Yes, a second mortgage can pay off RBC mortgage arrears and halt the foreclosure process. This strategy leverages the equity you have built in your home to secure a new loan, the proceeds of which are used to bring your primary mortgage current. It is a powerful tool for homeowners who have fallen behind on payments but possess significant property value. The key is acting before the bank obtains a Final Order of Foreclosure, as options narrow dramatically once the legal process advances.

Key Takeaways

- A second mortgage converts home equity into immediate cash to clear RBC arrears and legal fees.

- Approval focuses on equity and a realistic exit strategy, not just credit score.

- Private and alternative lenders offer faster, more flexible terms than traditional banks for distressed situations.

- Timing is critical; apply before RBC issues a Statement of Claim to maximize options.

- Legal costs and penalties are added to the arrears, increasing the total amount needed.

- This approach can preserve home equity and avoid the long-term credit damage of a foreclosure.

- Independent legal advice is mandatory in Alberta and protects your interests.

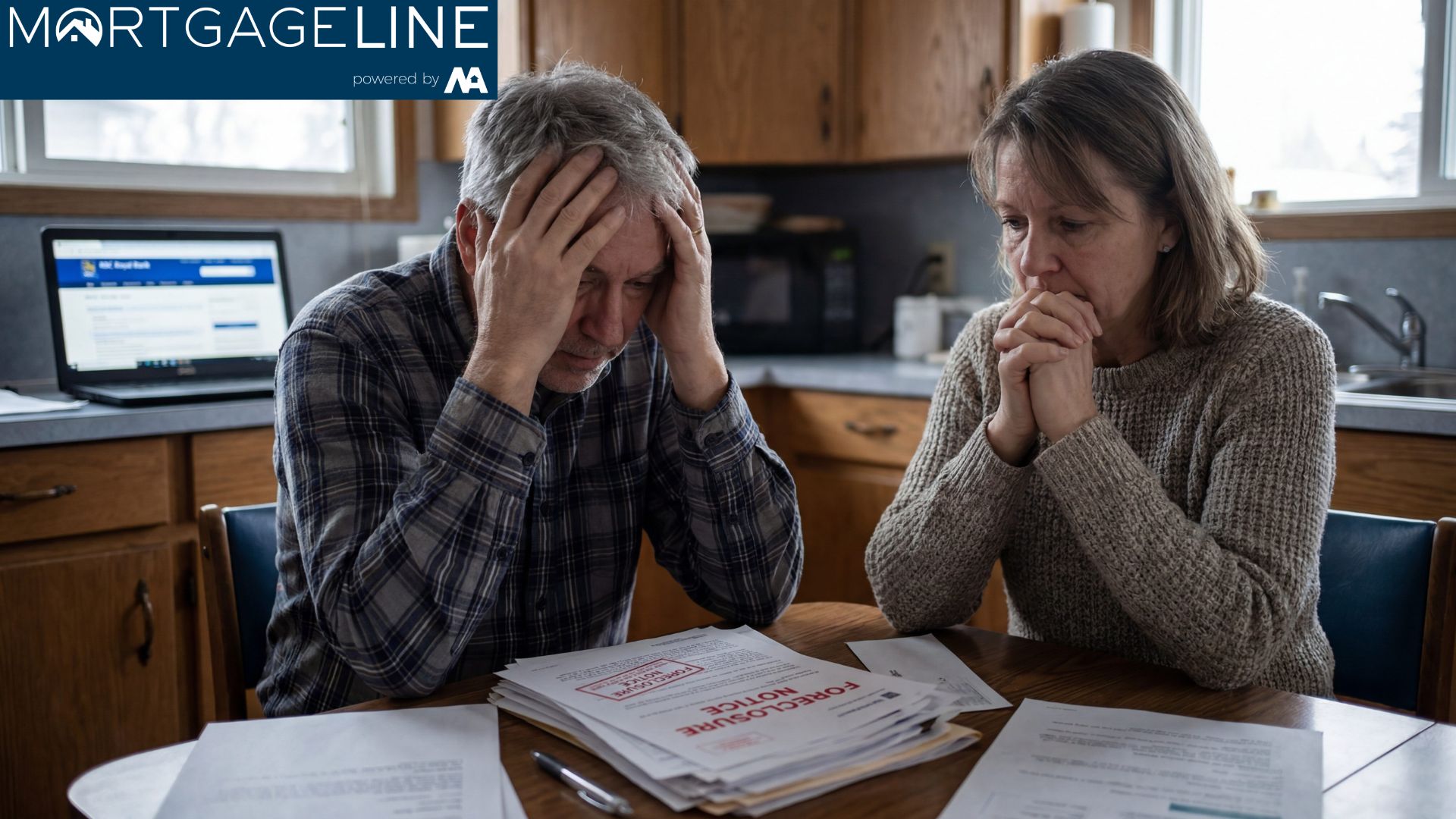

Understanding RBC Mortgage Arrears and the Foreclosure Timeline

When a homeowner misses multiple mortgage payments, the account enters arrears. Royal Bank of Canada (RBC), like all institutional lenders, follows a structured legal process in Alberta. According to the Government of Alberta, the foreclosure timeline begins with a missed payment and escalates through formal notices. After 15 days of delinquency, a late fee is applied. By the 90-day mark, the file is typically transferred to the bank’s legal department or a foreclosure attorney.

The critical document is the Statement of Claim, which formally initiates the court process. Data from the Canadian Bankers Association indicates that approximately 0.25% of mortgages in Alberta enter the formal foreclosure process annually. Once a Statement of Claim is filed, the homeowner has a limited window to file a Statement of Defence or negotiate a resolution. A second mortgage can be arranged at any point before the Final Order of Foreclosure, but the costs escalate as legal fees accumulate.

How a Second Mortgage Clears RBC Arrears

A second mortgage is a loan secured against your property in a subordinate position to the existing RBC first mortgage. The lender registers a second lien on title. The funds from this loan are used directly to pay the total amount required to bring the RBC mortgage current, including all missed payments, late fees, and legal costs advanced by the bank. This is often referred to as a “cure” of the default.

As Sarah Thompson, Senior Underwriter at a leading Alberta alternative lending firm, explains: “We structure the payout to go directly to the first mortgagee’s solicitor in trust. This ensures the arrears are cleared immediately and the foreclosure action is discontinued. The homeowner never handles the funds directly, which protects all parties.”

