Securing a second mortgage during a housing market correction requires homeowners to navigate reduced loan-to-value (LTV) maximums, heightened property appraisal scrutiny, and stricter debt-to-income thresholds. Success hinges on presenting a robust financial profile, leveraging alternative lending institutions like Mortgage Investment Corporations (MICs), and maintaining a total debt service (TDS) ratio below 40%. By accurately valuing the property with a full interior appraisal and strategically timing the application, homeowners can successfully access their built-up equity despite temporarily declining property values.

Key Takeaways

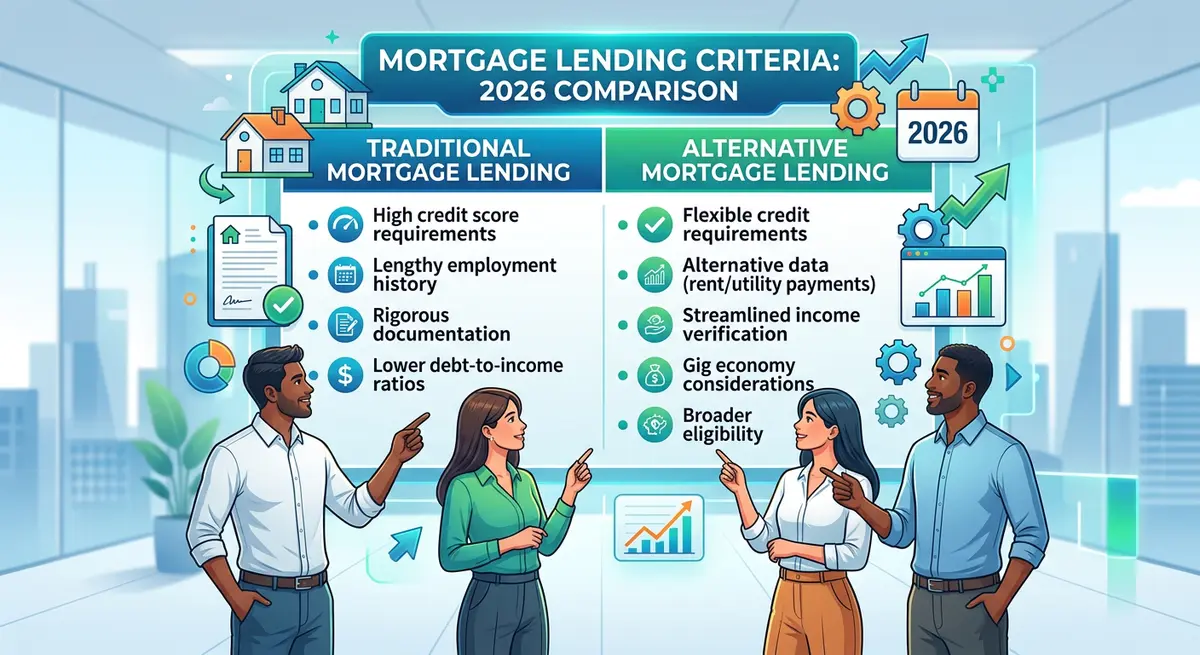

- Equity Requirements Have Increased: Traditional lenders have reduced maximum combined loan-to-value (CLTV) ratios from 85% to 75%-80% in 2026.

- Alternative Lenders Fill the Gap: As major banks tighten criteria, MICs and private lenders offer viable equity-based approvals, albeit at a 3.5% to 5% interest premium.

- Appraisal Standards are Stricter: Automated Valuation Models (AVMs) are largely rejected; lenders now require full interior appraisals with comparable sales from the last 30 to 60 days.

- Income Verification is Rigorous: Self-employed borrowers must provide 24 months of pristine financial records to prove income sustainability.

- Strategic Borrowing is Favored: Applications for high-interest debt consolidation or value-add property renovations have significantly higher approval rates than general cash-out requests.

Understanding the 2026 Calgary Real Estate Correction

Understanding the dynamics of secondary financing during a market downturn is essential for setting realistic borrowing expectations. The current market correction reflects broader economic adjustments affecting Alberta, including stabilized population growth patterns, energy sector recalibrations, and sustained interest rate policies set by the Bank of Canada. These macroeconomic factors have fundamentally altered how financial institutions assess property-backed risk.

According to recent 2026 data published by the Calgary Real Estate Board (CREB), benchmark property prices have seen a localized adjustment of 4.2% across various quadrants in the first half of the year. This correction manifests through reduced home sales volumes, listing periods extending beyond 45 days, and uneven price adjustments across different property segments. Luxury properties and condominiums are facing greater downward pressure, while entry-level single-family homes demonstrate notable resilience.

