To qualify for a second mortgage as a self-employed individual in Calgary in 2026, borrowers must typically demonstrate a minimum credit score of 650, retain at least 20% to 35% equity in their property (capping the maximum Loan-to-Value at 80%), and provide either two years of Notice of Assessments (NOAs) or 6 to 12 months of consecutive business bank statements. Lenders also require Total Debt Service (TDS) ratios to remain below 44% and demand proof of business stability for a minimum of 24 months. By meeting these specific underwriting criteria, entrepreneurs and independent contractors can successfully access their home’s appraised equity to fund business expansion, consolidate high-interest debt, or manage seasonal cash flow fluctuations.

Key Takeaways

- Equity is Paramount: You must maintain a minimum of 20% equity in your home; most lenders cap the combined Loan-to-Value (LTV) at 80%.

- Flexible Income Verification: Alternative lenders now accept 6 to 12 months of business bank statements instead of traditional tax returns to verify gross cash flow.

- Credit Score Minimums: While traditional banks prefer scores above 680, alternative lenders will consider self-employed applicants with scores as low as 600-650.

- Stress Testing Applies: Federally regulated lenders require you to qualify at a rate 2.0% higher than your contract rate to ensure you can handle future fluctuations.

- Strategic Capital: Funds can be legally used for commercial expansion, CRA tax arrears, or inventory purchases without the high rates of unsecured business loans.

The 2026 Lending Landscape for Calgary Entrepreneurs

Securing financing as an entrepreneur presents a unique set of challenges. Unlike salaried employees who simply hand over a standard T4 slip, business owners must navigate a complex web of income verification, tax optimization strategies, and stringent federal stress tests. However, the Calgary real estate market’s dynamic economic landscape—fueled by a rapidly diversifying tech sector alongside robust traditional energy markets—has prompted financial institutions to develop highly sophisticated approaches to evaluating self-employed applications.

The financial environment for independent contractors and business owners has evolved significantly over the past few years. According to early 2026 labor data published by Statistics Canada, self-employment now accounts for nearly 15% of Alberta’s total workforce. This demographic shift has created massive demand for tailored financial products. Consequently, the mortgage market has adapted, offering more flexible underwriting guidelines while still adhering to federal risk management protocols.

Lenders evaluate self-employed applications primarily through a lens of risk mitigation. They inherently understand that business revenues fluctuate from quarter to quarter. Therefore, underwriters look for strong compensating factors—such as substantial home equity, pristine credit histories, or significant liquid reserves—to offset perceived income volatility. As David Chen, Chief Economist at the Calgary Real Estate Institute, explains: “In 2026, alternative lenders are increasingly focusing on 12-month bank statement averages rather than traditional Notice of Assessments. This allows business owners to borrow based on actual cash flow rather than heavily deducted taxable income, fundamentally changing how alternative financing for Calgary entrepreneurs is structured.”

Core Qualification Pillars for Self-Employed Borrowers

Successfully navigating the application process requires a deep understanding of four primary pillars: income verification, creditworthiness, debt service ratios, and property equity. Let us break down the exact requirements lenders demand in the current 2026 market.

1. Income Verification and Tax Documentation

Income verification remains the most critical hurdle for business owners. Traditional “A” lenders (major banks) typically require a minimum of two years of self-employment history in the exact same industry. The documentation required depends heavily on how your business is legally structured.

For Sole Proprietors, underwriters mandate two years of T1 General tax returns, including the T2125 statement of business or professional activities, alongside the corresponding Notice of Assessments (NOAs) from the Canada Revenue Agency (CRA). For Incorporated Businesses, you must provide T2 corporate tax returns, current financial statements prepared by a licensed accountant, and proof of income drawn from the corporation via T4s or T5s.

Fortunately, the market has adapted. Many alternative lenders now accept 6 to 12 months of business bank statements to prove gross revenue, bypassing the need for NOAs entirely. When applying the reasonability test to verify self-employed income, underwriters ensure that declared revenues align with industry averages. Furthermore, lenders may add back certain non-cash deductions, such as Capital Cost Allowance (CCA) or depreciation, to calculate your true qualifying income.

