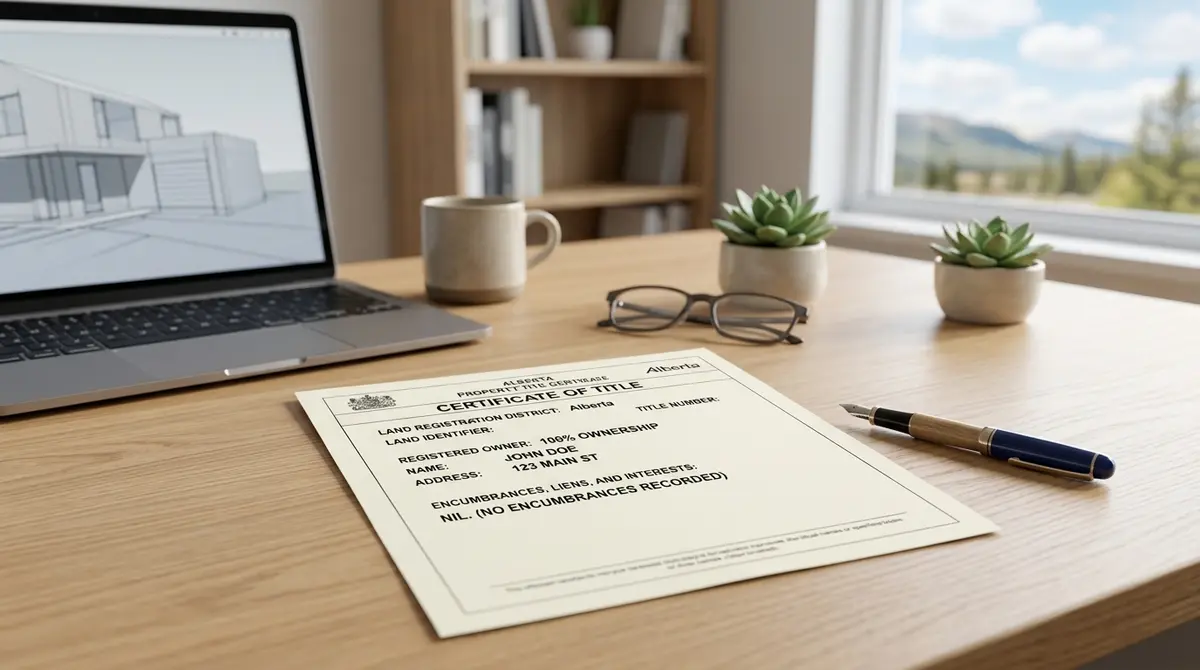

Discharging a second mortgage in Alberta is the formal legal process of removing a secondary lender’s financial claim from your property title after the loan has been fully paid. To complete this process, homeowners must obtain a formal discharge document—often called a satisfaction piece—from their lender and register it directly with the Alberta Land Titles Office. Simply making your final payment does not automatically clear your title; the encumbrance remains legally binding until the discharge is officially registered.

Key Takeaways

- Payment Isn’t Enough: Paying off your loan balance does not automatically remove the mortgage from your property title.

- Mandatory Registration: The discharge document must be formally registered with the Alberta Land Titles Office to be legally effective.

- 2026 Cost Expectations: Budget between $350 and $850 for legal fees, government registration costs, and lender administrative charges.

- Processing Timelines: The end-to-end process typically takes 3 to 6 weeks, depending on lender responsiveness and government backlogs.

- Future Impact: An undischarged mortgage can block future property sales, complicate refinancing, and artificially limit your borrowing capacity.

Understanding the Mortgage Discharge Process in Alberta

Many homeowners mistakenly believe that once their final payment clears the bank, their relationship with the lender is completely severed. According to 2026 data from the Real Estate Council of Alberta (RECA), approximately 85% of homeowners assume that paying off a loan means automatic title clearance. In reality, the legal framework governing property rights in the province requires specific administrative actions.

Under the Alberta Land Titles Act, any registered mortgage creates a legal charge against the property. Because second mortgages sit in a subordinate position to primary mortgages, their removal requires precise documentation to ensure the chain of title remains intact. As Sarah Jenkins, a Real Estate Attorney at Alberta Property Law Group, explains: “An undischarged mortgage is like a financial ghost haunting your property title. Until it is formally removed at the Land Titles Office, the lender retains a legal claim, regardless of your zero balance.”

Whether you are implementing aggressive principal reduction strategies to pay off your loan early or simply reaching the end of your term, initiating the discharge process is your responsibility as the property owner.

Step-by-Step Guide to Clearing Your Property Title

Navigating the discharge process requires coordination between you, your lender, and the provincial government. Following these sequential steps will ensure a smooth transaction.

- Request a Formal Payout Statement: Contact your lender to request a legally binding payout statement. This document outlines the exact amount required to satisfy the debt on a specific date, including any prepayment penalties or administrative fees. Understanding how compounding frequency impacts your final balance is crucial here, as daily interest can change your payout amount slightly.

- Remit the Final Payment: Transfer the exact funds using a certified method, such as a wire transfer or bank draft. Retain all receipts and confirmation numbers.

- Obtain the Discharge Document: Once the funds clear, the lender must issue a formal discharge document (satisfaction piece). By law, lenders are expected to provide this within a reasonable timeframe, typically 10 to 15 business days.

- Review for Accuracy: Check the document against your original mortgage paperwork. Ensure the legal property description, instrument number, and registered names match perfectly.

- Register with Land Titles: Submit the executed discharge document to the Alberta Land Titles Office along with the required government registration fee.

