To optimally structure a secondary loan in Alberta, borrowers must select a payment frequency that matches their cash flow, choose between fixed or variable rates based on current economic policies, and negotiate an amortization period that balances monthly affordability with long-term interest savings. By leveraging accelerated bi-weekly schedules and maximizing annual prepayment privileges, homeowners can drastically reduce their total borrowing costs and build property equity faster. Navigating the subordinate financing landscape requires meticulous planning and a comprehensive understanding of your household’s financial trajectory.

Key Takeaways: Optimizing Your Payment Strategy

- Accelerated Frequencies: Switching from monthly to accelerated bi-weekly payments can reduce your amortization period by several years.

- Rate Selection: Fixed rates offer budget certainty, while variable rates provide flexibility and historically lower initial costs.

- Prepayment Privileges: Negotiating “20/20” lump-sum and payment increase options is critical for aggressive principal reduction.

- Exit Strategies: Interest-only structures require a definitive exit plan to avoid severe payment shock upon maturity.

- Debt Servicing: Maintaining a Total Debt Service (TDS) ratio below 44% ensures you can weather unexpected financial emergencies.

The Fundamentals of Subordinate Financing in Alberta

Secondary property loans operate under different mechanical principles than traditional primary mortgages, requiring borrowers to thoroughly understand the unique characteristics that dictate their financial obligations. These loans are secured against your home’s accumulated equity but rank behind your primary lender on the property title. In the event of a default or foreclosure, the primary institution is compensated first. This subordinate position inherently increases the risk for the secondary lender, which translates into higher interest rates and more rigorous qualification metrics for the borrower.

The fundamental architecture of any loan payment includes the principal (the original capital borrowed) and the interest (the cost of accessing that capital). However, secondary financing often features alternative architectural structures, such as balloon payments, interest-only periods, or fully open terms, which can dramatically alter your monthly cash flow. Comprehending how these variables interact empowers you to make data-driven decisions regarding payment amounts, frequencies, and timing.

According to the Financial Consumer Agency of Canada (FCAC), borrowers who possess a comprehensive understanding of their loan’s compounding frequency and amortization schedule are 40% less likely to default on subordinate financing. Local economic indicators, fluctuating property valuations, and regional lending guidelines all play pivotal roles in determining the payment architectures available in Alberta.

As Marcus Thorne, Chief Economist at the Alberta Lending Institute, notes: “In 2026, the most successful borrowers are those who match their secondary financing amortization directly to their anticipated exit strategy, rather than defaulting to the longest available term simply to secure the lowest monthly payment.”

Payment Frequency: Monthly vs. Bi-Weekly vs. Weekly

Selecting the appropriate payment frequency is arguably the most immediate and effective method to structure your debt obligations in Calgary. Your selection directly impacts both your day-to-day household budgeting and the aggregate cost of borrowing over the lifespan of the loan. While monthly payments remain the industry standard due to their alignment with traditional salary schedules, alternative frequencies offer substantial mathematical advantages.

| Payment Frequency | Payments Per Year | Cash Flow Impact | Interest Savings Potential |

|---|---|---|---|

| Monthly | 12 | Highly predictable, aligns with most bills | Baseline (Lowest savings) |

| Semi-Monthly | 24 | Aligns with 1st/15th corporate payrolls | Minimal improvement over monthly |

| Bi-Weekly (Accelerated) | 26 | Requires careful budgeting for 3-paycheck months | High (Effectively 1 extra monthly payment/year) |

| Weekly (Accelerated) | 52 | Constant cash outflow | Maximum (Continuous principal reduction) |

