Comparing secondary lenders requires a systematic evaluation of interest rates, loan-to-value (LTV) maximums, administrative fees, and repayment flexibility. To secure the most favorable terms in 2026, homeowners must analyze the total cost of borrowing rather than just the advertised introductory rate, ensuring the new loan aligns with their long-term financial objectives without jeopardizing their primary property agreement.

Key Takeaways

- Total Cost Analysis: Always calculate the combination of interest rates, legal fees, and administrative costs, which typically range from 1.5% to 3% of the loan amount.

- LTV Limits: Most institutions cap combined borrowing at 80% to 85% of your property’s current appraised value.

- Lender Types: Traditional banks offer lower rates (averaging 5.8% to 7.5%) for prime credit, while alternative lenders provide faster funding with more flexible approval criteria.

- Rate Structures: Fixed terms offer payment stability, whereas variable rates (often Prime + 1.1%) can provide savings if the Bank of Canada reduces benchmark rates.

- Strategic Negotiation: Presenting competing offers can frequently result in waived appraisal fees or rate reductions of up to 0.25%.

Understanding Home Equity Financing in the Current Market

Property owners frequently seek ways to tap into their residence’s accumulated value to fund significant life events, from major renovations to debt consolidation. A secondary loan allows you to borrow against this built-up equity while leaving your original, often lower-rate, primary loan entirely intact. This financial instrument sits behind your first agreement in priority, meaning the primary institution is paid first in the event of a default.

According to recent housing data from the Canada Mortgage and Housing Corporation (CMHC), property values in major Albertan markets have seen steady appreciation, creating substantial equity reserves for long-term owners. This growth allows homeowners to access larger lump sums. However, leveraging this asset requires a thorough understanding of how lenders calculate risk and determine your borrowing capacity.

Decoding Loan-to-Value (LTV) Ratios

The Loan-to-Value ratio is the primary metric financial institutions use to assess the risk of lending against your property. It compares the total amount of debt secured against the house to its current market value. In 2026, most conservative lenders cap the combined LTV at 80%, though some alternative providers may extend this to 85% for well-qualified applicants.

| Appraised Home Value | Existing Primary Debt | Available Equity | Max Additional Borrowing (80% LTV) |

|---|---|---|---|

| $600,000 | $350,000 | $250,000 | $130,000 |

| $750,000 | $400,000 | $350,000 | $200,000 |

| $900,000 | $550,000 | $350,000 | $170,000 |

Maintaining a lower LTV not only improves your approval odds but also unlocks access to the most competitive interest tiers. Borrowers who keep their total debt below 75% of their property’s value frequently avoid premium surcharges applied by risk-averse institutions.

How to Evaluate Lender Terms and Credit Requirements

Selecting the optimal financing partner involves scrutinizing the specific conditions attached to their capital. The most attractive advertised rate may come with restrictive prepayment penalties or exorbitant setup fees. A holistic evaluation ensures you are not caught off guard by hidden clauses.

“Evaluating lenders isn’t just about the lowest advertised rate; it’s about understanding the total cost of borrowing over the term. A loan with a slightly higher rate but zero administrative fees often costs less over a three-year period than a heavily discounted rate packed with upfront charges.”

— Sarah Jenkins, Senior Financial Analyst at the Canadian Equity Research Institute

Credit Score Thresholds and Income Verification

Your credit history acts as the gatekeeper to premium financing. According to Equifax Canada, borrowers with scores above 720 are positioned to negotiate the most favorable terms. Most traditional institutions require a minimum score of 620 to even consider an application. If your score falls below this benchmark, you will likely need to engage with alternative or private lenders.

Income verification is equally stringent. Lenders calculate your Total Debt Service (TDS) ratio, ensuring that your existing obligations plus the new loan payment do not exceed 40% to 45% of your gross monthly income. For entrepreneurs, verifying self-employed income requires additional documentation, such as Notices of Assessment (NOAs) and corporate financial statements, to prove consistent cash flow.

Fixed vs. Variable Rates: What the 2026 Market Shows

The decision between a fixed and variable interest structure fundamentally impacts your monthly household budget and long-term financial planning. In the first quarter of 2026, market data indicates that fixed-rate options average 6.4%, providing absolute certainty for the duration of the term. Conversely, variable rates hover near 5.9% (typically calculated as Prime + 1.1%).

Fixed schedules are ideal for households that prioritize predictable expenses and wish to insulate themselves from economic volatility. However, those with robust emergency funds might prefer variable plans, capitalizing on lower initial payments and the potential for further savings if benchmark rates decline. It is crucial to understand how compounding frequency impacts your total interest accumulation, as semi-annual compounding (standard for fixed rates in Canada) differs mathematically from the monthly compounding often seen with variable products.