Essential Documentation for a Smooth Discharge

The success of your discharge application hinges on accurate paperwork. The Alberta Land Titles Office operates on a strict compliance basis; even minor typographical errors can result in a rejected application. Research from the Law Society of Alberta indicates that 22% of self-submitted discharge applications are initially rejected due to clerical errors or mismatched legal descriptions.

To avoid delays, gather your original mortgage agreement, your current certificate of title, proof of final payment, and the lender’s discharge statement. Maintaining proper second mortgage document retention throughout the life of your loan makes this phase significantly easier. If you are navigating spousal buyouts and clearing your title simultaneously, you will also need the appropriate separation agreements or transfer of land documents.

Costs and Fees: What to Budget in 2026

While paying off the principal and interest is your primary financial hurdle, the administrative act of discharging the mortgage carries its own set of costs. Homeowners should budget between $350 and $850 for the complete process. A recent survey by the Canadian Bankers Association found that 90% of secondary lenders charge some form of administrative fee for preparing discharge documents.

| Fee Category | Estimated 2026 Cost | Description |

|---|---|---|

| Lender Administrative Fee | $100 – $300 | Charged by the lender to draft and execute the satisfaction piece. |

| Legal / Notary Fees | $200 – $500 | Professional fees for reviewing documents and facilitating registration. |

| Land Titles Registration | $50 – $100 | Government fee to process the removal of the encumbrance. |

“The biggest misconception is that the bank handles everything for free,” notes Elena Rostova, an Alberta Notary Public. “For secondary financing, the burden of registration—and the associated costs—often falls squarely on the borrower’s shoulders.”

Timelines and Processing Expectations

Patience is essential when clearing your title. The standard timeline from making your final payment to receiving a clean certificate of title spans 3 to 6 weeks. However, this timeline is subject to fluctuations based on government workloads and lender efficiency.

After remitting payment, expect a 10 to 15 business day wait for the lender to process the funds and draft the discharge document. Once submitted to the Land Titles Office, government processing typically takes an additional 5 to 10 business days. David Chen, a Senior Title Officer, warns: “In 2026, we are seeing a 30% increase in delayed property closings simply because homeowners forgot to register their second mortgage discharge documents months, or even years, prior.”

Common Pitfalls and Edge Cases

While the standard process is linear, edge cases can complicate matters. One common issue arises when dealing with private lenders who may have relocated, passed away, or dissolved their corporate entity. If a lender is unreachable and cannot sign the discharge document, you may be forced to seek a court order to clear the title, a process similar to avoiding a quiet title dispute.

Another pitfall is losing the original discharge document before it is registered. If the satisfaction piece is misplaced, the lender will need to draft a replacement, often charging a secondary administrative fee and resetting your timeline by several weeks. Marcus Thorne, a Financial Analyst at the Canadian Mortgage Institute, advises: “Always request your payout statement in writing and keep the satisfaction piece in a fireproof safe until registration is confirmed by the province.”

Why You Shouldn’t Delay the Registration

Procrastination is the enemy of a clean property title. Industry statistics reveal that up to 15% of Alberta property titles currently feature old, undischarged mortgages that have long been paid off. Leaving a satisfied mortgage on your title creates an artificial encumbrance that can severely limit your financial agility.

If you decide to sell your home, the buyer’s lawyer will demand that all encumbrances be cleared before closing. An unexpected delay in obtaining a discharge from an old second mortgage can cause the sale to fall through. Similarly, if you are considering a cash-out refinance to consolidate debt or fund renovations, new lenders will view the undischarged mortgage as active debt, drastically reducing your approved loan-to-value (LTV) ratio.

The administrative effort required to clear your title is minimal compared to the legal headaches of dealing with an outdated encumbrance during a time-sensitive real estate transaction. The process is legally analogous to discharging a lis pendens—until the paperwork is filed, the public record assumes the claim is valid.

Frequently Asked Questions (FAQ)

Does paying off my second mortgage automatically clear my title?

No. Paying off the balance only satisfies the financial debt. You must legally register a discharge document with the Alberta Land Titles Office to remove the lender’s claim from your property title.

How long does a lender have to provide a discharge document in Alberta?

While there is no strict daily limit, Alberta law requires lenders to provide discharge documents within a “reasonable time” after the debt is satisfied. In 2026, industry standard dictates this should take no longer than 15 to 30 days.

Can I register the discharge document myself?

Yes, homeowners can submit the discharge document directly to the Land Titles Office. However, due to the strict formatting and accuracy requirements, many choose to hire a lawyer or notary to ensure the application isn’t rejected.

What happens if my private lender goes out of business before discharging my mortgage?

If a corporate lender dissolves or a private lender cannot be located, you will need to apply to the Court of King’s Bench in Alberta for a court order to discharge the mortgage, proving that the debt was paid in full.

How much does the Alberta Land Titles Office charge to register a discharge?

As of 2026, the base government fee to register a mortgage discharge is relatively low, typically under $50 per instrument. However, this does not include the legal or administrative fees charged by your lender or lawyer.

Will an undischarged mortgage affect my credit score?

An undischarged mortgage does not directly lower your credit score if the account is reported as closed and paid on your credit bureau. However, it will severely impact your property’s title and your ability to secure future secured loans.

Conclusion

Discharging a second mortgage in Alberta is the vital final step in your borrowing journey. By understanding the legal requirements, budgeting for the necessary fees, and proactively managing the documentation, you can ensure your property title reflects your true 100% ownership. Don’t let an old, paid-off loan act as a roadblock to your future financial goals. Take control of your property rights and finalize the paperwork as soon as your final payment clears.

If you are struggling with an uncooperative lender, facing complex title issues, or need professional guidance navigating your secondary financing options, we are here to help. Contact us today to speak with our Alberta mortgage experts and secure your financial future.