Homeowners securing subordinate financing in Alberta typically encounter broker compensation ranging from 1.5% to 3.0% of the gross loan amount, supplemented by fixed administrative processing costs between $300 and $800. Because these loans represent a secondary lien position, they inherently carry elevated risk profiles for lenders, necessitating specialized sourcing and underwriting by licensed professionals. Understanding exactly what you are paying for, which fees are negotiable, and how these costs impact your overall cost of borrowing is critical for making an informed financial decision in 2026.

Key Takeaways for Alberta Homeowners

- Standard Commission Rates: Broker commissions generally fall between 1.5% and 3.0% of the gross loan amount, heavily dependent on transaction complexity and lender type.

- Upfront vs. Hidden Costs: Most broker fees are deducted directly from the loan proceeds at closing. You rarely pay out-of-pocket, but your net loan amount is reduced.

- Regulatory Protection: The Real Estate Council of Alberta (RECA) mandates strict, upfront disclosure of all broker remuneration via a Form 10 document before you sign a commitment letter.

- Negotiation Power: Borrowers with high credit scores and substantial home equity (Loan-to-Value under 65%) possess the highest leverage to negotiate lower broker fees.

- Administrative Caps: While percentage-based commissions are standard, borrowers can often negotiate a hard cap on flat processing and administrative fees.

Understanding the Structure of Alternative Lending Compensation in 2026

The alternative lending landscape in Alberta has evolved significantly over the past decade. Unlike primary mortgages where major financial institutions typically pay the broker a finder’s fee behind the scenes, subordinate financing often involves private lenders, Mortgage Investment Corporations (MICs), or specialized B-lenders. In these scenarios, the borrower is frequently responsible for compensating the broker directly. This compensation is broken down into several distinct categories.

Origination and Brokerage Commissions

The origination fee serves as the primary source of income for an alternative lending professional. This fee compensates the broker for underwriting your file, sourcing capital from specialized lending networks, and structuring a deal that mitigates lender risk while meeting your specific financial requirements. In 2026, a standard $100,000 subordinate loan will typically carry a broker fee of $1,500 to $3,000.

According to a 2026 market analysis by the Canada Mortgage and Housing Corporation (CMHC), alternative lending volumes in major metropolitan areas have increased by 14% year-over-year. This surge has made private lender networks more competitive, but also more risk-averse, requiring brokers to perform deeper due diligence to secure approvals.

Processing and Administrative Costs

Beyond the percentage-based commission, brokers often charge flat processing fees. These range from $300 to $800 and cover the hard costs of assembling your application. This includes pulling credit bureaus, verifying property tax statements, conducting preliminary title searches, and managing the extensive paperwork required by private lenders.

To ensure your file moves quickly and avoids unnecessary administrative delays that could inflate these costs, it is highly recommended to review a comprehensive document checklist before formally applying.

Commission Models: Who Actually Pays the Broker?

Broker compensation models dictate exactly how and when the fee is paid. Understanding these models helps you accurately calculate your Annual Percentage Rate (APR) and total cost of capital. There are three primary structures utilized in the Alberta market today.

| Commission Model | How It Works | Best Suited For | Impact on Interest Rate |

|---|---|---|---|

| Borrower-Paid (Direct) | Fee is added to the loan amount or deducted from gross proceeds at closing. | Private mortgages and complex alternative lending scenarios. | Often results in a lower nominal interest rate, as the lender does not build the broker’s fee into their yield. |

| Lender-Paid (Indirect) | The lender pays the broker a finder’s fee upon successful funding. | Institutional B-lenders and borrowers with strong credit profiles. | Typically results in a slightly higher interest rate, as the lender recovers the commission cost over the loan term. |

| Hybrid Structure | Broker receives a small base fee from the lender and a reduced percentage from the borrower. | Mid-tier credit profiles or specialized commercial-residential mixed properties. | Balances upfront closing costs with manageable monthly interest payments. |

