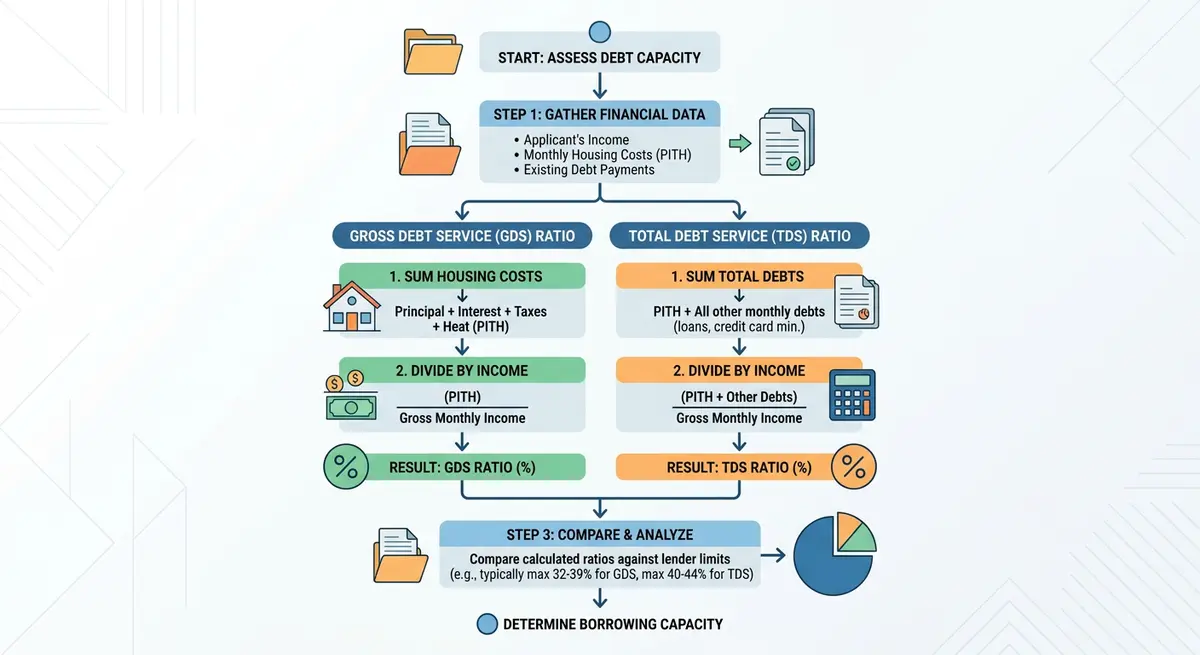

Lenders calculate debt service ratios for second mortgages by comparing a borrower’s gross monthly income against their combined monthly debt obligations. This standardized underwriting process relies on two distinct metrics: the Gross Debt Service (GDS) ratio, which divides total housing costs (including the first mortgage, proposed second mortgage, property taxes, and heating) by gross income, and the Total Debt Service (TDS) ratio, which adds all other consumer debts to those housing costs. In 2026, mastering these mathematical formulas is the definitive foundation for securing home equity financing and negotiating favorable loan terms in Calgary’s competitive real estate market.

Key Takeaways

- Dual Metric System: Underwriters evaluate both GDS (housing expenses) and TDS (total debt) to determine your true borrowing capacity.

- Standard vs. Alternative Limits: Traditional lenders require a GDS under 32% and a TDS under 40%, while Calgary’s alternative private lenders may accept TDS ratios up to 50% based on property equity.

- Comprehensive Calculations: Second mortgage ratios must simultaneously account for the existing first mortgage payment and the new proposed loan payment.

- Income Verification is Crucial: Verifiable gross income forms the denominator of the ratio; self-employed and rental incomes are subject to specific lender deductions.

- Strategic Debt Management: Paying down high-interest revolving credit before applying is the most effective method to rapidly lower your TDS ratio.

Understanding the Dual Ratio System in 2026

When considering a second mortgage, understanding financial metrics is crucial for securing approval. These ratios serve as the absolute foundation for mortgage underwriting decisions across Alberta. They determine whether borrowers can comfortably manage additional debt obligations alongside their existing financial commitments without risking default. For Calgary homeowners exploring equity extraction, mastering these calculations often means the difference between a rapid approval and a frustrating rejection.