As Dr. Sarah Jenkins, Senior Housing Economist at the Alberta Real Estate Institute, explains: “In 2026, lenders are prioritizing equity preservation over borrower income. A market correction doesn’t mean liquidity disappears; it means the cost of capital and the burden of proof shift significantly onto the homeowner. Institutions are stress-testing portfolios against potential further declines.”

How Market Downturns Impact Lending Criteria

The approval process for additional financing heavily depends on how financial institutions assess risk during periods of economic volatility. Traditional lenders typically implement stricter underwriting standards to protect their capital against potential further property value declines.

Stricter Loan-to-Value (LTV) Limits

During stable economic periods, lenders frequently approve combined loan-to-value (CLTV) ratios up to 85%. However, in 2026, conservative risk management has driven these maximums down. Most traditional lenders now cap CLTV at 80% or even 75% for secondary loans. This 5% to 10% reduction directly impacts your borrowing capacity. For example, on a home previously valued at $600,000, a drop to 75% LTV means your maximum allowable debt (first and second mortgage combined) is capped at $450,000, requiring homeowners to possess substantial built-up equity before applying.

Heightened Income and Debt Verification

Debt-to-income ratios face intense scrutiny in a correcting market. Lenders have reduced maximum allowable Total Debt Service (TDS) ratios from the standard 44% down to 40% or lower. Furthermore, income verification has become rigorous. Self-employed borrowers, in particular, must provide extensive proof of business stability. Utilizing alternative documentation for business owners is increasingly common, as lenders demand 24 months of tax returns and accountant-prepared financial statements to verify income sustainability.

Elevated Credit Score Requirements

Credit score thresholds have shifted upward. While a score of 600 might have secured a subprime loan in previous years, many lenders have raised their minimum baseline to 650 in 2026. Borrowers with marginal credit profiles must focus on rapid credit repair or expect to pay a significant interest rate premium to offset the perceived risk.

Traditional Banks vs. Alternative Lenders in a Correction

When applying for secondary financing under current economic conditions, alternative lenders often become the most viable path forward. Traditional banks become highly conservative, creating a critical market gap filled by Mortgage Investment Corporations (MICs), credit unions, and private lenders.

| Lender Type | Maximum LTV (2026) | Income Verification | Approval Speed | Best Suited For |

|---|---|---|---|---|

| Traditional Banks | 75% – 80% | Extremely Strict (TDS < 40%) | 3 – 5 Weeks | Prime borrowers with high equity and T4 income. |

| Credit Unions | 80% | Moderate to Strict | 2 – 4 Weeks | Community members seeking flexible terms. |

| MICs (Alternative) | 80% – 85% | Flexible (Focus on Equity) | 1 – 2 Weeks | Self-employed or slightly bruised credit. |

| Private Lenders | Up to 85% | Minimal (Equity-Based) | 3 – 7 Days | Urgent funding needs or non-traditional income. |

According to Marcus Thorne, Chief Underwriter at Calgary Financial Trust: “We have reduced our maximum LTV thresholds by 5% across the board. However, alternative lenders are absorbing this demand by pricing the risk into their interest rates, typically charging a 3.5% to 5% premium over prime rates. For many homeowners, this premium is a necessary cost to access trapped liquidity.”

Step-by-Step Guide: Securing Your Financing in 2026

A strategic approach to obtaining equity-based financing during a market downturn involves meticulous preparation. Follow these steps to maximize your approval odds.

- Calculate Your Adjusted Home Equity: Do not rely on your property tax assessment or an outdated appraisal. Engage a professional appraiser to determine your home’s current market value. As Elena Rostova, a certified Calgary real estate appraiser, notes: “Automated valuation models (AVMs) are no longer sufficient in a correcting market. Lenders require full interior appraisals with comparable sales from the last 30 to 60 days to ensure the asset’s value is accurate.”

- Gather Comprehensive Financial Documentation: Lenders expect a flawless paperwork package. You must compile two years of Notice of Assessments (NOAs), recent pay stubs, T4s, existing mortgage statements, and property tax bills. Properly organizing your second mortgage paperwork demonstrates financial responsibility and drastically reduces underwriting delays.

- Define a Clear Purpose for the Funds: Lenders favor applications with a clear, risk-mitigating purpose. Requests for debt consolidation or home improvements that increase property value are viewed much more favorably than general cash-out requests for lifestyle expenses. Provide detailed explanations and supporting documents, such as contractor quotes or payout statements.

- Partner with a Specialized Mortgage Broker: Navigating a correcting market alone is risky. Experienced mortgage professionals understand which lenders remain active, what specific criteria changes have occurred this month, and how to position your application. They can also help you compare options to ensure your chosen product beats an unsecured line of credit in terms of overall borrowing costs.

- Establish a Clear Exit Strategy: Lenders want to know how you plan to pay off the principal. Whether it is through an anticipated year-end bonus, selling the property when the market rebounds, or refinancing the entire debt stack in 24 months, a documented exit strategy significantly boosts approval odds.