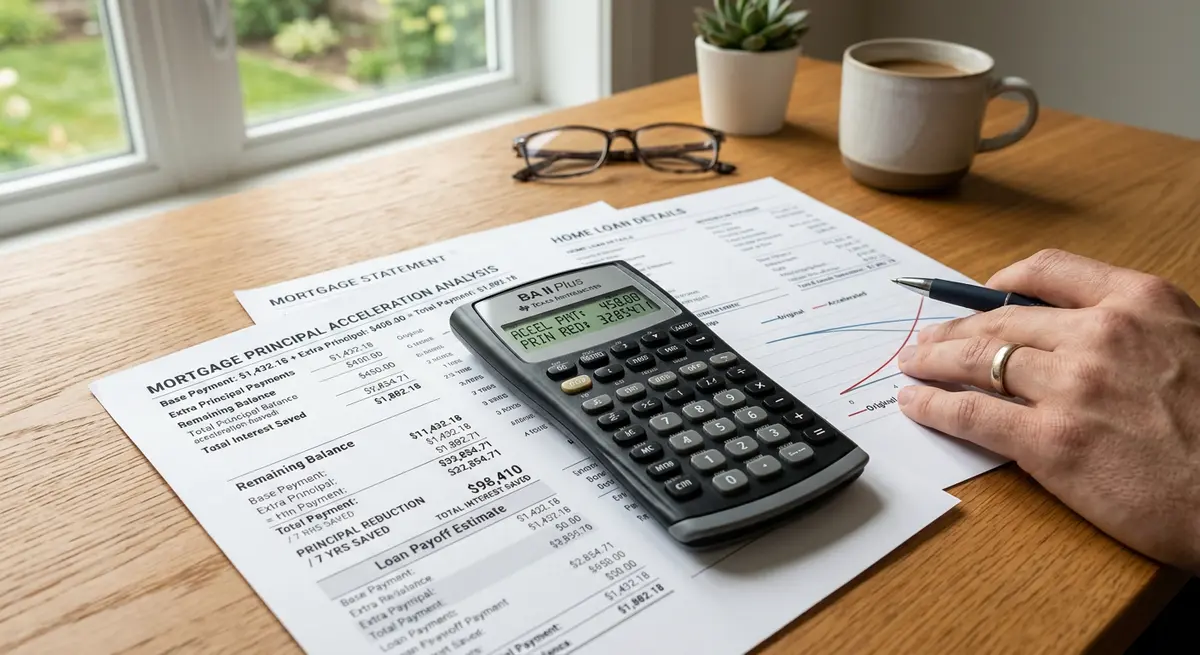

Data released by the Calgary Real Estate Board (CREB) in early 2026 indicates that homeowners who utilize accelerated bi-weekly schedules on their subordinate financing pay off their loans 18% faster than those adhering to standard monthly schedules. This acceleration occurs because the borrower makes 26 half-payments, which mathematically equates to 13 full monthly payments per calendar year.

For borrowers seeking to grasp the underlying mathematics of these savings, exploring how compounding frequency impacts your total debt load is a mandatory next step. Continuous, smaller payments chip away at the principal balance before the interest has an opportunity to compound, resulting in exponential savings over a five-year term.

Fixed vs. Variable Interest Rates in 2026

The dichotomy between fixed and variable interest rates fundamentally dictates your payment structure and long-term financial resilience. The Bank of Canada policy rate directly governs variable lending products, making this a critical strategic decision in 2026’s dynamic economic climate.

Fixed-rate products provide absolute payment stability throughout the contracted term. This predictability is invaluable for Calgary homeowners operating on strict household budgets, where unexpected payment fluctuations could precipitate severe financial distress. A fixed rate shields the borrower from macroeconomic volatility and inflationary pressures.

Conversely, variable-rate products typically launch with lower initial interest rates than their fixed counterparts, potentially reducing immediate payment burdens and enhancing short-term cash flow. However, borrowers opting for variable structures must possess the financial elasticity to absorb potential payment escalations. Variable loans also generally feature superior structural flexibility, offering more generous prepayment privileges and significantly lower penalties if the borrower needs to break the contract prematurely.

David Chen, Financial Policy Analyst at the Canadian Mortgage Institute, states: “With the 2026 economic indicators showing stabilization, variable rates are increasingly attractive for borrowers who prioritize flexibility and lower break penalties, provided they have stress-tested their household budgets against a 200 basis point increase.”

Amortization Periods and Debt Servicing

Amortization periods for subordinate loans in Alberta typically span from 5 to 25 years, a noticeably shorter horizon than the 25 to 30-year terms standard with primary mortgages. This compressed timeframe directly influences your payment architecture by necessitating larger monthly disbursements to retire the principal within the mandated period.

