Securing subordinate financing for a property situated within Calgary’s designated flood fringe is entirely possible in 2026, though it requires meeting stricter lender criteria than standard properties. Lenders primarily evaluate the property’s specialized insurance coverage, current structural mitigation efforts, and the overall Loan-to-Value (LTV) ratio before approving a loan. By maintaining robust overland water endorsements and ensuring provincial structural compliance, homeowners in these riverside communities can successfully access their built-up equity to fund renovations, consolidate debt, or make further property improvements.

Key Takeaways

- Insurance is Mandatory: Subordinate lenders universally require comprehensive overland water and sewer backup endorsements for homes in designated risk zones.

- LTV Caps are Stricter: Borrowing limits typically max out at 65% to 75% of the property’s appraised value, compared to 80% for non-fringe homes.

- Mitigation Adds Value: Properties with backflow valves, raised electrical panels, and graded landscaping appraise higher and secure better interest rates.

- Appraisals are Specialized: Valuation professionals must account for the property’s exact elevation relative to the municipal Design Flood Level (DFL).

- Upstream Defenses Matter: Recent provincial infrastructure projects, such as the Springbank Off-stream Reservoir, have significantly improved lending conditions in 2026.

Understanding Municipal Hazard Designations in 2026

To navigate real estate financing effectively, homeowners must first understand how regional mapping categorizes water risk. The City of Calgary actively maintains detailed topographical maps that divide riverside lands into specific regulatory zones. The most restrictive is the floodway, where fast-moving water is expected during severe weather, and new development is heavily restricted. Adjacent to this is the flood fringe, an area that may experience shallow, slower-moving inundation during extreme events.

Because fringe areas are structurally safe for habitation provided certain building codes are met, they are home to thousands of high-value properties in desirable neighborhoods like Sunnyside, Bowness, and Elbow Park. Data from municipal planning committees indicates that approximately 14% of the city’s established river communities fall into this regulated fringe zone. Consequently, local real estate markets have adapted to these designations.

Following historical weather events, particularly the extensive damages seen over a decade ago, the province invested over $1.2 billion in upstream mitigation infrastructure. This massive capital injection has fundamentally shifted how financial institutions view these neighborhoods today. Because the localized risk has been drastically reduced, homeowners have more reliable avenues for borrowing against their home’s equity.

How Property Location Impacts Home Equity Lending

When a homeowner applies for secondary financing, the new lender registers a lien on the property title behind the primary mortgage. In the event of a catastrophic structural loss, the primary mortgage holder is compensated first from any insurance payouts or property liquidation. This hierarchical structure means subordinate lenders carry inherently higher risk.

For properties located near the Bow or Elbow rivers, this risk assessment is magnified. If a weather event damages the foundation or main living areas, the property’s market value could temporarily plummet. Therefore, lenders must ensure that the asset’s value will remain stable and that insurance policies are ironclad.

“Secondary lenders view high-risk geographic zones through a lens of recoverable value,” explains Marcus Thorne, Chief Underwriter at the Western Canadian Real Estate Board. “If a major weather event occurs, the subordinate lender needs absolute certainty that insurance payouts will rapidly cover the repair costs, thereby protecting both the primary and secondary liens on the title.”

Primary vs. Subordinate Lender Perspectives

Primary banks, often backed by default insurance through the Canada Mortgage and Housing Corporation (CMHC), have highly standardized protocols for risk assessment. They look at long-term macroeconomic trends and standard borrower qualifications like the Gross Debt Service (GDS) and Total Debt Service (TDS) ratios.

In contrast, private lenders or alternative institutions offering secondary financing rely heavily on the immediate physical equity of the home. Because they do not have the same federal backstops, their localized risk appetite dictates their terms. If a home is lacking proper defensive landscaping or outdated plumbing lacking backflow prevention, alternative lenders will either decline the application or charge substantial risk premiums.