2. Credit Score Thresholds and History

Because self-employment carries inherent income variability, lenders demand stronger credit profiles to mitigate default risk. While traditional W-2 employees might secure secondary financing with a score of 600, self-employed applicants face stricter thresholds. Most mainstream lenders require a minimum credit score between 650 and 700. To access the most competitive interest rates, a score above 720 is highly recommended.

Lenders scrutinize your credit report for the past 24 months, looking specifically for consistency in revolving credit payments and zero instances of missed mortgage payments. If you have recent credit inquiries or minor blemishes, knowing how to explain credit inquiries to lenders through a well-crafted letter of explanation can significantly improve your approval odds.

3. Debt Service Ratios (GDS and TDS)

Your ability to manage monthly payments is quantified using two specific formulas mandated by the Financial Consumer Agency of Canada (FCAC): Gross Debt Service (GDS) and Total Debt Service (TDS).

- Gross Debt Service (GDS): This is the percentage of your gross income required to cover housing costs, including your first mortgage, the proposed second mortgage, property taxes, and heating. This ratio typically cannot exceed 35% to 39%.

- Total Debt Service (TDS): This encompasses all GDS costs plus all other debt obligations, such as credit cards, car loans, and unsecured lines of credit. Lenders generally cap the TDS ratio at 40% to 44%.

For self-employed borrowers, these ratios are rigorously stress-tested. The Bank of Canada requires federally regulated lenders to qualify borrowers at the contract rate plus 2.0%, ensuring you can withstand future rate hikes. “The stress test remains the largest hurdle for independent contractors,” notes Elena Rostova, a Calgary-based Certified Financial Planner. “Borrowers must prove they can handle payments at 2% above their contract rate, which requires meticulous financial planning and debt management.”

4. Equity and Property Valuation

A second mortgage is secured against the equity in your home. For self-employed applicants, lenders typically require a higher equity buffer to offset risk. You must maintain a minimum of 20% to 35% equity in the property after both the first and second mortgages are accounted for. This means the maximum Loan-to-Value (LTV) ratio is strictly capped at 80%.

To determine this exact figure, lenders mandate a full professional appraisal. The appraiser evaluates your home’s physical condition, recent renovations, and comparable sales in your specific Calgary neighborhood. “Maintaining a minimum of 25% equity in your property is the strongest compensating factor for income volatility,” states Marcus Thorne, Director of Mortgage Risk at Prairie Credit Union.