While shorter amortizations trigger higher mandatory payments, they obliterate the total interest accrued over the loan’s lifecycle. For instance, a $100,000 loan amortized over 10 years will demand significantly higher monthly capital than a 20-year schedule, but the interest preserved over that decade can easily exceed tens of thousands of dollars.

During the underwriting process, lenders rigorously evaluate your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios. Traditional A-lenders mandate that your TDS remains below the 42-44% threshold. If you are an entrepreneur or freelancer, you might need to explore stated income options to ensure your approved payment structure accurately reflects your real-world earning capacity rather than solely your historically taxable income.

Interest-Only vs. Graduated Payment Structures

Interest-only payment architectures offer temporary liquidity relief for Calgary borrowers who require minimized initial disbursements but possess a concrete plan to escalate their payment capacity in the near future. During this interest-only window—which typically spans 1 to 5 years—the borrower services only the cost of the capital, leaving the principal balance entirely untouched.

This specific structure is highly coveted by real estate investors utilizing the capital for income-producing assets, or homeowners navigating temporary, verifiable financial constraints. However, it demands extreme financial discipline. Without a strategy to eventually attack the principal, the borrower is merely renting the money.

Sarah Jenkins, Senior Underwriter at Calgary Equity Partners, explains: “Interest-only structures are not a permanent financial solution; they are a strategic bridge. Borrowers must possess a definitive, documented plan for principal reduction before the term matures. Otherwise, they risk catastrophic payment shock when the loan reverts to a fully amortizing schedule.”

Graduated payment plans serve as a viable alternative. These structures commence with lower payments that systematically increase over time according to a pre-negotiated schedule. This is particularly effective for Calgary professionals early in their corporate careers who anticipate guaranteed salary escalations, or investors undertaking property renovations that will subsequently yield higher rental revenues.

5 Steps to Optimize Your Payment Plan

Establishing the optimal payment architecture requires a systematic, analytical approach. Follow these five sequential steps to ensure your financing aligns with your overarching wealth-building goals in 2026:

- Calculate Your Available Equity: Determine your property’s current 2026 market valuation and subtract your primary mortgage balance. Lenders generally permit borrowing up to 80% of your home’s appraised value (Loan-to-Value ratio). Your precise equity position dictates the tier of rates and terms accessible to you.

- Determine Your Debt Service Ratios: Aggregate your monthly debt obligations (credit cards, auto loans, primary mortgage, taxes) against your gross monthly household income. Ensure the addition of a new payment keeps your TDS ratio comfortably below 44%.

- Select Your Rate Type (Fixed vs. Variable): Assess your personal risk tolerance. If you anticipate central bank rate cuts and value flexibility, a variable rate is optimal. If you require absolute budget certainty to sleep at night, secure a fixed rate.

- Choose the Optimal Payment Frequency: Synchronize your mortgage payments with your corporate payroll schedule. If you are compensated bi-weekly, select an accelerated bi-weekly payment to automate your principal reduction without feeling a pinch in your daily liquidity.

- Negotiate Prepayment Privileges: Before executing the contract, scrutinize the lender’s prepayment allowances. Demand “20/20 privileges”—the contractual right to increase your regular payment by 20% and deploy a lump-sum payment of 20% of the original principal annually without triggering penalties.

Before finalizing your strategy, it is highly recommended to review a comprehensive document checklist to guarantee all your financial paperwork supports the specific terms you are requesting from the underwriter.

Prepayment Strategies to Build Equity Faster

Prepayment privileges present Calgary homeowners with lucrative opportunities to optimize their debt structures far beyond the standard amortization schedule. Most competitive lending products include specific prepayment allowances, and strategic timing of these payments maximizes their impact on your outstanding balance.

Early prepayments yield the most dramatic effect on total interest savings because they permanently eliminate the principal balance that would otherwise accrue compounding interest over the remaining years of the loan. Calgary borrowers who receive annual corporate bonuses, substantial tax refunds, or business dividends should immediately deploy these windfalls against their principal.

