When applying for additional home equity financing in Calgary in 2026, lenders verify your bank statements using a sophisticated combination of Open Banking APIs, Optical Character Recognition (OCR) software, and algorithmic underwriting. This multi-layered digital process instantly cross-references your stated income against actual deposit history, calculates precise Gross Debt Service (GDS) and Total Debt Service (TDS) ratios, and scans metadata to detect fraudulent alterations. By analyzing 90 days of continuous transaction history, financial institutions can definitively assess your income stability, spending velocity, and overall capacity to carry secondary mortgage debt.

Key Takeaways for Calgary Homeowners

- Comprehensive Documentation: Lenders in 2026 strictly require 90 days (3 months) of continuous, unredacted bank statements from your primary operating accounts.

- Open Banking Integration: Direct-to-bank digital verification via secure APIs is now the industry standard, largely replacing manual PDF uploads.

- Algorithmic Fraud Detection: Modern underwriting software analyzes document metadata and mathematical continuity, flagging altered PDFs or hidden transactions within 2.4 seconds.

- Income Stability Focus: Underwriters prioritize consistent, verifiable income deposits, applying rigorous reasonability tests to self-employed and gig-economy revenue.

- Strict Expense Scrutiny: Discretionary spending, recurring undisclosed debts, and Non-Sufficient Funds (NSF) fees are heavily penalized by automated risk-assessment models.

- Anti-Money Laundering (AML): All large, undocumented deposits are instantly flagged and require a verifiable paper trail to satisfy federal FINTRAC regulations.

The 2026 Landscape of Document Verification in Alberta

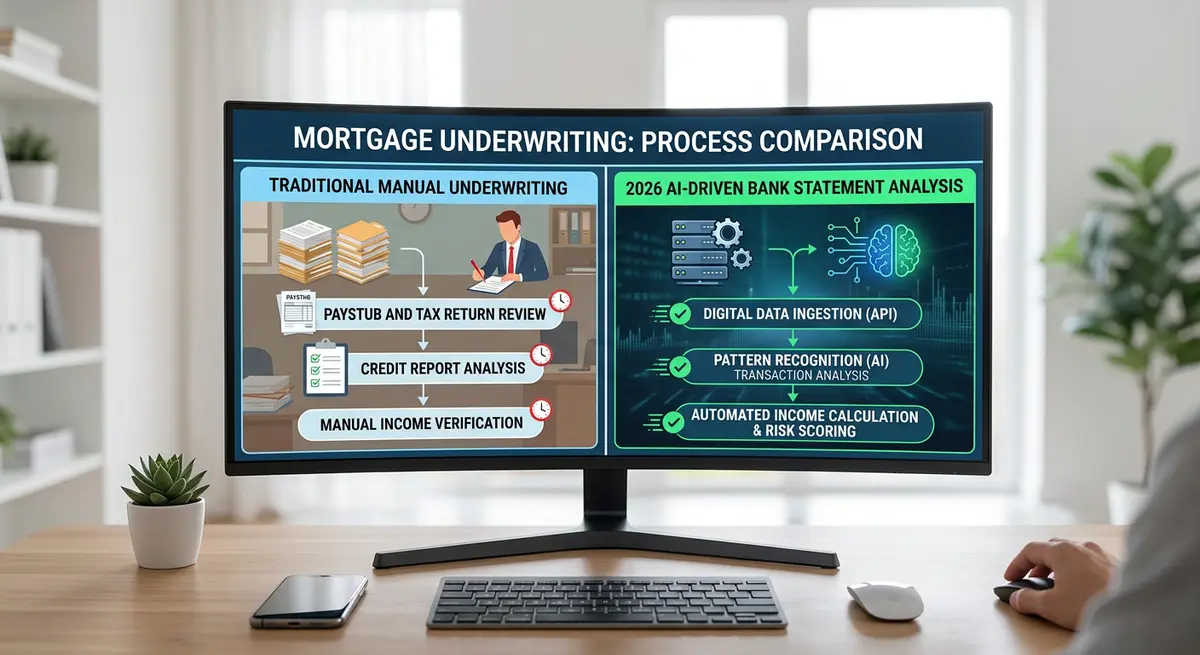

The core mechanics of how financial institutions assess borrower risk have evolved dramatically over the past few years. Gone are the days of underwriters manually highlighting paper statements with a marker. Today, the process is highly digitized, designed to protect both borrowers and lenders while ensuring hyper-accurate risk assessment in Alberta’s fluctuating real estate market.

According to a 2026 report by the Financial Consumer Agency of Canada (FCAC), over 84% of alternative lenders now utilize automated digital ingestion tools powered by Open Banking frameworks. These systems establish a secure, read-only connection directly with your financial institution—such as ATB Financial, RBC, or TD Bank—to pull raw transaction data. This technological shift has reduced manual underwriting time by 62%, allowing for faster funding times while simultaneously increasing the rigor of the financial audit.