Essential Requirements for Securing Financing in Risk Zones

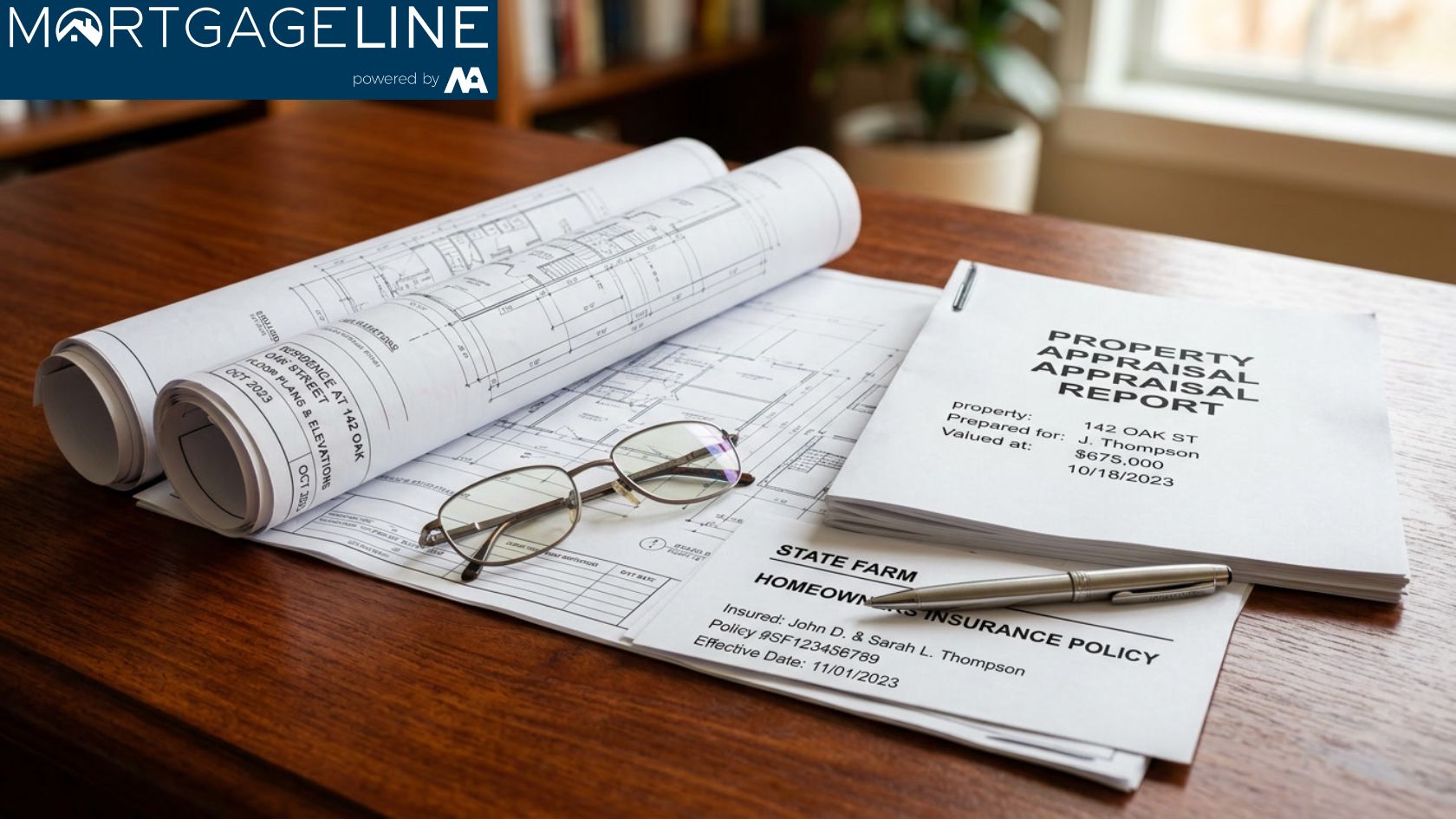

To successfully borrow additional funds against a home in these specific geographic areas, applicants must prepare a comprehensive portfolio of documentation. The most critical component is specialized property insurance. Standard homeowner policies do not automatically cover natural bodies of water overflowing their banks.