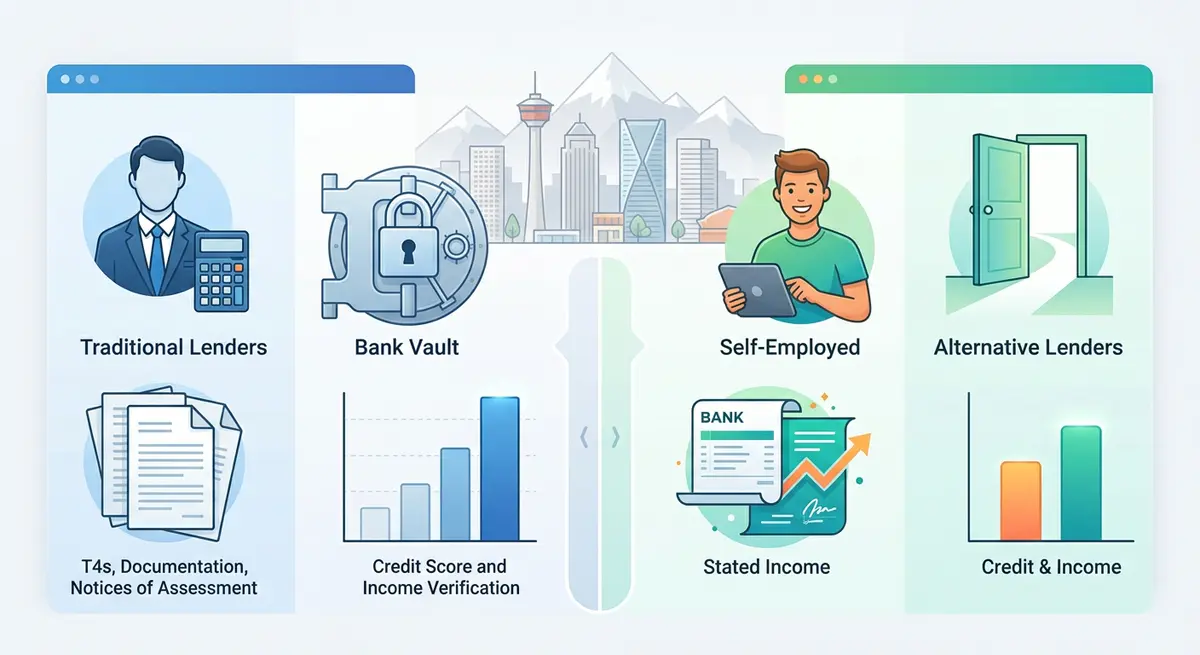

Traditional Banks vs. Alternative Lenders: A 2026 Comparison

When seeking secondary financing as a business owner in Calgary, you generally have three avenues: traditional “A” lenders (chartered banks), alternative “B” lenders (trust companies and credit unions), and private lenders. Each tier has distinct underwriting requirements.

| Lender Type | Income Verification | Min. Credit Score | Max LTV | Interest Rates |

|---|---|---|---|---|

| Traditional Banks | Strict (2 years NOAs, T1/T2) | 680 – 720+ | 80% | Lowest (Prime + 1-3%) |

| Alternative Lenders | Flexible (Bank statements) | 600 – 650 | 75% – 80% | Moderate (Prime + 3-6%) |

| Private Lenders | Equity-based (Stated income) | 500+ (Asset focused) | 65% – 75% | Highest (8% – 15%+) |

If your business heavily utilizes tax write-offs, resulting in a low taxable income, alternative or private lenders are often the most viable route. These institutions offer stated income second mortgages, focusing on gross cash flow rather than net taxable income.

Step-by-Step: How to Apply for a Self-Employed Second Mortgage

Preparation is the absolute key to securing favorable terms and avoiding unnecessary delays. Follow these actionable steps to streamline your application process in 2026:

- Organize Your Financial Paperwork: Gather your last two years of NOAs, T1/T2125 forms, or corporate financials. If applying with an alternative lender, download 12 months of pristine business bank statements. Utilize a comprehensive document checklist for Calgary secondary mortgages to ensure nothing is missed.

- Calculate Your Usable Equity: Estimate your home’s current market value and multiply it by 0.80 (80% LTV). Subtract your current first mortgage balance. The remaining figure represents your maximum potential borrowing amount.

- Optimize Your Credit Profile: Pay down revolving credit card balances to below 30% of their limits at least 45 days before applying. Do not open any new credit facilities or finance vehicles during this sensitive period.

- Prepare Liquid Reserves: Lenders prefer borrowers who hold 2 to 6 months of mortgage payments in accessible savings accounts. This proves you can weather seasonal business downturns without defaulting.

- Consult a Specialized Broker: Work with a mortgage broker who specializes in self-employed files. They can match your specific income structure with the right lender, saving you from unnecessary credit inquiries that could damage your score.

Navigating Complex Income Structures and Edge Cases

Calgary’s economy is highly diverse, meaning self-employed income rarely fits into a neat, predictable box. Fortunately, lenders have adapted their underwriting guidelines to handle various edge cases effectively.

Handling Seasonal Income and Heavy Write-Offs

Many Calgary businesses, particularly those in construction, landscaping, or specialized oilfield consulting, experience severe seasonal revenue fluctuations. Traditional lenders may view this as inherent instability. However, by providing a 24-month cash flow projection and demonstrating strong liquid reserves, you can mitigate these concerns.