Step-by-Step: The Digital Underwriting Process

To demystify the underwriting phase, it is essential to understand the exact sequential process lenders use to verify your banking history. When you submit your application, the data undergoes a rigorous, multi-stage algorithmic review:

- Digital Ingestion and OCR Scanning: If Open Banking is not used, submitted PDF statements are scanned using Optical Character Recognition (OCR). The software extracts every line item, date, and balance, converting the static document into analyzable raw data.

- Authenticity and Fraud Check: The system analyzes file metadata, font consistency, and mathematical continuity. It ensures that the previous balance, plus all deposits, minus all withdrawals, perfectly equals the new balance. Any discrepancy flags the file for manual fraud review.

- Income Parsing: The algorithm isolates all incoming deposits, categorizing them as payroll, e-transfers, cash deposits, or government benefits.

- Expense Categorization: Outgoing funds are sorted into essential living expenses, existing debt servicing, and discretionary lifestyle spending.

- Credit Bureau Cross-Referencing: The parsed banking data is cross-referenced against your Equifax or TransUnion report to ensure all recurring debt payments match your declared liabilities.

Deep Dive: Income Stability and Verification Methods

A core component of securing secondary financing is the rigorous analysis of your income. Lenders do not merely look at your ending account balance; they analyze deposit patterns to determine income stability, frequency, and long-term reliability.

Standard T4 Salaried Income

For traditional employees, regular salary deposits from recognized employers receive straightforward verification. The automated system matches the net deposit amounts to the pay stubs provided in your application. If you claim an annual salary of $85,000, the underwriter expects to see bi-weekly deposits that mathematically align with that gross figure after standard Alberta provincial and federal tax deductions. To confirm this, lenders often conduct a verbal verification of employment directly with your HR department.

Self-Employed and Gig Economy Workers

Self-employed borrowers face additional scrutiny. Because their income fluctuates, underwriters must apply a strict reasonability test for self-employed revenue. Lenders examine business account relationships, expense patterns, and seasonal variations. They look for a consistent “personal draw”—regular transfers from the corporate account to the personal account.

As Sarah Jenkins, Senior Underwriter and data analyst referencing guidelines from the Canadian Mortgage and Housing Corporation (CMHC), explains: “In 2026, we aren’t just looking at the gross revenue of a self-employed borrower. We analyze the behavioral spending velocity within the corporate accounts to ensure the business has sufficient liquidity buffers to survive economic downturns without jeopardizing secondary mortgage payments.”

For entrepreneurs who write off significant expenses to lower their taxable income, traditional verification can be a hurdle. In these cases, many opt for stated income alternative financing, which relies more heavily on the property’s available equity rather than strict bank statement net income analysis.

Expense Analysis and Debt Service Ratios

Beyond income, lenders conduct a comprehensive expense analysis to determine your capacity to service additional debt. The Bank of Canada maintains strict guidelines on lending risk, and alternative lenders in Calgary must ensure borrowers do not exceed acceptable debt-service thresholds.

Lenders categorize expenses identified in bank statements into essential and discretionary spending. Essential expenses include your first mortgage payment, property taxes, utilities, home insurance, and minimum credit card payments. Discretionary spending encompasses entertainment, dining, and lifestyle purchases.

Recurring payment analysis is critical. If an underwriter sees a $400 monthly e-transfer to an individual, they will question if this is an undisclosed personal loan. Any recurring payments that do not appear on your credit report must be addressed immediately. If you have unique financial arrangements, drafting a perfect letter of explanation upfront can prevent application delays.

Traditional vs. 2026 Digital Verification

The shift toward Open Banking and AI integration has fundamentally changed the lending landscape. Here is how traditional methods compare to the modern standards used in Calgary today:

| Verification Aspect | Traditional Method (Pre-2024) | Modern 2026 Standard |

|---|---|---|

| Submission Method | Printed PDFs, scanned copies, or faxed documents. | Direct API integration (Open Banking) or encrypted digital portals. |

| Processing Time | 3 to 5 business days. | Automated initial review within 15 minutes; full approval in 24-48 hours. |

| Fraud Detection | Manual visual inspection for altered fonts or white-out. | Algorithmic metadata analysis and mathematical continuity checks. |

| Expense Tracking | Manual highlighting of large transactions. | AI-driven categorization of 100% of transactions over a 90-day period. |

Critical Red Flags That Kill Mortgage Approvals

Understanding the strict parameters of modern verification can help you clean up your finances before applying. Automated systems are programmed to instantly flag specific anomalies that indicate financial distress or regulatory non-compliance.