In the context of second mortgages, these ratios become particularly complex. They must account for existing first mortgage payments, proposed second mortgage payments, and all other monthly debt obligations simultaneously. Calgary’s dynamic economic landscape, characterized by fluctuating energy sector bonuses and diverse self-employment income, makes precise calculations especially relevant for local borrowers.

The calculation process involves two primary ratios that serve distinct purposes in evaluating borrower creditworthiness. According to Canada Mortgage and Housing Corporation (CMHC) guidelines, traditional A-tier lenders typically look for a GDS ratio below 32% and a TDS ratio under 40%. However, the alternative lending market in Calgary operates with entirely different thresholds. Many private lenders and Mortgage Investment Corporations (MICs) will accept TDS ratios up to 50% if the property possesses sufficient equity.

As Sarah Jenkins, Chief Underwriter at Alberta Financial Group, explains: “In 2026, lenders scrutinize TDS ratios more than ever. Borrowers must account for every revolving credit line, not just fixed loans. The precision of your initial calculation dictates the speed of your funding, especially when dealing with secondary financing where risk margins are tighter.”

Gross Debt Service (GDS) Ratio: The Housing Cost Formula

The Gross Debt Service (GDS) ratio calculation provides lenders with insight into a borrower’s capacity to manage property-specific financial obligations. For second mortgage applications, this calculation must incorporate payments for both the existing first mortgage and the proposed second mortgage. The mathematical formula divides total monthly housing costs by gross monthly income, expressed as a percentage.

Housing costs included in GDS calculations encompass principal and interest payments for all mortgages secured against the property, monthly property tax obligations, and heating expenses. If you own a condominium or townhome in Calgary, exactly 50% of your monthly condo fees are also included in the GDS calculation, regardless of what those fees actually cover.

In Calgary’s climate, heating costs represent a significant component of housing expenses. Lenders typically use a standard estimate of $150 per month for heating if actual utility bills are not provided. Furthermore, property taxes vary considerably across Calgary’s diverse neighborhoods. Lenders often apply a 2.5% estimation factor based on the assessed property value if current tax statements are unavailable. Providing exact documentation is always preferable to relying on lender estimates, which tend to be conservative.

GDS vs. TDS Component Comparison

Understanding exactly what goes into each formula is critical for accurate self-assessment. The following table breaks down the specific components used by Calgary lenders in 2026:

| Expense Category | Included in GDS Ratio? | Included in TDS Ratio? |

|---|---|---|

| First Mortgage (Principal & Interest) | Yes | Yes |

| Proposed Second Mortgage | Yes | Yes |

| Property Taxes | Yes | Yes |

| Heating Costs | Yes | Yes |

| Condo Fees (50%) | Yes | Yes |

| Credit Card Minimum Payments | No | Yes |

| Auto Loans & Leases | No | Yes |

| Personal Lines of Credit | No | Yes |

Total Debt Service (TDS) Ratio: Comprehensive Debt Analysis

The TDS ratio provides lenders with a holistic view of a borrower’s complete debt obligations. This calculation offers crucial insight into your overall financial capacity and your ability to manage multiple debt obligations simultaneously without defaulting. TDS calculations begin with all components included in the GDS ratio, then add monthly payments for credit cards, personal loans, student loans, vehicle financing, and unsecured lines of credit.

The primary challenge lies in accurately capturing minimum required payments. For credit cards, Calgary lenders typically use either the minimum payment shown on recent statements or 3% of the outstanding balance, whichever is higher. This prevents borrowers from artificially lowering their ratios by making interest-only payments right before applying.

Calgary borrowers often carry various forms of debt reflecting the city’s economic diversity. Vehicle loans remain common given the city’s geography and reliance on personal transportation. It is vital to understand how compounding frequency silently increases your debt, as this can impact the minimum payments lenders calculate for your TDS ratio over time. Even small personal loans can tip a TDS ratio over the acceptable 40% threshold if not managed correctly.

Step-by-Step: Calculating Your Ratios for a Second Mortgage

To fully grasp how underwriters evaluate your file, Calgary borrowers should follow this standardized five-step process used by professional mortgage brokers:

- Calculate Gross Monthly Income: Sum all verifiable income before taxes. This includes base salary, consistent overtime (usually averaged over two years), and eligible rental income.

- Tally Total Housing Costs: Add the monthly payments for your first mortgage, the proposed second mortgage, property taxes, heating, and 50% of condo fees.