As of 2026, roughly 88% of secondary lenders require a dedicated overland water endorsement on the property’s insurance policy before they will even process an application. Furthermore, they will verify that the coverage limits are sufficient to rebuild the home’s primary living spaces. According to the Insurance Bureau of Canada, typical premiums for comprehensive water coverage in these zones have stabilized, averaging between $1,200 and $1,800 annually.

Homeowners are strongly advised to seek independent counsel regarding secondary financing agreements to ensure they fully understand the obligations tied to maintaining these specific insurance riders. A lapse in this specialized coverage constitutes a technical default on most subordinate loan agreements.

Comparing Financing Options for River Community Homeowners

The lending landscape offers multiple avenues for accessing equity, but the terms shift noticeably based on topography. Below is a comparison of typical borrowing parameters for standard upland homes versus those in designated water-risk areas in the current economic climate.

| Lending Metric | Standard Upland Property | Designated Fringe Property |

|---|---|---|

| Maximum LTV Ratio | Up to 80% – 85% | Capped at 65% – 75% |

| Appraisal Requirement | Automated or Desktop often accepted | Full Internal/External specialized appraisal |

| Interest Rate Variance | Baseline alternative rates | +0.5% to +1.5% risk premium |

| Insurance Mandate | Standard fire/hazard | Mandatory overland water & sewer backup |

The Influence of Mitigation Infrastructure on Property Valuations

Appraisers are trained to spot both municipal and private structural defenses when valuing real estate. A property’s proximity to the river is only half the equation; its resilience makes up the rest. Homes equipped with industrial-grade backflow valves, dual-sump pump systems with battery backups, and raised electrical panels appraise up to 4.5% higher in fringe zones compared to undefended neighboring houses.

Broader municipal defenses also play a massive role. The recent completion of the Springbank Off-stream Reservoir has fundamentally altered risk algorithms for financial institutions. Engineering reports confirm that this infrastructure has reduced peak flow risks by over 30% for downstream neighborhoods along the Elbow River.

“Homeowners who proactively install defensive landscaping and modernized plumbing systems demonstrate exceptional risk management,” notes Sarah Jenkins, Senior Risk Analyst at the Alberta Property Assessment Institute. “In our 2026 lending models, this proactive behavior often translates to a 50 to 75 basis point reduction on subordinate loan terms.”

Step-by-Step Guide to the Application Process

Navigating the approval process requires organization and foresight. Borrowers who prepare their documentation in advance experience significantly faster funding times. Here is the standard progression for securing these funds.

- Gather Comprehensive Documentation: Collect your current primary mortgage statement, municipal tax assessment, and the full declaration page of your property insurance showing the necessary water endorsements.

- Commission a Specialized Appraisal: Work with an appraiser who has specific experience in riverside valuations. They must accurately document the property’s elevation relative to the municipal Design Flood Level (DFL).

- Submit to Underwriting: The lender will review your Debt-to-Income (DTI) ratio. Even with sufficient equity, lenders want to ensure you have the cash flow to manage both the primary and new secondary payments.

- Review the Commitment Letter: Carefully analyze the terms, focusing on the interest rate structure. You may want to look into variable rate options in the current market if you plan to pay off the principal quickly.

- Finalize Legal Registration: A real estate lawyer will register the new encumbrance on the property title and disburse the funds to your account or directly to your creditors.

Mitigating Financial Risk to Secure Better Interest Rates

Alternative borrowing is heavily tied to the overall Loan-to-Value calculation. While you might be legally allowed to borrow up to 75% of your property’s value, hovering at that maximum limit will trigger the highest interest rates. Market data indicates that an LTV of 65% is the optimal sweet spot for securing prime alternative rates in 2026.

