A second mortgage in Alberta is a subordinate loan secured against your property’s accumulated equity, allowing you to borrow up to 80% of your home’s appraised value minus your existing primary mortgage balance. It functions by placing a secondary lien on your property, providing either a lump sum of cash or a revolving line of credit without requiring you to break or renegotiate the terms of your first mortgage. Because the primary mortgage remains intact, homeowners can access necessary capital while preserving their original, often lower, interest rate.

Key Takeaways

- Homeowners can access up to 80% of their property’s appraised value through secondary financing options.

- The primary mortgage remains entirely unaffected, allowing borrowers to maintain their original interest rates and terms.

- Funds can be utilized for various purposes, including high-interest debt consolidation, property renovations, or business investments.

- Approval relies heavily on available equity, with minimum credit scores typically starting around 620 for traditional lenders, though private lenders offer more flexibility.

- Secondary liens carry higher interest rates than primary mortgages due to the increased risk assumed by the lender in the event of default.

Understanding Home Equity and Borrowing Limits in Alberta

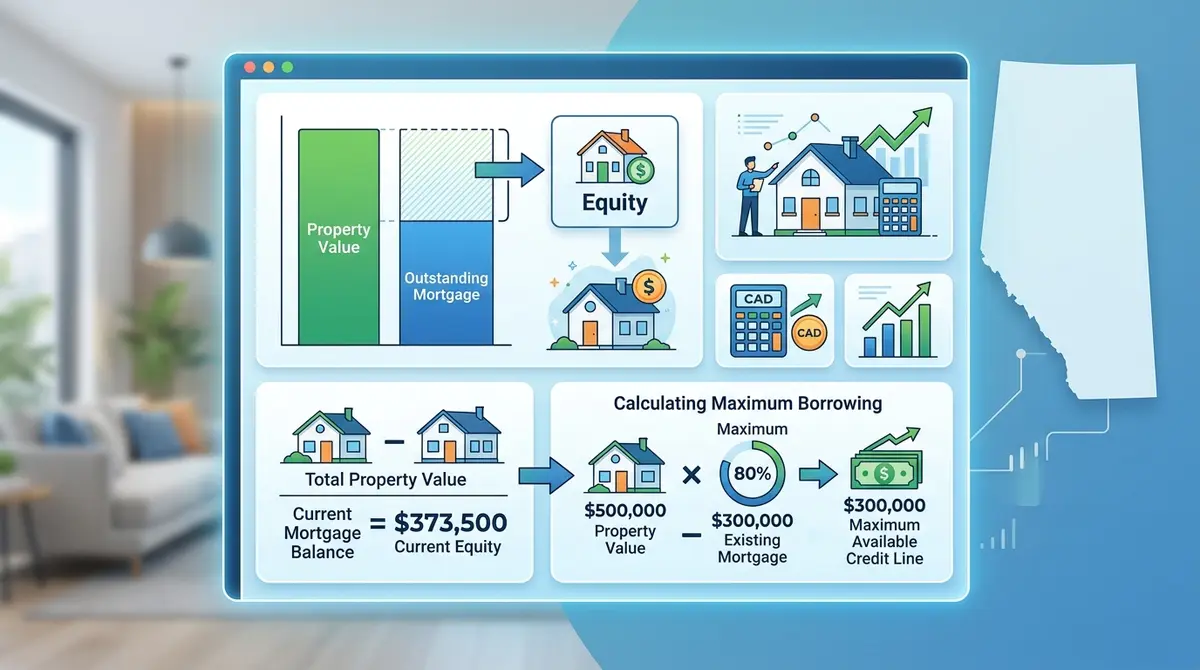

To grasp how secondary financing operates, one must first understand the concept of home equity. Equity represents the portion of your property that you truly own outright—calculated as the current market value of the home minus any outstanding loan balances secured against it. In 2026, with the Calgary Real Estate Board reporting sustained property value growth across numerous quadrants, many homeowners find themselves sitting on substantial untapped wealth.

Canadian financial regulations stipulate that homeowners can borrow up to a maximum Loan-to-Value (LTV) ratio of 80% when combining their first and second mortgages. Understanding Loan-to-Value ratio mechanics is critical for calculating your exact borrowing capacity.

Consider this mathematical example: If your property is appraised at $600,000, the maximum allowable debt secured against the home is $480,000 (80% of $600,000). If your primary mortgage balance is $350,000, your available borrowing capacity for a secondary loan would be $130,000. This calculation forms the foundation of every secondary financing application.

Types of Secondary Financing Available to Homeowners

Not all secondary loans are structured identically. Depending on your financial objectives, lenders offer several distinct products. Selecting the correct vehicle is paramount for long-term financial stability.