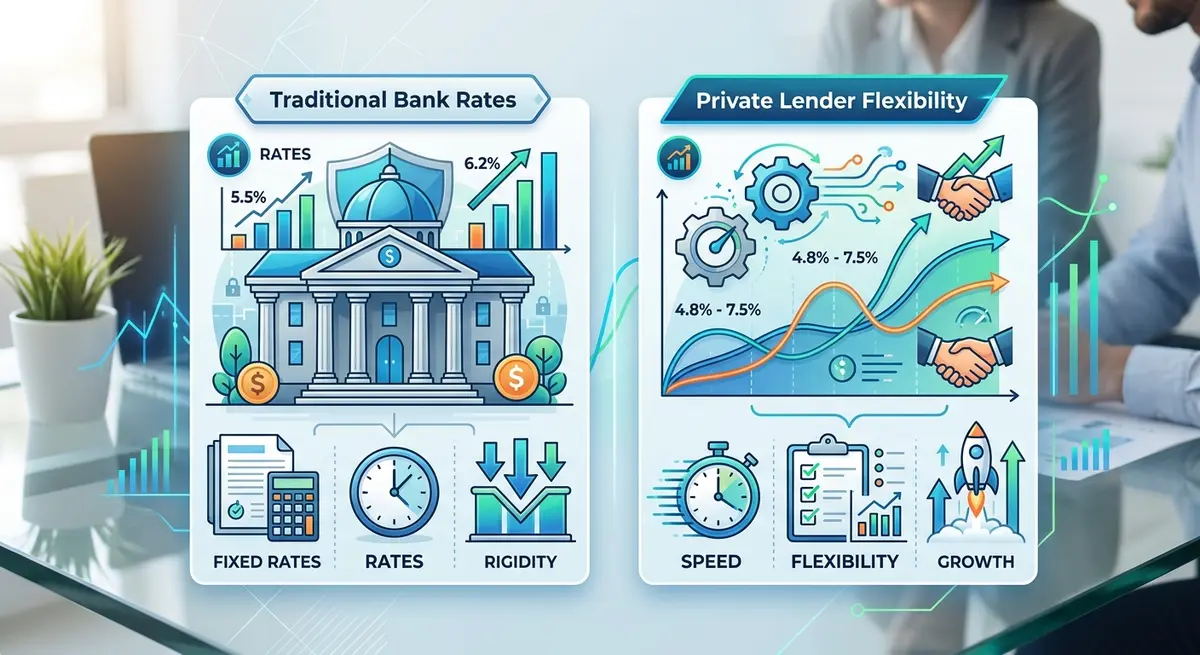

Institutional Banks vs. Alternative Private Lenders

The lending landscape is broadly divided into two categories: traditional financial institutions (A-lenders and B-lenders) and private mortgage investment corporations (MICs) or individual investors. Each serves a distinct segment of the market.

Traditional Financial Institutions

Banks and credit unions offer the lowest interest rates, typically ranging from 5.8% to 7.5%. However, their approval processes are notoriously rigorous. They require pristine credit, verifiable standard income, and low debt-to-income ratios. The underwriting process can take anywhere from three to six weeks, making them unsuitable for borrowers needing immediate capital.

Alternative and Private Lenders

Private lenders focus primarily on the equity in the property rather than the borrower’s credit score. They will often approve applications with credit scores as low as 550 and can fund a loan in as little as five to seven days. The trade-off for this speed and flexibility is cost. Private lending rates typically range from 8% to 12%, accompanied by higher setup fees. Borrowers using these funds should have a clear, short-term exit strategy, such as cash-out refinancing alternatives once their credit improves.

Second Mortgages vs. HELOCs: Structuring Your Debt

While both products leverage property value, their structures serve entirely different financial needs. A standard secondary loan provides a single, lump-sum payout with a fixed amortization schedule. This makes it the superior choice for defined, one-time expenses like a $60,000 basement renovation or consolidating a specific amount of high-interest credit card debt.

A Home Equity Line of Credit (HELOC), regulated under guidelines by the Financial Consumer Agency of Canada (FCAC), functions like a revolving credit card secured by your house. You are approved for a maximum limit and can draw, repay, and redraw funds as needed. Interest is only charged on the deployed capital. HELOCs are ideal for ongoing, unpredictable expenses, such as funding a child’s multi-year university education or managing cash flow for a small business. When deciding between the two, consider whether you need disciplined, forced repayment (lump sum) or flexible access to capital.

The Application Process: Documentation and Approval

Securing approval requires meticulous preparation. Lenders scrutinize your financial stability to mitigate their risk. Organizing your paperwork before approaching an institution significantly accelerates the underwriting process and demonstrates financial responsibility.

Step-by-Step Application Preparation

- Gather Identification and Title Documents: Prepare government-issued ID and a recent property tax bill to confirm ownership.