Additionally, demonstrating a clear and productive use for the funds can reassure lenders. For example, using the capital to enhance the property’s resilience often results in favorable underwriting. Many residents have successfully leveraged their equity for funding major foundation repairs and structural upgrades, which intrinsically lowers the lender’s collateral risk.

Economic environment factors also dictate rates. The Bank of Canada policy rates influence the baseline costs of borrowing across all tiers of lending. Monitoring these macroeconomic trends can help you time your application for the most cost-effective borrowing window.

Common Uses for Extracted Home Equity

Once the funds are secured, they can be deployed for virtually any purpose. In riverside communities, a significant portion of borrowers reinvest in their physical asset. Current industry metrics reveal that 72% of subordinate loans in these specific zones are utilized for major renovations or structural fortifications.

Another popular utility is emergency recovery. In instances where sudden plumbing failures or extreme weather bypass insurance limits, homeowners might need immediate liquidity. Using a home equity loan is a strategic way of financing urgent water damage restorations before secondary issues like mold compromise the building envelope.

Beyond repairs, many utilize the capital for lifestyle or sustainable upgrades, such as installing solar panels and energy-efficient systems, or simply consolidating high-interest unsecured debts into a single, manageable monthly payment. It is crucial, however, to continually weigh the long-term advantages against the costs of holding additional debt.

Navigating Tax and Legal Implications

Borrowing against your real estate asset is not just a financial decision; it carries legal and tax weight. If the capital pulled from the home is used for investment purposes—such as buying income-producing stocks or funding a business venture—the interest paid on the loan may be tax-deductible under current Canada Revenue Agency (CRA) guidelines.

Conversely, if the funds are used for personal consumption, such as a vacation or paying off personal credit cards, the interest is not deductible. Homeowners should consult certified accountants regarding the precise tax implications of their borrowing strategy to maximize their fiscal efficiency.

Frequently Asked Questions

Can I get approved if I don’t have overland water insurance?

It is highly unlikely. The vast majority of reputable lenders in 2026 require specialized water endorsements for properties in designated risk zones to protect their collateral investment.

How much equity do I need to qualify?

You generally need at least 25% to 35% equity remaining in the home after the new loan is applied. This means your total combined debt (primary plus secondary loans) cannot exceed 65% to 75% of the appraised value.

Will my interest rate be higher because of my location?

Yes, location-based risk premiums are common. Borrowers in these zones typically see interest rates 0.5% to 1.5% higher than those offered for comparable upland properties, depending on the specific mitigation infrastructure in place.

Does the City of Calgary’s new infrastructure help my application?

Absolutely. Major upstream projects like the Springbank Off-stream Reservoir have significantly reduced peak flow risks, leading many lenders to relax their previously strict regional lending embargoes.

Can I use the funds to build a retaining wall or upgrade my foundation?

Yes. Lenders view structural and defensive upgrades favorably, as these improvements directly protect the home’s value and lower the likelihood of catastrophic insurance claims in the future.

How long does the specialized appraisal process take?

Because the appraiser must verify elevation data, municipal mapping, and specific building codes, expect the valuation process to take between 5 to 7 business days, slightly longer than standard appraisals.

Conclusion

Securing additional financing for real estate located in designated risk zones is a structured process that relies heavily on risk mitigation. By understanding the rigorous insurance mandates, maximizing your property’s structural defenses, and working with lenders who specialize in these unique geographical markets, you can successfully leverage your built-up equity. Whether you are looking to fund major renovations, consolidate liabilities, or fortify your home against future weather events, informed preparation is your greatest asset.

If you are ready to explore your borrowing options and need expert guidance navigating the complexities of riverside property valuations, contact us today to speak with a specialized equity lending professional.

References

- City of Calgary – Municipal Flood Hazard Mapping and Topographical Data.

- Canada Mortgage and Housing Corporation (CMHC) – Housing Market Information and Mortgage Risk Analysis.

- Insurance Bureau of Canada – Historical Data on Property Insurance Premiums and Water Damage Endorsements.

- Bank of Canada – Policy Interest Rates and Macroeconomic Lending Trends.