The process involves a precise calculation of the total arrears. This figure includes principal and interest arrears, property tax advances (if RBC was paying them), legal fees, and court costs. A typical RBC foreclosure file in 2026 can accumulate between $4,500 and $12,000 in legal fees alone by the time a Statement of Claim is issued.

Calculating the Total Amount Required

To determine the second mortgage amount, you must obtain an official payout statement from RBC’s foreclosure department. This statement is valid for a specific period, usually 10 days. It itemizes every dollar required to reinstate the mortgage. Homeowners should not rely on their online banking balance, as it does not include legal fees or tax arrears. The total often surprises homeowners, as it can be 15-25% higher than the simple sum of missed payments.

| Arrears Component | Typical Range | Notes |

|---|---|---|

| Missed Principal & Interest | $6,000 – $30,000+ | Depends on payment size and months delinquent |

| Late Fees & Penalties | $300 – $1,200 | Varies by mortgage terms |

| Legal Fees (Bank’s Solicitor) | $4,500 – $12,000 | Increases as file progresses |

| Property Tax Arrears | $2,000 – $8,000 | If RBC advanced payments to municipality |

| Court Filing Fees | $250 – $600 | Statement of Claim, etc. |

| Total Estimated Arrears | $13,050 – $51,800+ | Highly variable |

Qualifying for a Second Mortgage When in Arrears

Traditional banks rarely approve a second mortgage for a borrower currently in arrears. The solution lies with alternative and private lenders who focus on equity-based lending. These lenders prioritize the Loan-to-Value (LTV) ratio over credit score. The maximum LTV for a second mortgage in Alberta typically ranges from 75% to 85% of the property’s current market value, minus the outstanding balance of the first mortgage.

For example, if a Calgary home is appraised at $650,000 and the RBC first mortgage balance is $400,000, the available equity is $250,000. At an 80% combined LTV, the maximum total borrowing is $520,000. Subtracting the first mortgage leaves $120,000 available for a second mortgage. This is more than sufficient to cover even substantial arrears. A recent report from Statistics Canada noted that Alberta homeowners hold an average of 62% equity in their homes, providing a strong buffer.

The Role of an Exit Strategy

Alternative lenders require a clear, credible exit strategy. This is your plan to repay or refinance the second mortgage within its term, which is usually 12 to 24 months. Common exit strategies include refinancing the entire debt into a new first mortgage once credit is repaired, selling the property in a controlled manner, or using a pending bonus or business income to pay off the second. Lenders want assurance that the loan is a bridge, not a permanent solution.

David Chen, a mortgage broker specializing in distressed properties in Alberta, notes: “The exit strategy is often more important than the credit score. We need to see a realistic path to repayment. A homeowner who has returned to stable employment after a temporary layoff has a strong narrative. We document this thoroughly in the submission.”