Strategic Uses for Home Equity in a Down Market

Despite the challenges, a market correction presents unique financial opportunities for well-positioned homeowners. Leveraging equity strategically can yield long-term financial benefits, provided the capital is deployed intelligently.

High-Interest Debt Consolidation

With inflation impacting household budgets, consolidating high-interest unsecured debt is the most common and effective use of equity in 2026. For example, transferring $40,000 of 22% credit card debt into a 9% to 12% equity loan can drastically improve monthly cash flow. This strategy lowers your overall TDS ratio and provides immediate financial relief, protecting your credit score from missed payments.

Value-Add Property Renovations

Investing in your primary residence through strategic renovations can force appreciation, counteracting the broader market’s downward trend. Projects that add livable square footage, such as developing a legal basement suite, not only increase the property’s appraised value but can also generate rental income to offset the new debt obligations. These equity extraction strategies must be calculated carefully to ensure the return on investment exceeds the cost of borrowing.

Real Estate Investment Opportunities

Market corrections often result in discounted asset prices. Savvy investors use their primary residence’s equity to fund a down payment on an investment property, acquiring real estate while prices are temporarily depressed. This requires careful cash flow analysis to ensure the rental income covers the new debt obligations and provides a buffer for vacancy periods.

Risk Management and Long-Term Considerations

Managing the risks of secondary financing requires forward-thinking financial planning. Borrowers must look beyond the initial funding and plan for the entire lifecycle of the loan, especially when property values are fluctuating.

Interest rate environments remain volatile. When securing new financing, you must stress-test your budget against potential rate increases at renewal. According to the Canada Mortgage and Housing Corporation (CMHC), borrowers who maintain a 10% buffer in their monthly debt-servicing budget are significantly less likely to face default during economic downturns. It is also crucial to understand how compounding frequency silently increases your debt, as many alternative lenders compound interest monthly rather than semi-annually.

Furthermore, meticulous record-keeping is non-negotiable. Knowing how long to retain your mortgage documents is vital for future refinancing efforts, tax purposes, and potential audits by Statistics Canada or the CRA regarding investment-related interest deductions. Always maintain digital and physical copies of your appraisal, commitment letter, and payout statements.

Frequently Asked Questions (FAQ)

Can I get approved if my Calgary home has dropped in value?

Yes, you can still secure financing if your home has decreased in value, provided you still have sufficient equity. Lenders will base their LTV calculations on a current, conservative appraisal rather than your original purchase price or previous peak value.

What is the minimum credit score required in 2026?

Traditional banks typically require a minimum credit score of 650 to 680 during the current market correction. However, alternative and private lenders focus more on property equity and may approve borrowers with scores below 600, though at higher interest rates.

How long does the approval process take during a market correction?

Approval timelines vary significantly by lender type. Traditional banks may take 3 to 5 weeks due to heightened underwriting scrutiny, while private lenders and MICs can often approve and fund applications within 5 to 10 business days.

Will a lender accept an automated appraisal (AVM) right now?

In a correcting market, most lenders reject Automated Valuation Models (AVMs) because they lag behind real-time price drops. You should expect to pay for a full interior appraisal conducted by a certified local appraiser.

Is it better to get a second mortgage or break my first mortgage to refinance?

This depends entirely on your current first mortgage rate. If you hold a low fixed rate on your first mortgage, breaking your first mortgage to refinance could trigger massive prepayment penalties and force you into a higher rate for the entire balance. Secondary financing allows you to preserve your favorable first mortgage terms.

What happens if my property value drops further after I get the loan?

Once your loan is funded, a subsequent drop in property value does not change your current loan terms or trigger an immediate recall of the loan, provided you continue making your payments on time. However, it may make renewing the loan at the end of its term more difficult if your LTV exceeds the lender’s maximum threshold at that time.

Can I use the funds to start a business?

Yes, leveraging home equity to inject capital into a business is a common strategy. However, lenders will heavily scrutinize your business plan and exit strategy. Alternative lenders are generally more receptive to funding business ventures than traditional banks, which prefer to see funds used for property improvements or debt consolidation.

Conclusion

Navigating the complexities of secondary financing during Calgary’s 2026 housing market correction requires a strategic, well-documented approach. While traditional lenders have tightened their LTV limits and increased income scrutiny, alternative lenders continue to provide vital liquidity to homeowners with sufficient equity. By understanding the shifting appraisal standards, preparing a flawless documentation package, and clearly defining the purpose of your funds, you can successfully leverage your home’s value to achieve your financial goals, even in a downward trending market.

If you are struggling to navigate these stricter lending criteria or need help finding an alternative lender that fits your unique financial situation, professional guidance is essential. Contact our team today to discuss your options and secure the financing you need.