Having a secondary lien significantly complicates the refinancing process because the new primary lender will legally require first position on your property’s title. To achieve this, homeowners must either consolidate both existing loans into a single new primary mortgage, pay off the secondary loan entirely out of pocket, or obtain a formal subordination agreement from the secondary lender allowing the new primary loan to jump ahead in the priority line. Understanding these mechanics is crucial for minimizing penalties and securing favorable terms in today’s lending environment.

Key Takeaways

- Lien Priority is Mandatory: New primary lenders will not fund a refinance unless they are guaranteed first position on the property title.

- The 80% LTV Ceiling: Under 2026 federal regulations, your combined mortgage balances cannot exceed 80% of your home’s appraised value during a standard refinance.

- Subordination Challenges: Secondary lenders are not legally obligated to subordinate to a new primary lender, especially if the new loan amount increases.

- Consolidation Benefits: Wrapping multiple property debts into one primary loan often reduces overall monthly carrying costs, despite potential prepayment penalties.

- Credit Impacts: Managing multiple mortgage payments heavily influences your Total Debt Service (TDS) ratio, which must typically remain below 44% for prime approval.

The Mechanics of Refinancing with Multiple Property Liens

When you register a mortgage against a property in Alberta, it is recorded on the land title in a specific chronological order. The first mortgage holds the primary position, meaning in the event of a default, that lender gets paid first from the sale proceeds. Any subsequent financing, such as a Home Equity Line of Credit (HELOC) or a private equity loan, sits in second position. This hierarchy is the fundamental reason why secondary financing directly impacts your ability to restructure your primary debt.

If you attempt to refinance your primary mortgage, the original first mortgage is discharged from the title, and a new one is registered. However, without intervention, the existing secondary lien would automatically slide up into the first position. Because prime lenders offer low rates based on the security of being first in line, they will outright reject an application if they are forced into second position. Therefore, the secondary lien must be addressed before the new primary loan can be funded.

“A subordination agreement is essentially a legal permission slip,” explains Marcus Thorne, Senior Underwriting Director at Alberta Lending Solutions. “It is a binding document where the secondary lender agrees to remain in second position behind the new primary mortgage. However, they will only sign this if their investment remains secure, meaning the homeowner must retain sufficient equity.” For a deeper understanding of this legal mechanism, Investopedia’s definition of subordination provides excellent context on how these agreements function across the financial sector.

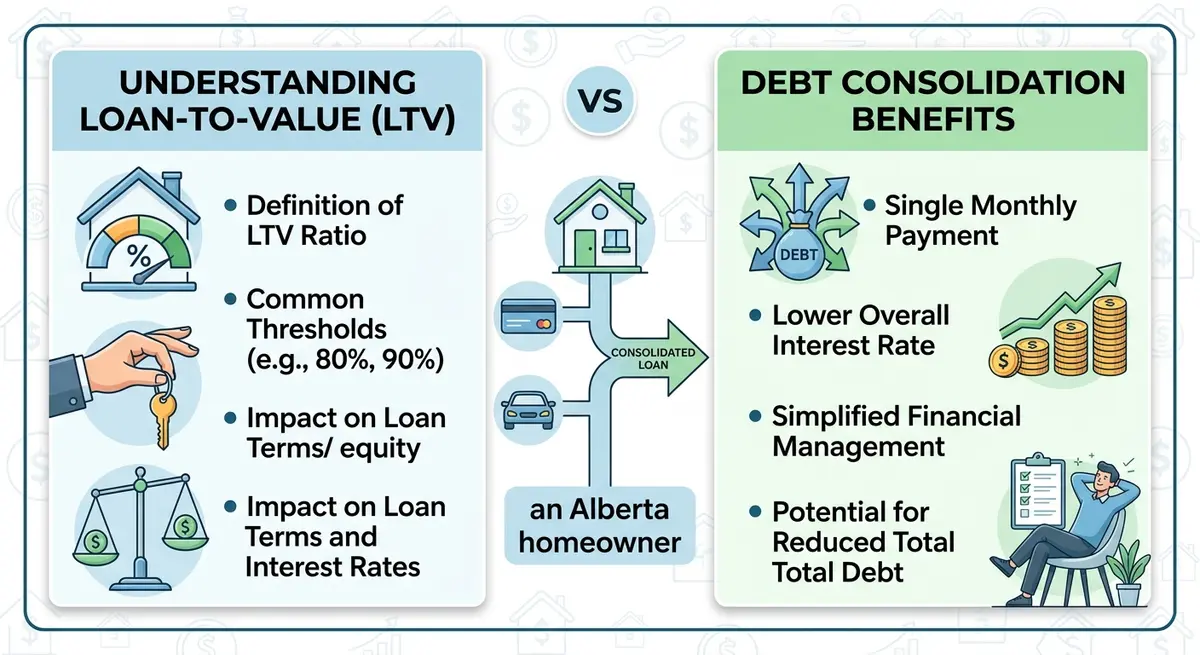

How Secondary Financing Impacts Your Loan-to-Value (LTV) Ratio

Your Loan-to-Value (LTV) ratio is the most critical metric lenders evaluate during underwriting. It represents the percentage of your property’s value that is currently mortgaged. In Canada, federal regulations stipulate that homeowners can only borrow up to 80% of their property’s appraised value when refinancing. When you have multiple liens, the balances of all registered mortgages are combined to calculate your Total Loan-to-Value (TLTV).