Furthermore, if you aggressively write down your income to minimize your annual tax burden, you might struggle to qualify with a major bank. Understanding how Alberta entrepreneurs secure financing with low taxable income is crucial. Alternative products allow you to declare your actual gross earnings, provided they are reasonable for your industry and supported by consistent bank deposits.

Real-World Case Study: Securing Capital for Business Expansion

Consider the case of Michael, a self-employed IT consultant operating in NW Calgary. In early 2026, Michael needed $100,000 to hire two junior developers and expand his agency’s service offerings. His home was appraised at $850,000, and his first mortgage balance sat at $450,000.

Despite generating $250,000 in gross revenue, Michael’s aggressive tax write-offs reduced his net taxable income to just $65,000—far too low to qualify for a traditional bank loan under standard TDS ratios. By working with an alternative lender, Michael utilized a 12-month bank statement program. The lender verified his $250,000 gross cash flow and approved a second mortgage of $100,000. His total loan amount became $550,000, representing a highly secure 64% LTV.

This capital allowed him to scale his operations without resorting to high-interest unsecured business loans, proving the strategic value of inventory and expansion financing via home equity.

Frequently Asked Questions (FAQ)

Can I get a second mortgage in Calgary with only 1 year of self-employment?

While traditional banks strictly require 24 months of self-employment history, some alternative and private lenders in Calgary will approve an application with only 6 to 12 months of history. You will need to demonstrate strong gross revenues through bank statements and maintain a higher equity position, typically 25% or more.

What is a stated income second mortgage?

A stated income mortgage allows self-employed borrowers to declare their gross income based on business bank deposits rather than relying on net taxable income from NOAs. Lenders apply a “reasonability test” to ensure the stated income aligns with industry norms, making it ideal for business owners with significant tax write-offs.

How much equity do I need for a self-employed second mortgage?

In 2026, most Calgary lenders require you to retain at least 20% equity in your home, meaning the combined total of your first and second mortgages cannot exceed 80% of the property’s appraised value. Private lenders may restrict this further to 65% or 75% LTV depending on your credit profile and property location.

Will a lender accept my business bank statements instead of tax returns?

Yes, alternative lenders (B-lenders) frequently accept 6 to 12 months of continuous business bank statements to verify cash flow. This alternative documentation method bypasses the need for T1 Generals and NOAs, focusing instead on your actual business revenue and deposit consistency.

Does the federal mortgage stress test apply to second mortgages?

Yes, if you are borrowing from a federally regulated institution like a major bank or trust company, you must pass the stress test. This requires proving you can afford the mortgage payments at a qualifying rate that is typically 2.0% higher than your actual contract rate.

Should I get a second mortgage or do a cash-out refinance?

This depends entirely on your current first mortgage rate. If you locked in a historically low rate on your first mortgage, breaking it to refinance could trigger massive penalties and force you into a higher rate on the entire balance. In such cases, keeping the first mortgage intact and adding a second mortgage is mathematically superior. You can review a detailed comparison of second mortgages vs. cash-out refinancing to determine the best path.

Conclusion

According to the Canada Mortgage and Housing Corporation (CMHC), self-employed Canadians represent a vital and growing segment of the housing market. Securing secondary financing as a business owner in Calgary requires strategic foresight, immaculate documentation, and a clear understanding of how lenders view risk in 2026. Whether you utilize traditional tax returns or leverage alternative bank statement programs, the key is translating your business success into a language that underwriters understand.

By preparing meticulously, optimizing your credit, and maintaining healthy property equity, Calgary entrepreneurs can successfully unlock the wealth tied up in their homes to fuel their next phase of growth. If you are a business owner looking to navigate these requirements and secure the best possible terms, professional guidance is invaluable. Contact us today to discuss your unique financial situation and explore your home equity options.