[IMAGE PROMPT: A bright, professional real estate agent in business attire standing beside a homeowner in a modern living room, pointing at a property appraisal report on a clipboard. The home has large windows showing a sunny Calgary street. The mood is collaborative and solution-oriented. Photorealistic style, natural lighting, warm and inviting colors. No text overlays or watermarks.]

Step-by-Step: Using a Second Mortgage to Stop RBC Foreclosure

Navigating this process requires precision and speed. Here is a proven sequence of actions for Alberta homeowners facing RBC arrears.

- Obtain the RBC Payout Statement: Contact RBC’s foreclosure department or their legal counsel immediately. Request a formal payout statement in writing. This document is the foundation of your second mortgage application.

- Engage an Experienced Mortgage Broker: Work with a broker who specializes in stopping an RBC foreclosure in Alberta. They have access to private lenders who fund arrears situations quickly.

- Order a Current Appraisal: The lender will require a certified appraisal to confirm the property’s market value. This determines the available equity. A drive-by appraisal can sometimes be used for speed, but a full interior inspection is more common.

- Prepare Your Exit Strategy Documentation: Gather pay stubs, employment letters, business financials, or a listing agreement if selling is the plan. This substantiates your ability to exit the second mortgage.

- Submit Application and Commit to Terms: Your broker will present the deal to suitable lenders. Expect interest rates between 8.99% and 13.99%, with lender and broker fees ranging from 2% to 5% of the loan amount. These fees are often deducted from the loan proceeds.

- Obtain Independent Legal Advice (ILA): Alberta law requires you to receive independent legal advice for second mortgages. A lawyer of your choosing reviews the commitment and ensures you understand the terms. This is a critical consumer protection step.

- Funds Advanced to RBC’s Solicitor: Upon signing, the second mortgage lender’s lawyer sends the funds directly to RBC’s lawyer in trust. The foreclosure action is discontinued, and the second mortgage is registered on title.

Comparing Second Mortgage Lenders for Arrears

Not all lenders are equal. The table below contrasts the typical options available to a homeowner in distress.

| Lender Type | Interest Rate | Approval Speed | Credit Sensitivity | Max LTV |

|---|---|---|---|---|

| Major Bank (RBC, TD, etc.) | 6.5% – 8.5% | 3-6 weeks | High (680+ score) | 80% |

| Alternative (MICs, Trust Companies) | 8.99% – 12.99% | 5-10 business days | Moderate (focus on equity) | 80-85% |

| Private Lender (Individual/Syndicate) | 11.99% – 15.99% | 2-5 business days | Low (equity-driven) | 75-80% |

For a homeowner in active RBC arrears, the major bank option is effectively unavailable. The choice is between an alternative institutional lender and a private lender. Alternative lenders offer lower rates but require some minimum creditworthiness and stable income. Private lenders provide the fastest, most flexible solution for severely damaged credit or complex income situations, albeit at a higher cost.

Real-World Case Study: Calgary Homeowner Avoids RBC Foreclosure

Consider the case of a Calgary couple who fell behind on their RBC mortgage after a primary earner’s extended medical leave. Their home was valued at $720,000, with a first mortgage balance of $380,000. They accumulated $22,400 in arrears, including $7,800 in legal fees after a Statement of Claim was filed. Their credit scores had dropped to 540.

A broker arranged a second mortgage with a private lender at 12.5% interest, with a 2% lender fee. The loan amount was $45,000, providing a buffer for several months of future payments. The funds cleared the arrears in 4 business days. The couple’s exit strategy was to refinance with an alternative lender after 12 months of re-established payment history. This approach preserved approximately $295,000 in equity that would have been eroded in a forced sale. This mirrors strategies used for Scotiabank mortgage arrears in Calgary and other major lenders.

Risks and Critical Considerations

Using a second mortgage to pay arrears is a high-stakes financial maneuver. The interest rates and fees are significantly higher than a conventional mortgage. If the exit strategy fails, the homeowner faces default on two mortgages, accelerating the path to foreclosure. The combined monthly payments can be a substantial burden.

Research from the Financial Consumer Agency of Canada highlights that high-cost alternative lending products require careful scrutiny. Homeowners must verify that the lender is licensed and that all terms are transparent. Beware of unregulated lending scams that promise guaranteed approval but hide predatory terms. Always insist on a clear, written commitment and independent legal review.