According to the Calgary Real Estate Board (CREB), the benchmark price for a detached home in Calgary reached approximately $745,000 in early 2026. If you own a home at this value, your maximum borrowing limit (80% LTV) is $596,000. Consider a scenario where your primary mortgage balance is $450,000, and you have a secondary loan of $100,000. Your combined debt is $550,000, resulting in a TLTV of 73.8%. Because this is under the 80% threshold, you have room to maneuver. However, if your combined debt was $620,000, you would exceed the legal limit, making a traditional refinance impossible without bringing cash to closing.

Homeowners must also account for the costs associated with breaking their current terms. Prepayment penalties, discharge fees, and legal costs are often rolled into the new loan balance. If your equity is already tight, these additional fees can push your TLTV over the 80% limit. Before initiating the process, it is highly recommended to review principal reduction strategies to build a larger equity cushion prior to appraisal.

Three Paths to Refinancing When You Have a Second Mortgage

Homeowners looking to restructure their property debt generally have three distinct pathways. The optimal choice depends on current interest rates, available equity, and long-term financial goals.

- Debt Consolidation (The Wrap-In Strategy): This is the most common approach. The homeowner applies for a new primary mortgage large enough to pay off both the existing first mortgage and the secondary lien simultaneously. This leaves the borrower with a single monthly payment, usually at a much lower interest rate than the secondary loan carried. This method requires sufficient equity (under 80% LTV) and strong income qualification.

- Subordination (The Keep-and-Replace Strategy): If the secondary loan has highly favorable terms, or if the borrower lacks the equity to consolidate, they may choose to refinance only the primary mortgage. This requires the secondary lender to sign a subordination agreement. Lenders typically charge a fee for this (ranging from $250 to $500) and will re-evaluate the property’s value to ensure their position isn’t compromised by the new primary loan amount.

- Strategic Payoff (The Clean Slate Strategy): If the secondary balance is relatively small, the homeowner may use savings, investments, or an unsecured loan to pay it off entirely before applying for the refinance. This removes the complication of subordination and cleans up the title, making the primary refinance process significantly faster and cheaper regarding legal fees.

Comparing Refinancing Options

To help visualize the differences between these strategies, the following table breaks down the core components of each approach based on 2026 market standards in Alberta.

| Refinancing Strategy | Best Suited For | Primary Advantage | Potential Drawback |

|---|---|---|---|

| Debt Consolidation | Borrowers with high-interest secondary debt and >20% equity. | Simplifies finances into one lower monthly payment. | May incur significant prepayment penalties on the primary loan. |

| Subordination | Borrowers wanting to keep a low fixed rate on their secondary loan. | Avoids penalties on the secondary loan; maintains credit lines. | Requires secondary lender approval, which is never guaranteed. |

| Strategic Payoff | Borrowers with liquid assets or small secondary balances. | Streamlines underwriting and reduces legal closing costs. | Depletes liquid savings or requires taking on unsecured debt. |

Calgary Market Dynamics and Interest Rate Trends in 2026

The economic environment heavily influences the viability of restructuring property debt. In 2026, the Bank of Canada has maintained a stabilized overnight rate, which has created a predictable environment for fixed-rate mortgage products. However, secondary financing—often tied to prime rates or offered by private lenders—continues to carry premiums of 1.5% to 4% above primary rates.

“In the 2026 rate environment, maintaining a low-interest primary mortgage while strategically managing secondary debt is often more cost-effective than a full break-and-blend,” advises Dr. Harrison Vance, Chief Economist at the Prairie Real Estate Institute. “Borrowers must calculate the blended amortization cost. Breaking a 3.5% primary mortgage to consolidate a 9% secondary loan into a new 5% primary mortgage might actually cost more in lifetime interest, depending on the balances.”

Furthermore, Calgary’s robust population growth has sustained property values, providing many homeowners with the equity required to execute cash-out refinancing options. However, lenders remain hyper-vigilant about property appraisals. An over-leveraged property in a localized market dip can quickly derail a consolidation plan.

The Role of Credit Scores and Debt Service Ratios

When you apply to restructure your mortgages, lenders scrutinize your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios. Data from the Financial Consumer Agency of Canada (FCAC) indicates that prime lenders strictly enforce a maximum GDS of 39% and a TDS of 44%. Having a secondary loan payment significantly inflates your TDS.

