The fundamental difference between a reverse mortgage and a second mortgage lies in cash flow requirements and age restrictions. A reverse mortgage requires zero monthly payments and is exclusively available to homeowners aged 55 and older, whereas a second mortgage mandates regular monthly payments but is accessible to any legally aged adult who meets income and credit qualifications. Both financial instruments allow Calgary homeowners to extract equity without selling their property, but they serve entirely different demographic needs, risk profiles, and long-term estate planning goals.

Key Takeaways

- Age Restrictions: Reverse mortgages are strictly for seniors (55+) and require no monthly payments, but interest compounds rapidly over time.

- Universal Access: Second mortgages are available to any qualifying adult and require monthly payments, preserving equity by preventing compound interest growth.

- Borrowing Limits: Calgary homeowners can access up to 55% of their home’s appraised value through a reverse mortgage, compared to up to 80% with a second mortgage.

- Qualification Focus: Income and credit scores are critical for second mortgage approval but are largely irrelevant for reverse mortgage underwriting.

- Market Context: In 2026’s higher interest rate environment, choosing the right product depends entirely on your monthly cash flow capacity versus your desire to leave a fully paid-off estate to heirs.

Understanding Home Equity Extraction in Calgary’s 2026 Market

In 2026, with Calgary’s benchmark detached home values stabilizing above $745,000, leveraging property equity has transitioned from a last-resort measure to a primary wealth management strategy for Albertans. However, the economic landscape heavily influences borrowing strategies. With the Bank of Canada maintaining a cautious stance on overnight rates to combat lingering inflation, borrowing costs remain significantly higher than the pre-2022 era.

Strong interprovincial migration has kept Calgary property values robust, providing homeowners with unprecedented equity reserves. As David Chen, Principal Economist at the Alberta Real Estate Research Institute, explains: “The choice between equity extraction methods in 2026 hinges entirely on cash flow capacity versus estate preservation goals. Calgary’s high property values offer a massive safety net, but the compounding interest of a reverse mortgage in a higher-rate environment demands careful calculation.”

What is a Reverse Mortgage in Calgary?

A reverse mortgage is a specialized financial product designed specifically for older homeowners. It allows individuals aged 55 and older to convert up to 55% of their primary residence’s equity into tax-free cash. The defining characteristic of this loan is the absolute absence of monthly mortgage payments. Instead, the interest compounds over time and is added to the principal balance.

The loan only becomes due when the last surviving borrower sells the home, moves into long-term care, or passes away. According to guidelines from the Financial Consumer Agency of Canada (FCAC), these products have surged in popularity as Canadians increasingly seek to age in place. Seniors can access substantial capital to fund home renovations, cover medical expenses, or gift early inheritances to children.

However, the convenience of zero monthly payments comes at a premium. Reverse mortgage interest rates are typically 1.5% to 2.5% higher than traditional mortgage rates. Because no payments are made, the debt grows exponentially, which can significantly erode the final estate value left to heirs.

What is a Second Mortgage?

A second mortgage is a traditional, subordinate loan secured against your property’s equity, sitting in second position behind your primary mortgage. Unlike a reverse mortgage, a second mortgage requires regular monthly payments of principal and interest (or interest-only, depending on the lender’s terms). This option is available to any adult homeowner who meets the lender’s income, credit, and equity requirements, with no age restrictions.

Calgary homeowners can typically borrow up to 80% of their home’s appraised value, minus the outstanding balance of their first mortgage. This Loan-to-Value (LTV) ratio provides access to significant capital. Second mortgages are highly versatile and are frequently used for debt consolidation, funding higher education, or leveraging home equity for business expansion.