Home Equity Loans (Lump Sum)

A traditional home equity loan provides a single, lump-sum payment upfront. These loans typically feature fixed interest rates and a set amortization schedule, meaning your monthly payments remain entirely predictable. This structure is ideal for homeowners facing a specific, one-time expense, such as a major home renovation or consolidating a fixed amount of consumer debt.

Home Equity Lines of Credit (HELOCs)

A HELOC functions similarly to a high-limit credit card secured by your home. It provides a revolving credit facility where you only pay interest on the funds you actively draw. HELOCs generally feature variable interest rates tied to the Bank of Canada interest rate policies. They offer unparalleled flexibility for ongoing projects or as an emergency financial safety net.

Private Secondary Mortgages

For individuals who may not meet the stringent stress-test requirements of traditional banking institutions, private lenders offer an alternative. These loans focus primarily on the property’s equity rather than the borrower’s credit score or traditional income verification. While they carry higher interest rates, they provide rapid access to capital and flexible qualification criteria.

| Financing Type | Interest Rate Structure | Fund Disbursement | Best Used For |

|---|---|---|---|

| Home Equity Loan | Fixed | Single Lump Sum | Debt consolidation, major one-time purchases |

| HELOC | Variable | Revolving Credit | Ongoing renovations, emergency funds |

| Private Mortgage | Fixed or Variable | Lump Sum | Bridge financing, repairing credit, urgent capital |

The Mechanics of Lien Priority

The term “second” in secondary financing refers directly to lien priority. When a property is used as collateral, lenders register a legal claim, or lien, against the title. The institution that holds your primary mortgage holds the first position. Any subsequent lender takes a subordinate, or second, position.

As Marcus Thorne, a senior real estate financial analyst, explains: “Lien priority dictates the order in which creditors are paid in the event of a property liquidation. Because the secondary lender is only paid after the primary lender is made whole, they assume significantly more risk. This structural risk is precisely why secondary financing carries a higher interest rate than primary mortgages.”

2026 Interest Rates and Associated Costs

When evaluating secondary financing, borrowers must look beyond the advertised interest rate and consider the Annual Percentage Rate (APR), which encompasses all associated fees. In 2026, interest rates for these products typically range from 6.5% to 12%, depending heavily on the borrower’s credit profile, the LTV ratio, and the type of lender chosen.

Beyond the interest rate, applicants should budget for several administrative and legal expenses:

- Appraisal Fees: A professional valuation is mandatory to confirm the property’s current market worth, typically costing between $350 and $500.

- Legal Fees: Registering a new lien on a property title requires a real estate lawyer. Expect legal disbursements to range from $800 to $1,500.

- Lender/Broker Fees: Particularly in the private lending space, origination fees or broker commissions of 1% to 3% of the loan amount are standard.

It is crucial to request a comprehensive disclosure of all fees upfront. Understanding these costs helps in formulating effective strategies for reducing your principal balance over the lifespan of the loan.

Step-by-Step: The Application and Approval Process

Securing a secondary loan involves a systematic underwriting process. While faster than acquiring a primary mortgage, it still requires thorough documentation and financial transparency. Following a comprehensive documentation checklist can significantly expedite approval.

- Equity Assessment: Calculate your available equity using a recent property tax assessment or a conservative estimate of your home’s current market value.

- Document Preparation: Gather proof of income (T4s, recent pay stubs, Notice of Assessment), current mortgage statements, and property tax records. If you are self-employed, you may need to explore alternative financing for entrepreneurs that utilizes stated income.

- Lender Selection: Compare offers from traditional banks, credit unions, and alternative lenders to find terms that align with your financial profile.

- Property Appraisal: The lender will order an independent appraisal to verify the exact value of the collateral.

- Underwriting and Legal Review: The lender assesses your debt service ratios and credit history. Once approved, the paperwork is sent to your lawyer for title registration and fund disbursement.

Qualification Requirements: What Lenders Analyze

Lenders evaluate risk through several specific metrics before approving a secondary loan. According to Financial Consumer Agency of Canada guidelines, federally regulated institutions must apply strict stress tests, though alternative lenders have more leeway.

Credit Score Thresholds

While traditional banks typically require a minimum credit score of 680 for a HELOC or home equity loan, alternative and private lenders are far more accommodating. Many will approve applications with scores as low as 550, provided there is substantial equity (usually an LTV below 65%) to offset the credit risk.

Debt Service Ratios

Your ability to manage monthly payments is calculated using two formulas: Gross Debt Service (GDS) and Total Debt Service (TDS). Lenders generally prefer a GDS ratio under 39% and a TDS ratio under 44%. These ratios calculate what percentage of your gross monthly income is consumed by housing costs and total debt obligations, respectively.

If you are applying with a partner to improve these ratios, understanding the process of including a partner on your application is essential for a smooth underwriting experience.