Key Variables Dictating Your Total Cost of Borrowing

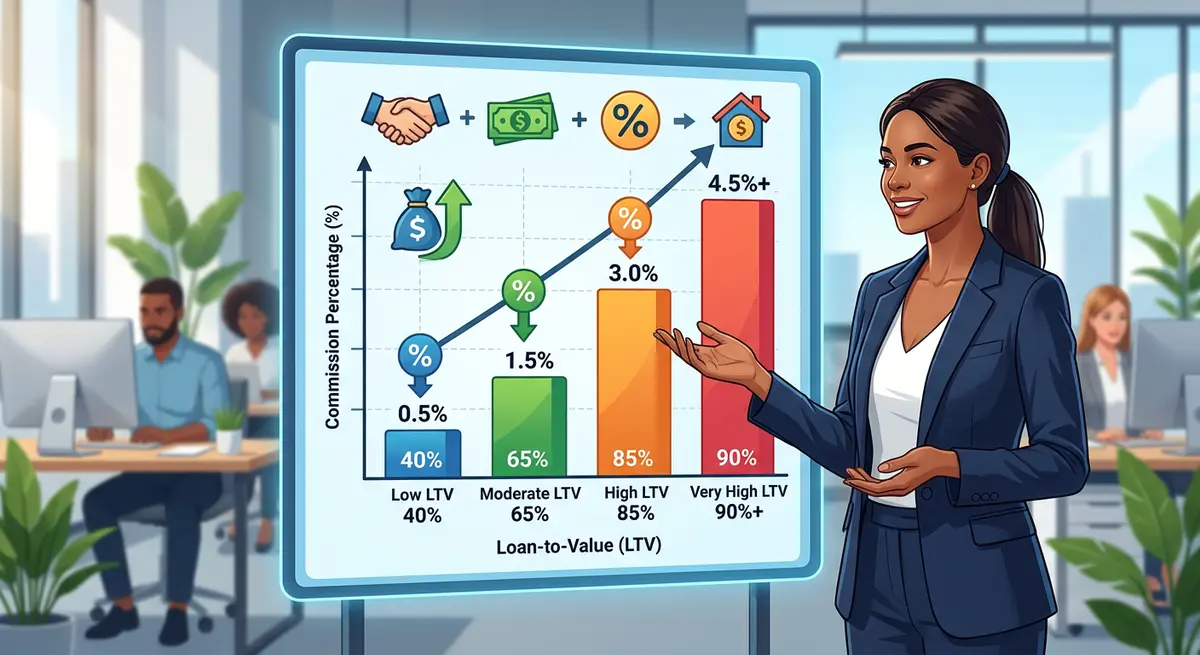

Not all borrowers pay the same rate. Several critical variables dictate where you fall on the 1.5% to 3.0% fee spectrum. Brokers assess the amount of labor required to fund your deal based on these specific risk factors.

Loan-to-Value (LTV) Ratios and Risk Assessment

Your LTV is the single most significant determinant of transaction complexity. If your primary mortgage and proposed secondary financing combined equal less than 65% of your home’s appraised value, brokers can easily place your deal with multiple competing lenders. This competition naturally drives fees down toward the 1.5% mark.

Conversely, pushing your LTV to 80% or 85% requires specialized private lenders who demand rigorous due diligence. This demands significantly more effort from the broker, justifying a higher fee of 2.5% to 3.0%.

Credit Profiles and Income Verification Complexity

Borrowers with strong credit scores and traditional T4 income require less underwriting effort. However, if you are a business owner relying on bank statements rather than tax returns, the broker must perform complex income reasonability assessments. Entrepreneurs seeking stated income alternative financing should expect slightly higher processing fees due to the extensive documentation required to satisfy anti-money laundering (AML) regulations.

Furthermore, if you have recent credit hits, knowing how to properly explain recent credit inquiries to your broker can prevent your file from being classified as high-risk, potentially saving you hundreds of dollars in risk premiums.

Economies of Scale on Loan Size

Because the administrative workload for a $50,000 loan is nearly identical to a $300,000 loan, brokers often implement minimum fee thresholds. A $40,000 loan might carry a flat $2,000 fee (effectively 5%), whereas a $400,000 loan might be negotiated down to a 1.25% commission due to the sheer volume of the transaction.

Step-by-Step: How to Negotiate Lower Mortgage Broker Fees

Many homeowners mistakenly believe that broker compensation is entirely fixed and non-negotiable. While minimums certainly exist to cover operational costs, there is often room for negotiation, especially for prime borrowers with substantial equity.

- Request the Initial Disclosure Early: Under Alberta law, brokers must provide a written estimate of all fees. Ask for this document before signing an exclusivity agreement. This allows you to shop the rate effectively.

- Compare the APR, Not Just the Rate: The Annual Percentage Rate includes both the interest rate and the broker fees. A 10% rate with a 1.5% fee is mathematically superior to a 9.5% rate with a 3.0% fee on a standard one-year term.

- Leverage Your Alternatives: If you have strong equity, mention that you are also weighing against an unsecured line of credit. Brokers are far more likely to sharpen their pencils if they know they are competing against traditional bank products.

- Cap Administrative Costs: While percentage commissions are standard for origination, you can often negotiate a hard cap on processing and administrative fees, ensuring they do not exceed $500 regardless of how many credit bureaus are pulled.

Alberta’s Regulatory Framework and Consumer Protection

The mortgage brokerage industry in Alberta operates under strict provincial oversight. The Real Estate Council of Alberta (RECA) enforces rigorous standards regarding fee transparency, ethical conduct, and fiduciary duty.

As Marcus Thorne, Lead Economist at the Alberta Lending Institute, explains: “Transparency in alternative lending has improved drastically over the last five years. In 2026, Alberta brokers are legally mandated to present a Form 10 disclosure that explicitly outlines every dollar of remuneration they receive, whether from the borrower, the lender, or a combination of both. This eliminates the hidden yield spread premiums that historically confused consumers.”