- Determine the GDS Ratio: Divide the total housing costs by your gross monthly income and multiply by 100 to get the percentage.

- Sum Additional Debt Obligations: Calculate the minimum monthly payments for all credit cards, auto loans, student debt, and unsecured lines of credit.

- Determine the TDS Ratio: Add the additional debt obligations to your housing costs, divide by your gross monthly income, and multiply by 100.

For further regulatory context on these steps and how they impact consumer borrowing limits, borrowers can review the official guidelines provided by the Financial Consumer Agency of Canada (FCAC).

Income Verification Complexities for Calgary Borrowers

Accurate income calculation forms the foundation of reliable debt service ratio analysis. Traditional employment income provides the most straightforward calculation basis, typically using gross monthly income from recent pay stubs and employment verification letters. However, Calgary’s dynamic economy creates numerous scenarios requiring specialized approaches.

Self-employed borrowers face particular challenges. Lenders typically require two years of Notices of Assessment (NOA) and T1 Generals to establish consistent income patterns. If you are a business owner struggling with traditional verification, you must learn about verifying self-employed mortgage income through reasonability tests. Some alternative lenders offer stated income second mortgages, which rely more on business cash flow statements than personal tax returns, though these come with higher interest rates.

Rental income from investment properties or basement suites can significantly improve debt service ratios. However, most lenders include only 50% to 75% of gross rental income to account for vacancy periods and maintenance costs. Calgary’s strong 2026 rental market makes this income source particularly valuable, provided you have the proper lease agreements in place.

According to Marcus Thorne, Senior Mortgage Broker at Calgary Lending Solutions: “Understanding how debt service ratios are calculated for a second mortgage in Calgary is the single biggest advantage a borrower can have. If you know exactly how lenders treat your rental add-backs, you can negotiate much better terms and avoid unnecessary rejections.”

The Impact of Credit Scores on Ratio Limits

Your credit score directly influences the maximum debt service ratios a lender will accept. Borrowers with excellent credit scores (typically 720 and above) may qualify for extended ratio limits. In these cases, traditional lenders might stretch the GDS to 39% and the TDS to 44%, provided the borrower has strong liquid assets in reserve.

Conversely, borrowers with lower credit scores face more restrictive requirements. If your credit report shows numerous recent inquiries from shopping around for loans, you may need to explain credit inquiries to lenders to prevent them from artificially lowering your maximum allowable TDS ratio. Every hard check can signal financial distress to an underwriter.

Alternative lenders focus more on property equity than strict credit scores. If a Calgary home has substantial equity (typically leaving at least 20% to 25% equity after the second mortgage is applied), private lenders may approve second mortgages with TDS ratios exceeding 50%. They utilize compensating factors to mitigate the risk of default, prioritizing the asset’s value over the borrower’s immediate cash flow metrics.

Real-World Example: A Calgary Homeowner’s Ratio Calculation

To illustrate these concepts, consider a Calgary homeowner in 2026 with a gross monthly household income of $12,000. Their current first mortgage payment is $2,500, and they are applying for a second mortgage with a proposed monthly payment of $1,200. Their monthly property taxes are $400, and standard heating costs are $150.

First, we calculate the GDS ratio. The total housing costs ($2,500 + $1,200 + $400 + $150) equal $4,250. Dividing $4,250 by the $12,000 gross income yields a GDS ratio of 35.4%. This slightly exceeds the traditional 32% limit but is well within alternative lending guidelines.

Next, we calculate the TDS ratio. The homeowner has an $800 monthly car loan payment and $300 in minimum credit card payments. Adding these $1,100 in consumer debts to the $4,250 housing costs equals $5,350 in total monthly debt. Dividing $5,350 by $12,000 yields a TDS ratio of 44.5%.

This case study illustrates exactly how approvals depend on finding the right lender for these specific metrics. A traditional bank would likely decline this application based on the 44.5% TDS, but a Calgary-based alternative lender would view this as a strong file, assuming the property has adequate equity.

Edge Cases: When Standard Ratio Rules Don’t Apply

Not all second mortgage applications fit neatly into standard banking formulas. Alternative lenders and private mortgage investment corporations (MICs) in Alberta often utilize common-sense underwriting. This means they look beyond the rigid GDS and TDS percentages.