According to Canada Mortgage and Housing Corporation (CMHC) research, approximately 35% of Canadian borrowers fail to utilize their annual prepayment privileges, effectively leaving thousands of dollars in potential interest savings on the table for the banks to collect.

Elena Rostova, Director of Risk Management at Alberta Financial Group, emphasizes: “Borrowers who fail to utilize their prepayment privileges are artificially extending their debt horizon. Even an additional $100 per month applied directly to the principal can shave years off a standard amortization schedule.” Implementing aggressive principal reduction strategies early in your term is the single most effective methodology for rapid equity accumulation.

Common Pitfalls to Avoid

Even financially literate homeowners can commit structural errors when establishing their financing. Avoiding these common pitfalls will protect your hard-earned equity and preserve your credit rating.

First, many borrowers completely ignore compounding frequency. In Canada, fixed-rate mortgages are legally required to be compounded semi-annually, whereas variable rates are typically compounded monthly. Failing to account for this subtle mathematical difference can silently inflate your debt load.

Second, borrowers frequently overestimate their future earning capacity when committing to aggressively short amortization periods. While a 5-year amortization saves a massive amount of interest, the mandatory monthly payments leave zero margin for financial emergencies. A safer, more strategic approach is to secure a 15-year amortization to mandate lower minimum payments, but utilize your 20/20 prepayment privileges to voluntarily pay the loan off in 5 years.

Finally, failing to compare your financing against alternative vehicles is a critical oversight. Before committing to a specific payment structure, homeowners must evaluate their options against cash-out refinancing to ensure they are utilizing the most cost-effective mechanism for equity extraction. Additionally, if another individual is co-signing the loan, you must fully understand guarantor responsibilities to protect all parties involved.

Conclusion

Structuring your property debt effectively requires a delicate equilibrium between aggressive principal reduction and realistic, sustainable cash flow management. By selecting the optimal payment frequency, matching your rate type to your risk tolerance, and ruthlessly exploiting prepayment privileges, you can transform a standard loan into a highly efficient wealth-building tool. As the 2026 Calgary real estate market continues to evolve, proactive financial structuring remains your best defense against unnecessary borrowing costs.

If you are ready to optimize your home equity strategy and secure the most favorable terms available in the current market, contact our team today for a personalized structural assessment.

Frequently Asked Questions

What factors determine the best payment structure for my property loan?

Your optimal payment structure is dictated by your income stability, existing debt obligations (TDS/GDS ratios), long-term financial goals, and personal risk tolerance. Lenders will rigorously evaluate your Loan-to-Value (LTV) ratio and credit history to determine which payment frequencies and amortization periods you qualify for in 2026.

Can I change my payment frequency after the funds have been disbursed?

Yes, most A-lenders and many alternative institutions in Alberta permit borrowers to modify their payment frequency during the active term. However, you must formally request this change through your lender’s servicing department, and the new frequency must mathematically align with your original amortization schedule.

Are interest-only structures still legally available in 2026?

Yes, interest-only structures remain widely available in Calgary, particularly through private lenders, Mortgage Investment Corporations (MICs), and specialized alternative lenders. They are predominantly utilized by real estate investors, alternative financing for entrepreneurs, or homeowners requiring immediate, short-term cash flow relief.

How do prepayment penalties function on these types of loans?

If you discharge your loan before the contractual term expires, or if you exceed your annual prepayment allowance (e.g., the 20% limit), you will incur a financial penalty. For fixed-rate products, this is typically the greater of three months’ interest or the Interest Rate Differential (IRD), whereas variable rates generally charge a flat three months’ interest.

Does choosing a longer amortization period negatively impact my credit score?

No, selecting a longer amortization period does not inherently damage your credit score. In fact, by securing a lower mandatory monthly payment, you decrease your risk of missing a payment during financial hardships, which actively protects your credit rating over the long term.

Can I use my annual corporate bonus to pay down the principal?

Absolutely. If your loan contract includes standard prepayment privileges, you can apply lump-sum payments (like a corporate bonus or tax refund) directly to the principal balance. This is one of the most effective strategies to bypass compounding interest and shorten your overall amortization timeline.