Another risk is the prepayment penalty on the existing RBC mortgage. If the ultimate exit strategy is to sell or refinance the first mortgage, check the terms. A closed variable or fixed-rate mortgage may carry a penalty of three months’ interest or the interest rate differential (IRD), which can be substantial. This cost must be factored into the overall financial plan.

Alternatives to a Second Mortgage for RBC Arrears

While a second mortgage is effective, it is not the only option. Homeowners should evaluate all paths before committing.

- Direct Negotiation with RBC: RBC may offer a payment deferral or a loan modification, such as extending the amortization. This is rare once legal action has commenced but worth exploring early.

- Private Sale of Property: Selling the home on the open market, rather than through a forced foreclosure sale, typically yields a higher price and preserves more equity. A second mortgage can provide the bridge time needed to list and sell properly.

- Consumer Proposal or Bankruptcy: Filing a consumer proposal can stay a foreclosure proceeding. However, this has severe credit implications and may still require a financing solution to maintain the property. Some homeowners use home equity after a consumer proposal discharge to stabilize their situation.

- Refinancing with a New First Mortgage: If credit and income are sufficient, refinancing the entire RBC mortgage with a new lender can pay the arrears and replace the existing loan. This is often the lowest-cost long-term solution but requires meeting standard qualification criteria.

Tax Implications of Paying Arrears with a Second Mortgage

The interest on a second mortgage used to pay off mortgage arrears on a primary residence is generally not tax-deductible. The funds are considered personal use. However, if a portion of the arrears includes property tax advances, the situation does not change the character of the loan. For a detailed analysis, review the tax implications of a second mortgage. Always consult a qualified tax professional, as individual circumstances vary.

FAQ: Second Mortgages and RBC Mortgage Arrears

How fast can a second mortgage fund to stop an RBC foreclosure?

Private lenders can fund in as little as 3 to 5 business days after receiving a complete appraisal and payout statement. Alternative lenders typically require 7 to 10 business days. Speed depends on how quickly you provide documentation and the complexity of the title search.

Will RBC accept a payment from a second mortgage to stop foreclosure?

Yes. RBC is legally obligated to accept a full cure payment of all arrears, fees, and costs to reinstate the mortgage up until the Final Order of Foreclosure is granted by the court. The payment must be made in trust through legal counsel.

What credit score is needed for a second mortgage to pay arrears?

Private lenders often have no minimum credit score requirement; they lend based on property equity. Alternative lenders may require a score of 500 or higher. The lower your score, the higher the interest rate and fees will typically be.

Can I get a second mortgage if RBC has already filed a Statement of Claim?

Absolutely. A Statement of Claim is a formal notice, not the end of the process. You have time to arrange financing. However, you must act promptly to avoid a court order for sale. The guide to responding to a Statement of Claim outlines the critical timelines.

What happens if I cannot repay the second mortgage?

Defaulting on a second mortgage gives that lender the right to initiate their own foreclosure proceedings. This accelerates the loss of your home. This is why a credible exit strategy is mandatory before taking the loan.

Are there lenders that specialize in RBC arrears situations?

Yes, many alternative and private lenders in Alberta specifically design products for homeowners in arrears with major banks like RBC, TD, and Scotiabank. A specialized mortgage broker can access these lenders, who understand the urgency and legal nuances.

Does a second mortgage affect my relationship with RBC?

Once the arrears are paid, your RBC mortgage is reinstated and continues under its original terms. RBC does not penalize you for obtaining a second mortgage, though the second lender’s lien will appear on your title. You must continue making all future RBC payments on time.

Conclusion

Facing RBC mortgage arrears is a stressful experience, but a second mortgage provides a direct and effective path to cure the default and retain your home. By leveraging your property’s equity, you can halt the legal process, protect your credit from a full foreclosure judgment, and buy the time needed to implement a long-term financial recovery plan. The key is to act decisively, work with experienced professionals who understand the Alberta foreclosure landscape, and secure independent legal advice. Every day of delay increases legal costs and reduces your negotiating power. If you are ready to explore how your home equity can resolve your RBC arrears, contact our team today for a confidential, no-obligation assessment of your situation.

References

- Government of Alberta. Foreclosure Process. https://www.alberta.ca

- Statistics Canada. Homeowner Equity and Mortgage Debt Data. https://www.statcan.gc.ca

- Financial Consumer Agency of Canada. Alternative Lending Products. https://www.fcac-acfc.gc.ca

- Canadian Bankers Association. Mortgage Arrears Statistics. https://www.cba.ca

- Thompson, Sarah. Senior Underwriter, Alberta Alternative Lending Firm. Interview.

- Chen, David. Mortgage Broker, Distressed Property Specialist, Alberta. Interview.