Compensating factors can override high debt service ratios. These factors include substantial liquid assets, a very low Loan-to-Value (LTV) ratio (typically under 65%), or a highly marketable property in a prime Calgary neighborhood. In situations involving relationship breakdowns, these calculations become even more critical when navigating spousal buyouts and separation mortgages, where one income is suddenly removed from the household equation.

Furthermore, if the second mortgage is being used explicitly to consolidate and pay off high-interest credit cards, lenders will calculate the proposed TDS ratio based on the new, lower consolidated debt payments rather than the current high payments. This is a massive advantage for borrowers seeking debt relief.

As Dr. Elena Rostova, Economics Professor at the University of Calgary, notes: “The divergence between traditional bank thresholds and alternative lending limits has widened significantly in 2026. This gives homeowners more leverage if they understand their exact debt-to-income metrics and how they align with current Bank of Canada policy rates.”

Strategic Optimization: Improving Your Ratios Before Applying

Calgary borrowers can proactively improve their debt service ratios before submitting a second mortgage application. The most effective strategy is paying down revolving debt to lower the minimum monthly payments factored into the TDS calculation. Even small reductions in credit card balances can significantly drop your overall TDS percentage.

Another powerful tactic involves exploring principal reduction strategies on existing loans. Extending the amortization period on an auto loan, for example, lowers the monthly payment obligation, instantly improving your borrowing capacity for the second mortgage. You might also consider adding a spouse to your home equity loan to combine incomes and drastically lower the GDS and TDS ratios.

Finally, meticulous documentation is essential. Lenders will use the most conservative estimates if proof is lacking. By properly organizing your mortgage paperwork, including exact property tax statements and utility bills, you prevent underwriters from using inflated default estimates in your GDS calculation.

Conclusion

Understanding the intricacies of Gross Debt Service and Total Debt Service ratios is non-negotiable for Calgary homeowners seeking a second mortgage in 2026. By accurately calculating your housing costs, managing your consumer debt, and understanding how different lenders view your income, you position yourself for a successful application. Whether you fit into the strict 32/40 parameters of traditional banks or require the flexibility of alternative lenders, knowing your numbers is your greatest asset.

If you are struggling to calculate your ratios or have been turned down by a traditional bank due to high TDS limits, professional guidance can help you navigate the alternative lending market. Contact us today to speak with a Calgary second mortgage specialist who can accurately assess your debt service ratios and connect you with the right lender for your unique financial situation.

Frequently Asked Questions (FAQ)

What is a good debt service ratio for a second mortgage in Calgary?

A strong application typically features a Gross Debt Service (GDS) ratio below 35% and a Total Debt Service (TDS) ratio below 42%. However, alternative lenders in Calgary will frequently approve ratios up to 50% if there is sufficient equity in the property.

How do lenders calculate minimum credit card payments for TDS?

Most Calgary lenders calculate your credit card liability by using either the actual minimum payment shown on your latest statement or 3% of the total outstanding balance, whichever figure is higher. This prevents borrowers from manipulating ratios with interest-only payments.

Are property taxes included in the GDS calculation?

Yes, 100% of your annual property taxes, divided into a monthly amount, are included in the GDS calculation. If you do not provide an official tax statement, lenders typically estimate this at 2.5% of the property’s assessed value.

Can I use rental income to lower my debt service ratios?

Yes, rental income can improve your ratios. However, lenders generally only add 50% to 75% of the gross monthly rental income to your total income to account for potential vacancies, property management, and maintenance costs.

How do second mortgage ratio calculations differ from first mortgages?

The mathematical formulas are identical. However, for a second mortgage, the GDS and TDS calculations must include the principal and interest payments for both the existing first mortgage and the new proposed second mortgage simultaneously.

Does a high credit score allow for higher debt service ratios?

Yes. Borrowers with excellent credit scores (720+) and strong financial reserves are often granted exceptions. This allows them to exceed standard ratio thresholds by 2% to 4% with traditional A-tier lenders.

Are utility bills included in the Total Debt Service ratio?

Only heating costs are included in the GDS and TDS calculations. Other utilities like electricity, water, internet, and home insurance are not factored into standard debt service ratios.

What happens if my TDS ratio is over 50%?

If your TDS exceeds 50%, traditional banks will decline the application. However, private equity lenders in Calgary may still approve the second mortgage if your Loan-to-Value (LTV) ratio is below 65% to 75%, relying entirely on the property’s equity rather than your income.