If a broker attempts to charge upfront fees before a loan commitment is officially issued by a lender, this is a major red flag. Legitimate broker fees are almost exclusively paid at the time of closing through the real estate lawyer’s trust account. For further information on your rights, borrowers can consult the Alberta Consumer Protection guidelines.

Real-World Case Study: Calculating Net Proceeds

To illustrate how these fees impact your bottom line, consider an Alberta homeowner taking out a $100,000 subordinate loan for debt consolidation in 2026. The property is valued at $600,000, and the primary mortgage balance is $350,000 (resulting in a 75% combined LTV).

- Gross Loan Amount: $100,000

- Broker Fee (2.0%): $2,000

- Broker Processing Fee: $400

- Lender Fee (1.0%): $1,000

- Legal and Appraisal Fees: $1,600

- Net Proceeds to Borrower: $95,000

In this scenario, the total cost of securing the capital is $5,000. Because these fees are deducted from the gross loan, the borrower receives $95,000 in hand but pays interest on the full $100,000. This highlights the critical importance of understanding the impact of compounding frequency on your total debt over the lifecycle of the loan.

Common Pitfalls and Expensive Edge Cases to Avoid

When navigating alternative lending fees, borrowers must remain vigilant against common industry pitfalls that can unnecessarily inflate borrowing costs.

Cancellation Fees and Exclusivity Clauses

Read your broker agreement carefully. Some contracts include a “cancellation fee” or “liquidated damages” clause. If the broker secures a valid mortgage commitment that matches your requested terms, but you decide to back out, you may still be legally obligated to pay a portion of their commission. Always ask for these clauses to be modified or removed before signing.

Bait-and-Switch Tactics

A less reputable broker might quote a low 1% fee upfront, only to introduce a “lender administration fee” of 2% right before closing. Because the broker and the private lender sometimes have close corporate relationships, this is effectively a hidden commission. Ensure your initial disclosure document guarantees the maximum total fees across all parties involved.

Ignoring the Refinance Alternative

Before accepting high broker fees for a subordinate lien, you must evaluate all available options. Depending on the penalty to break your current primary mortgage, evaluating a cash-out refinance might reveal that paying a bank penalty is actually cheaper than paying private lender and broker fees combined. According to recent data from the Bank of Canada, shifting interest rate environments make this calculation highly variable month-to-month.

Conclusion

While alternative mortgage broker fees represent a significant upfront cost, a highly skilled broker provides immense value. They navigate a fragmented private lending market, negotiate lower interest rates on your behalf, and structure loans that align with your long-term exit strategy. By understanding the standard 1.5% to 3.0% fee range, demanding transparent Form 10 disclosures, and leveraging your property’s equity, you can secure the capital you need without overpaying for the service.

If you are navigating the complexities of alternative lending and want to ensure you are receiving a fair, transparent rate, contact us today. Our team of licensed professionals is ready to review your file and provide a clear, no-obligation assessment of your borrowing options.

Frequently Asked Questions

Are alternative mortgage broker fees tax deductible in Alberta?

Broker fees and other borrowing costs may be tax-deductible if the proceeds of the loan are used strictly for investment purposes or to generate business income. If the funds are used for personal reasons, such as a home renovation or personal debt consolidation, the fees are not deductible. Always consult with a certified accountant for specific tax advice.

Do I have to pay the broker fee upfront out of pocket?

No. Legitimate mortgage brokers in Alberta do not require upfront out-of-pocket payments for their commission. The fee is almost universally deducted from the gross loan proceeds by your real estate lawyer at the time of closing.

What happens to the broker fee if my loan doesn’t fund?

If the broker fails to secure a mortgage commitment, or if the lender backs out prior to funding due to their own issues, you do not owe a broker commission. However, you may still be responsible for hard costs already incurred, such as property appraisal fees.

Why are broker fees higher for subordinate financing than primary mortgages?

Primary mortgages are typically funded by A-lenders (major banks) who pay the broker directly via a finder’s fee. Subordinate financing involves private capital and B-lenders who do not pay finder’s fees, shifting the compensation burden to the borrower. Additionally, these loans require significantly more complex underwriting and risk assessment.

Can I roll the broker fee into the total loan amount?

Yes, this is the standard practice in the industry. If you need exactly $50,000 in hand, the broker will structure a gross loan of approximately $53,000 to $55,000 to cover their commission, lender fees, and legal costs, ensuring you receive your required net proceeds.

Is a 3% broker fee considered too high for a standard file?

A 3% fee is at the higher end of the spectrum but is standard for complex files. This includes scenarios with poor credit, stated income for self-employed individuals, or high Loan-to-Value ratios (above 80%). For a straightforward, low-LTV loan, you should aim to negotiate the fee closer to 1.5% or 2.0%.