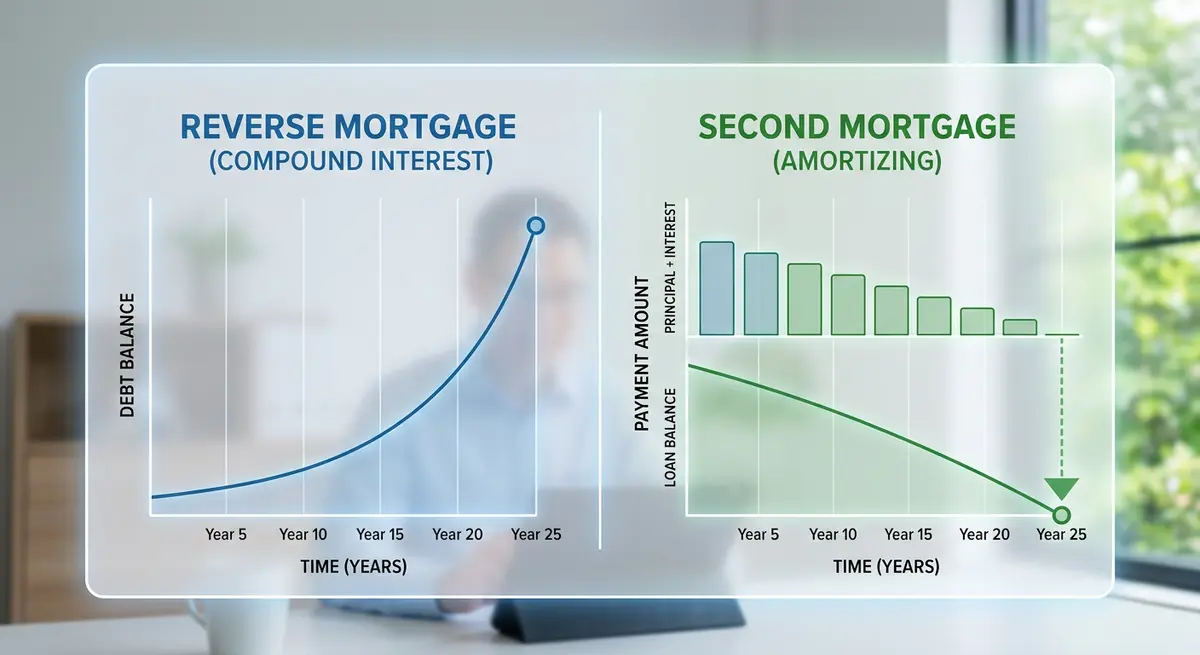

Because second mortgages require monthly payments, the principal balance decreases (or remains static in interest-only scenarios) rather than compounding negatively. This preserves your home’s equity over the long term, making it a preferred choice for borrowers with strong cash flow. If you are considering this route, you may also want to compare a second mortgage vs cash out refinance to ensure you secure the lowest possible blended interest rate.

Direct Comparison: Reverse Mortgage vs. Second Mortgage

To make an informed decision, homeowners must compare these products across several critical dimensions. The debate often comes down to immediate cash flow relief versus long-term equity preservation.

| Feature | Reverse Mortgage | Second Mortgage |

|---|---|---|

| Age Requirement | 55 years or older | 18+ (Legal adult) |

| Monthly Payments | None required | Mandatory monthly payments |

| Maximum Loan Amount | Up to 55% of home value | Up to 80% of home value (minus 1st mortgage) |

| Income Verification | Minimal to none | Strict income and employment verification |

| Interest Accumulation | Compounds and grows over time | Paid monthly (balance decreases or stays flat) |

| Primary Use Case | Retirement income, aging in place | Renovations, debt consolidation, investments |

Eligibility and Qualification Criteria

Understanding the strict qualification criteria for both products will quickly narrow down your options. Lenders assess risk differently depending on whether they require monthly payments or rely entirely on the property’s future sale value.

Qualifying for a Reverse Mortgage

Reverse mortgage lenders focus almost exclusively on the asset rather than the borrower. Because there are no monthly payments, your credit score and current income are largely irrelevant. The primary requirements include:

- Age: All titleholders must be at least 55 years old. The older you are, the higher the percentage of equity you can access.

- Property Type: The home must be your primary residence. Secondary homes, vacation properties, or dedicated rental properties do not qualify.

- Equity: You must have substantial equity. If you have an existing small mortgage, the reverse mortgage funds must first be used to pay it off entirely.

- Maintenance: Borrowers must prove they can afford ongoing property taxes, home insurance, and basic structural maintenance.

Qualifying for a Second Mortgage

Second mortgages follow traditional underwriting guidelines. Lenders must ensure you have the monthly cash flow to service the new debt alongside your existing obligations. Key criteria include:

- Credit Score: Most Calgary lenders require a minimum credit score of 600, though prime rates are reserved for scores above 680. If you have recent credit checks, you must know how to explain recent credit inquiries to your underwriter.

- Income Verification: You must provide T4s, pay stubs, or Notices of Assessment. Self-employed individuals may qualify for stated income second mortgages with alternative documentation.

- Debt Service Ratios: Your Total Debt Service (TDS) ratio generally cannot exceed 44% of your gross monthly income.

- Documentation: The application process is rigorous. Reviewing a second mortgage document checklist ensures a smooth approval process.

Sarah Jenkins, Senior Underwriter at Calgary Equity Partners, notes: “When underwriting secondary financing in Alberta, we look strictly at the borrower’s ability to service the debt. If your Total Debt Service ratio exceeds 44%, a traditional second mortgage becomes unviable, regardless of how much equity sits in the property.”

The Financial Mathematics: Compounding Interest vs. Amortization

The mathematical reality of borrowing against your home cannot be ignored. The most significant financial implication is how interest is calculated and applied.

With a second mortgage, you pay interest monthly. Your principal balance only decreases if you make amortizing payments, but even with interest-only payments, the core debt never grows. However, with a reverse mortgage, you face the reality of compound interest. Because you make no payments, the interest is added to the principal, and the following month, you are charged interest on the new, higher balance. Understanding how compounding frequency silently increases your debt is vital before signing a reverse mortgage contract.

According to 2026 housing data from the Canada Mortgage and Housing Corporation (CMHC), a $200,000 reverse mortgage at an 8% interest rate will grow to over $430,000 in just 10 years. Calgary homeowners must weigh this rapid equity erosion against their immediate need for capital.