Strategic Uses: Why Homeowners Choose Secondary Mortgages

Leveraging property wealth is a powerful financial tool when deployed strategically. In 2026, data indicates that over 32% of homeowners utilizing secondary financing do so for debt consolidation. By paying off high-interest credit cards (often carrying rates of 19.99% to 24.99%) with a secondary loan at 8%, borrowers can save thousands in interest and dramatically improve their monthly cash flow.

Another primary use is property improvement. Investing equity back into the home through renovations—such as developing a legal basement suite or upgrading kitchens—can yield a high return on investment, effectively increasing the property’s overall value.

Furthermore, many investors use their primary residence’s equity as a springboard for acquiring additional real estate, leveraging equity for a new down payment on a rental property.

Secondary Financing vs. Mortgage Refinancing

A common dilemma for homeowners is deciding between adding a secondary lien or breaking their existing mortgage to refinance. Comparing secondary financing to cash-out refinancing requires analyzing your current interest rate.

If you secured your primary mortgage several years ago at a historically low fixed rate (e.g., 2.5%), breaking that mortgage to access equity means your entire balance will be subject to today’s higher rates (e.g., 5.5%), plus you will incur substantial prepayment penalties. In this scenario, taking out a smaller secondary loan at a higher rate is mathematically superior, as it protects the low rate on the bulk of your debt.

Conversely, if your primary mortgage is nearing renewal or your current rate is higher than prevailing market rates, a complete cash-out refinance might be the more economical choice.

Navigating the Risks: Default and Market Fluctuations

Borrowing against your home is not without risk. Because the loan is secured by your property, failure to maintain payments can result in severe legal consequences. If a borrower defaults, the lender has the legal right to initiate foreclosure proceedings to recover their capital.

It is vital to understand the legal timeline for property seizure in Alberta. If the property is sold through foreclosure, the primary mortgage holder is paid first. The secondary lender receives the remaining funds. If the property value has dropped due to market fluctuations, the secondary lender may face a shortfall, which is why they strictly enforce the 80% LTV limit to ensure a buffer exists.

To mitigate these risks, borrowers should maintain a robust emergency fund covering three to six months of living expenses and avoid borrowing to their absolute maximum limit.

Choosing the Right Lender

The lending landscape in Alberta is diverse. Traditional “A-Lenders” (major banks) offer the lowest rates but demand pristine credit and rigorous income verification. “B-Lenders” (trust companies and credit unions) provide a middle ground, offering slightly higher rates for those with minor credit blemishes.

Private lenders focus almost exclusively on the asset’s value. While their rates are the highest, they offer unparalleled speed and flexibility, making them an excellent short-term solution for bridge financing or debt restructuring before transitioning back to a traditional lender.

Conclusion

Understanding how secondary financing works empowers homeowners to make informed, strategic decisions about their wealth. By carefully calculating available equity, comparing lender terms, and deploying the funds toward wealth-building or debt-reduction strategies, a secondary loan can be a transformative financial tool. However, it requires disciplined repayment planning and a clear understanding of the associated risks and costs.

If you are considering leveraging your property’s equity and want to explore the best rates and terms available in the 2026 market, professional guidance is invaluable. Get in touch with our team today to discuss your unique financial situation and discover the optimal borrowing strategy for your needs.

Frequently Asked Questions (FAQ)

Can I get a secondary loan with bad credit?

Yes, it is possible to secure financing with poor credit by utilizing alternative or private lenders. These institutions base their approval primarily on the amount of equity in your property rather than your credit score, though you will pay a higher interest rate.

How long does the approval process take?

The timeline varies by lender. Traditional banks may take two to four weeks to process an application, order an appraisal, and complete legal registration. Private lenders can often approve and fund a loan within five to ten business days.

Do I have to make monthly payments on a HELOC if I haven’t used it?

No. A Home Equity Line of Credit is a revolving facility. You are only charged interest on the exact amount of funds you have drawn. If your balance is zero, your monthly payment is zero.

Can a lender force the sale of my home if I default on the secondary loan?

Yes. Because the loan is secured by a legal lien against your property title, the secondary lender has the right to initiate foreclosure proceedings if you default on your payments, regardless of whether your primary mortgage is in good standing.

Are the fees for setting up the loan tax-deductible?

In Canada, the fees and interest associated with borrowing against your home are generally not tax-deductible if the funds are used for personal reasons (like renovations or consumer debt). However, if the funds are used directly to generate investment income, portions may be deductible. Always consult a certified accountant.

What happens to my secondary loan when I sell my house?

When you sell your property, the proceeds from the sale are used to pay off all registered liens in order of priority. Your primary mortgage is paid first, followed immediately by the secondary loan, before any remaining profit is released to you.