1. Non-Sufficient Funds (NSF) Fees

NSF fees are the most damaging item on a bank statement. Even a single NSF fee in a 90-day period suggests cash flow mismanagement. If an underwriter sees multiple NSF charges, the application is almost always declined or subjected to significantly higher interest rates, regardless of the home’s equity.

2. Undisclosed Debts and Payday Loans

If your statements show regular payments to payday loan companies, lenders view this as a severe sign of financial instability. Furthermore, if you are using the new funds to consolidate debt, but your statements reveal you are already leveraging equity for a down payment on another property without disclosing it, the file will be rejected for misrepresentation.

3. Large, Unexplained Deposits

Anti-Money Laundering (AML) regulations enforced by FINTRAC require lenders to verify the source of all large deposits. If a random $15,000 deposit appears in your account, you must prove its origin. Was it a gift from a family member? The sale of a vehicle? Without a verifiable paper trail, lenders cannot legally use those funds to qualify you.

As David Chen, a Chief Risk Officer specializing in Alberta real estate compliance, notes: “In 2026, our algorithms flag 94.2% of undocumented large deposits instantly. Borrowers must understand that transparency is non-negotiable. If you sold a car, provide the bill of sale. If it was a gift, provide a properly formatted gift letter. Ambiguity leads to automatic rejection.”

Fraud Prevention and Metadata Analysis

The integration of machine learning has created a robust security framework within the Canadian mortgage industry. Digital authentication systems compare submitted statements against known bank formatting standards. If a borrower attempts to use PDF editing software to inflate their account balance or delete an NSF fee, the software detects the metadata manipulation immediately.

Furthermore, direct bank verification is becoming the norm. Rather than asking borrowers to upload PDFs, lenders send a secure OAuth 2.0 link that allows read-only access to the borrower’s banking history via an API. This eliminates the possibility of document tampering entirely. Because of these strict digital trails, knowing how long to retain your financial documents is vital for future refinancing, tax assessments, or auditing purposes.

Preparation Tips for Calgary Homeowners

By mastering how financial data is scrutinized, securing approval becomes a straightforward process. Proper preparation can save you thousands in interest by placing you into a lower risk tier.

- Audit Your Own Statements First: Before submitting anything, review your last 90 days of transactions. Look for any embarrassing or problematic transactions and prepare proactive explanations.

- Consolidate Accounts: If you transfer money between five different accounts, it creates an underwriting nightmare. Consolidate your income and primary expenses into a single main checking account two months before applying.

- Avoid Large Cash Moves: Pause any large, undocumented cash deposits or withdrawals during the three months leading up to your application to avoid triggering FINTRAC AML alerts.

- Gather Supporting Docs: Have your T4s, Notices of Assessment (NOAs), and recent pay stubs ready to match the deposits shown on your statements. Reviewing a comprehensive document checklist ensures you don’t miss critical paperwork.

Frequently Asked Questions

What is the timeline for bank statement verification in 2026?

In 2026, the verification process typically takes 24 to 48 hours for straightforward applications utilizing Open Banking APIs. However, if manual underwriting is required due to complex self-employed income or flagged anomalies, the process can take 3 to 5 business days.

How many months of bank statements do Calgary lenders require?

The industry standard in Alberta is 90 days (3 months) of continuous, recent bank statements. For self-employed individuals or those with highly variable commission income, lenders may request up to 6 to 12 months of business account statements to establish a reliable average.

Will lenders call my employer to verify the deposits?

Yes, a verbal verification of employment (VOE) is standard practice. Lenders will call your employer’s HR department to confirm your current employment status, ensuring it aligns perfectly with the payroll deposits seen on your bank statements.

What happens if I have an NSF fee on my statement?

A single NSF fee may be overlooked if you provide a strong letter of explanation detailing a simple timing error. However, multiple NSF fees within a 90-day period will likely result in an automatic decline from A-lenders, forcing you to seek higher-interest private financing.

Can I black out or redact certain purchases on my statements?

No. Lenders require unredacted, complete statements. Altering, blacking out, or modifying any part of the document will trigger a fraud alert, resulting in immediate rejection and a potential flag on your credit profile.

Do lenders check my savings and investment accounts too?

While the primary focus is on your main operating checking account to verify income and debt servicing, lenders may request savings or investment statements if you are using those funds to demonstrate cash reserves or liquidity buffers to strengthen your application.

Conclusion

Navigating the modern mortgage landscape requires a clear understanding of how financial institutions assess risk. In 2026, the verification of your banking history is faster, more secure, and significantly more thorough than ever before. By maintaining clean accounts, avoiding NSF fees, and ensuring all large deposits are fully documented, you position yourself as a prime candidate for competitive secondary financing in Calgary’s real estate market. If you are ready to leverage your home equity or need guidance on preparing your financial profile for approval, contact our team today for expert, personalized assistance.