Step-by-Step: How to Choose the Right Equity Loan

Choosing the right financial product requires a structured approach to ensure alignment with your long-term goals. Follow these steps:

- Assess Your Cash Flow: Calculate your reliable monthly income. If you cannot comfortably afford an additional $500 to $1,500 per month in loan payments, a second mortgage is likely unviable.

- Determine Your Timeline: How long do you plan to stay in the home? Reverse mortgages carry high setup fees (often $2,000 to $3,000) and are not cost-effective for short-term borrowing (under 5 years).

- Evaluate Estate Goals: Discuss your plans with your heirs. If leaving a fully paid-off home is a priority, avoid reverse mortgages. If your children are financially independent, utilizing your equity for your own comfort may be the better choice.

- Consult a Professional: Speak with a licensed Alberta mortgage broker who has access to both B-lenders for second mortgages and specialized reverse mortgage providers like HomeEquity Bank or Equitable Bank.

Real-World Calgary Case Studies (2026)

To illustrate how these products function in the real world, consider these two distinct 2026 scenarios.

Scenario A: The Retiree Aging in Place (Reverse Mortgage)

Margaret, 72, owns a detached home in Brentwood valued at $800,000, completely mortgage-free. Her pension provides enough for basic living expenses, but she needs $100,000 for accessibility renovations and a new vehicle. Because her fixed income cannot support a new monthly payment, she opts for a reverse mortgage. She receives a tax-free lump sum of $100,000. She makes no monthly payments, allowing her to maintain her lifestyle while aging comfortably in her community.

Scenario B: The Entrepreneur Expanding a Business (Second Mortgage)

James and Sarah, both 45, own a home in Mahogany valued at $900,000 with a $400,000 first mortgage. They need $150,000 to expand their local retail business. Because they are under 55, a reverse mortgage is impossible. They secure a second mortgage at an 8.5% interest rate. Their strong business revenue easily covers the $1,200 monthly interest-only payment. After five years, their business expansion pays off, and they clear the second mortgage entirely, having preserved their home’s equity.

Legal Considerations and Common Pitfalls

Navigating home equity loans in Alberta comes with specific legal and financial pitfalls. One major oversight is ignoring spousal rights. Under the Alberta Dower Act, non-title spouses are protected from having their primary residence encumbered without their consent. If you are married or in an interdependent relationship, you must understand common law partner property rights before attempting to leverage the home’s equity.

Another frequent mistake is failing to compare all available options. Some homeowners rush into a secured loan when an unsecured product might suffice for smaller amounts. Always review the pros and cons of leveraging home equity versus an unsecured line of credit to ensure you aren’t paying unnecessary legal, appraisal, and registration fees for secured debt.

Frequently Asked Questions (FAQ)

Can I lose my home with a reverse mortgage in Calgary?

You cannot lose your home as long as you meet your borrower obligations. These include paying your property taxes, maintaining home insurance, keeping the property in good repair, and living in the home as your primary residence for at least six months of the year.

Are reverse mortgage funds taxable in Canada?

No. The funds you receive from a reverse mortgage are considered a loan advance, not income. Therefore, they are completely tax-free and will not affect your Old Age Security (OAS) or Guaranteed Income Supplement (GIS) government benefits.

Can I pay off a reverse mortgage early?

Yes, you can pay off a reverse mortgage at any time. However, doing so within the first few years usually triggers significant prepayment penalties. Always review the penalty schedule in your contract before signing.

How fast can I get a second mortgage approved in Calgary?

In 2026, private second mortgages in Calgary can be approved and funded in as little as 5 to 10 business days. Institutional second mortgages from B-lenders typically take 2 to 4 weeks due to stricter income verification processes and appraisal requirements.

What happens if I default on my second mortgage?

If you fail to make your monthly payments, the second mortgage lender has the legal right to initiate foreclosure proceedings in Alberta. They can force the sale of the property to recover their funds, though the first mortgage lender is always paid first from the sale proceeds.

Is it better to get a second mortgage or refinance my first mortgage?

If you have a very low interest rate on your existing first mortgage, a second mortgage is usually better because it allows you to keep that low rate intact. Breaking a first mortgage to refinance often incurs massive penalties and forces you into today’s higher interest rates on the entire balance.

Conclusion

Deciding between a reverse mortgage and a second mortgage in Calgary requires a careful analysis of your age, income, and long-term financial objectives. While a reverse mortgage offers seniors the unparalleled freedom of accessing equity without the burden of monthly payments, the compounding interest can rapidly deplete an estate. Conversely, a second mortgage provides a flexible, lower-cost borrowing solution for adults of any age, provided they have the monthly cash flow to support the debt.

In 2026’s complex economic environment, making the wrong choice can cost tens of thousands of dollars in unnecessary interest or fees. Before signing any loan documents, it is crucial to speak with an expert who can evaluate your specific situation and present all viable options. Contact our Calgary mortgage team today to schedule a free consultation and discover the safest, most cost-effective way to unlock your home’s equity.