Major banks require proof of current, stable income to service the debt under federal stress test rules. If you are unemployed, you must seek a private lender who focuses on your property’s Loan-to-Value (LTV) rather than traditional income verification.

How much equity do I need to qualify during a downturn?

Typically, private lenders will lend up to 80% Loan-to-Value (LTV). However, during a severe economic downturn, some lenders may conservatively cap this at 75% to protect themselves against further drops in regional property values.

Are interest rates higher for second mortgages during a recession?

Yes, they generally are. Lenders perceive higher macroeconomic risk in the market, so they charge a risk premium on the interest rate. However, these rates (typically 10-12%) remain significantly lower than the 24% charged by unsecured credit cards.

Can I use a second mortgage to pay my primary mortgage?

Absolutely. This is a highly common and effective strategy for avoiding foreclosure. You can use the lump sum from a second mortgage to prepay your first mortgage for 6 to 12 months, granting you a payment holiday while you seek new employment.

Do private lenders care if my income is from oil and gas contracts?

Generally, no. Private lenders are far less concerned with the specific industry source of your income. They are primarily focused on the equity in your home and your proposed exit strategy for repaying the loan.

How long does it take to get approved by a private lender?

Unlike traditional banks that can take 3 to 4 weeks, private lenders can often approve and fund a second mortgage in 5 to 10 business days. This rapid turnaround is crucial for homeowners needing immediate debt consolidation or foreclosure relief.