If you are attempting a subordination strategy, the new primary lender will include the monthly payment of your secondary loan in their TDS calculations. If that secondary loan is a HELOC, they will typically calculate the payment based on the fully amortized limit of the credit line, not just your current drawn balance. This aggressive calculation method often pushes borrowers over the 44% TDS limit, forcing them to pivot to a consolidation strategy instead.

Additionally, your credit score plays a pivotal role. Prime lenders generally require a minimum beacon score of 680 for optimal rates. If your score has dropped due to high credit utilization or recent inquiries, you may face higher rate premiums. It is vital to know how to explain recent credit inquiries to underwriters to mitigate perceived risks.

Real-World Example: Navigating a Complex Refinance in Alberta

To illustrate these concepts, consider the MacLeod family in South Calgary. In early 2026, their property was appraised at $650,000. They held a primary mortgage of $320,000 at 4.2% and a private secondary loan of $80,000 at 10.5%, which they had used for emergency home repairs. Their combined monthly payments were straining their cash flow.

They initially wanted to refinance their primary mortgage to a lower rate while keeping the private loan. However, the private lender refused to sign a subordination agreement because the MacLeods wanted to roll $15,000 of credit card debt into the new primary loan, which would have increased the primary balance and diluted the private lender’s equity security.

Instead, their broker pivoted to a full consolidation strategy. They secured a new primary mortgage of $425,000 at 4.8%. This new loan paid off the original primary, the high-interest private loan, the credit card debt, and covered the $2,100 in legal and appraisal fees. While their primary interest rate increased slightly, eliminating the 10.5% secondary loan and the 19.9% credit card debt reduced their total monthly debt obligations by $840. This case highlights why understanding compounding frequency impacts across different debt vehicles is essential for long-term wealth preservation.

Common Pitfalls to Avoid During the Underwriting Process

Restructuring multiple property liens involves significant legal and administrative maneuvering. Homeowners frequently encounter roadblocks that can delay funding or incur unexpected costs. Being proactive can save thousands of dollars.

First, never underestimate prepayment penalties. Under the Canada Interest Act, breaking a closed fixed-rate mortgage usually triggers an Interest Rate Differential (IRD) penalty, which can easily exceed $10,000 depending on your balance and remaining term. Always request an official payout statement from your current lenders before signing a new commitment.

Second, ensure your documentation is pristine. Lenders will require updated income verification, property tax statements, and full details of all registered liens. Missing paperwork is the leading cause of funding delays. Utilizing a comprehensive guide for organizing your mortgage paperwork ensures you present a strong, organized file to the underwriter.

Finally, be prepared for appraisal shortfalls. If you are relying on alternative documentation financing or have a unique property, the appraised value might come in lower than expected. A lower appraisal immediately shrinks your 80% LTV borrowing limit, which can leave you short of the funds needed to pay out the secondary lender during a consolidation.

Frequently Asked Questions (FAQ)

Can a secondary lender block my ability to refinance?

Yes, indirectly. If you are not paying off the secondary loan through consolidation, the secondary lender must sign a subordination agreement. If they refuse—often because they feel their equity position is threatened by the new primary loan—you cannot proceed with the refinance.

Does consolidating a secondary loan into a primary mortgage save money?

Usually, yes. Secondary loans typically carry interest rates 2% to 8% higher than primary mortgages. Consolidating them into a single primary loan at a lower rate reduces your blended interest cost and significantly lowers your monthly payments.

How much does it cost to process a subordination agreement in Alberta?

Secondary lenders typically charge an administrative fee ranging from $250 to $500 to review and sign a subordination agreement. Additionally, your real estate lawyer will charge fees to register the new documents on the land title, usually adding $1,000 to $1,500 to your closing costs.

Will I need a new property appraisal?

Almost certainly. Because you are restructuring the debt secured against the property, the new primary lender will require a full, current appraisal to confirm the home’s market value and ensure the Total Loan-to-Value (TLTV) remains under the 80% legal limit.

Can I consolidate my secondary loan if my credit score has dropped?

It is possible, but challenging. Prime lenders generally require a credit score of 680+ for consolidation. If your score is lower, you may need to work with a “B-lender” or alternative institution, which will charge a higher interest rate and potentially a 1% lender fee.

What happens if my property value has decreased?

If your property value has dropped, your Loan-to-Value ratio increases. If your combined mortgage balances exceed 80% of the new, lower appraised value, you will not be able to consolidate both loans without bringing cash to the closing table to cover the shortfall.

Conclusion

Navigating the complexities of property refinancing when multiple liens are involved requires careful mathematical analysis and strategic planning. Whether you choose to consolidate your debts into a single, manageable payment or negotiate a subordination agreement to preserve favorable terms, understanding your Loan-to-Value limits and debt service ratios is paramount. In the evolving 2026 Calgary real estate market, making the wrong move can trigger severe prepayment penalties or leave you trapped in high-interest obligations. Professional guidance is essential to ensure your property’s equity is working for you, not against you. If you are struggling to manage multiple property liens or want to explore your restructuring options, contact us today to speak with a specialized mortgage strategist.