- Compile Income Evidence: Collect your last three pay stubs, two years of T4s, and recent NOAs.

- Document Existing Debt: Provide recent statements for your primary mortgage, auto loans, and revolving credit.

- Order an Appraisal: Most lenders require a fresh property valuation from an approved local appraiser to confirm current market worth.

Incomplete files are the leading cause of funding delays. Utilizing a comprehensive document checklist ensures your application moves swiftly from the underwriter’s desk to final approval.

Decoding Upfront Fees and Ongoing Costs

The interest rate is only one component of the total borrowing cost. Accessing home equity involves several administrative and legal hurdles, each carrying a price tag. Failing to account for these can result in receiving a smaller net loan amount than anticipated.

- Appraisal Fees: Valuing the property typically costs between $300 and $600. This is usually an out-of-pocket expense paid upfront.

- Legal and Title Fees: Registering the new charge against your property title requires a real estate lawyer. Expect to pay between $1,200 and $2,000 for their services and disbursements.

- Lender Administration Fees: Particularly common with alternative lenders, these setup fees range from 1% to 3% of the total loan amount and are often deducted directly from the loan proceeds.

- Brokerage Fees: If you use a mortgage broker to source a private loan, they may charge a fee (often 1% to 2%), though traditional bank mortgages usually compensate the broker directly without cost to the borrower.

“Borrowers often overlook administration and legal fees, which can add thousands to the upfront cost of a secondary loan. Always request a detailed ‘Cost of Borrowing’ disclosure before signing any commitment letter.”

— David Chen, Managing Director of Alberta Mortgage Analytics

Expert Negotiation Strategies for Better Rates

Many borrowers mistakenly believe that loan terms are non-negotiable. In reality, the lending market is highly competitive, and institutions are eager to acquire well-qualified clients. Strategic negotiation can save you thousands of dollars over the life of the loan.

Start by securing pre-approvals or term sheets from at least three different institutions. When you present competing offers to your preferred lender, they are often willing to match rates or waive certain administrative costs to win your business. For instance, asking a bank to cover the $450 appraisal fee is a common and frequently successful concession.

Furthermore, discuss repayment flexibility. Negotiating the ability to make lump-sum prepayments without penalty allows you to implement principal reduction strategies, drastically cutting the total interest paid. If you are considering alternative funding sources, such as borrowing from family, weigh the emotional and relational risks against the strict legal framework and higher costs of institutional borrowing.

Conclusion

Navigating the secondary lending market in 2026 requires a careful balance of understanding macroeconomic trends, assessing your personal risk tolerance, and meticulously comparing lender terms. By looking beyond the advertised interest rate and calculating the total cost of borrowing—including appraisal, legal, and administrative fees—you can leverage your property’s equity to achieve your financial goals without compromising your long-term stability. Whether you opt for the predictable structure of a fixed-rate lump sum or the flexibility of a variable HELOC, informed decision-making is your greatest asset.

If you need personalized guidance to evaluate your equity options, compare local rates, or structure an application that maximizes your approval odds, professional advice is invaluable. Get in touch with our team today to explore tailored financing solutions that align with your unique financial landscape.

Frequently Asked Questions

What is the minimum credit score required for a secondary property loan?

Traditional banks generally require a minimum credit score of 620, with the best interest rates reserved for applicants scoring 720 or higher. Alternative and private lenders are more flexible, often approving borrowers with scores as low as 550, provided there is sufficient equity in the property.

How long does the approval and funding process take?

The timeline varies significantly by lender type. Private lenders can often appraise the property and fund the loan within 5 to 7 business days. In contrast, traditional financial institutions typically require 3 to 6 weeks to complete their rigorous underwriting and income verification processes.

Can I use the borrowed funds to consolidate unsecured debt?

Yes, debt consolidation is one of the most common uses for this type of financing. By using unsecured credit options to pay off high-interest credit cards or personal loans, you can significantly reduce your blended monthly interest rate and improve your household cash flow.

Are there penalties for paying off the loan early?

Most fixed-rate agreements include prepayment penalties if you clear the balance before the term expires. This penalty is typically calculated as either three months of interest or the Interest Rate Differential (IRD), whichever is greater. Always negotiate prepayment privileges before signing the contract.

Does taking out a new loan affect the terms of my primary mortgage?

No, a secondary loan is an entirely separate legal agreement. It does not alter the interest rate, amortization schedule, or terms of your primary mortgage. However, a default on the new loan can lead to foreclosure proceedings, which would impact your primary residence.

What happens if my property value decreases after I secure the loan?

If property values decline, your Loan-to-Value (LTV) ratio will increase, potentially leaving you with negative equity if the drop is severe. While this does not immediately trigger a recall of the loan as long as you make regular payments, it will make refinancing or renewing the loan at the end of the term much more difficult.