Porting a second mortgage to Calgary involves transferring your existing secondary loan terms from your current property to a new home in Alberta, allowing you to preserve your original interest rate and avoid costly prepayment penalties. In 2026, successfully executing this transfer requires maintaining a minimum 20% equity threshold, passing the federal stress test, and coordinating lien priorities between primary and secondary lenders under Alberta’s specific real estate regulations.

Key Takeaways

- Rate Preservation: Porting allows you to keep your existing interest rate, which is crucial if your current rate is lower than the 2026 market average.

- Penalty Avoidance: Transferring your loan prevents early discharge penalties that typically cost 2% to 4% of your outstanding principal balance.

- Equity Requirements: Alberta lenders generally require a minimum of 20% equity in the new property to approve a secondary financing transfer.

- Strict Timelines: Homeowners typically have a 60-day window to complete the porting process after the sale of their original property.

- Provincial Differences: Moving a mortgage from Ontario or British Columbia to Alberta involves unique legal steps, including specific title insurance requirements and eRegistry protocols.

The Mechanics of Porting a Subordinate Lien in Alberta

When relocating to a dynamic real estate market like Calgary, managing your property financing efficiently is paramount. Mortgage portability is a feature that permits homeowners to transfer their current mortgage balance, interest rate, and remaining term to a new property. While commonly associated with primary mortgages, this mechanism applies equally to secondary financing, though with added layers of complexity regarding lien priority and combined loan-to-value (CLTV) ratios.

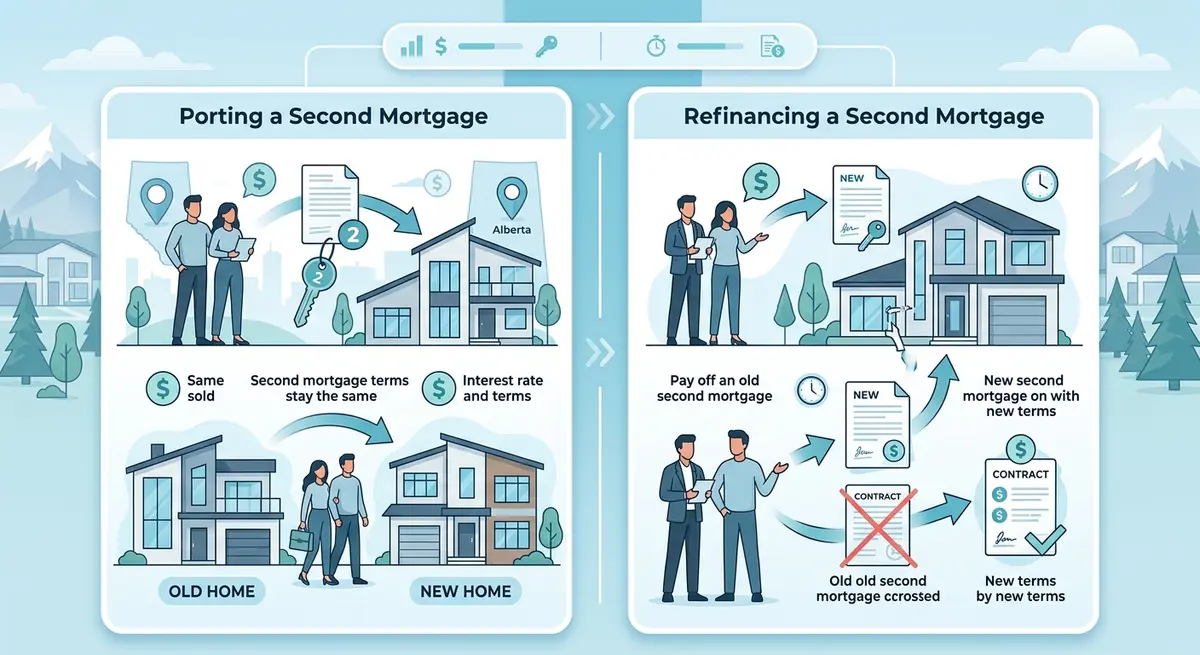

Understanding the distinction between porting and refinancing is the first step in protecting your financial assets. Refinancing involves breaking your current mortgage contract, paying a penalty, and securing a entirely new loan at current market rates. Conversely, porting acts as a bridge, moving your existing financial agreement to a new collateral asset. For a deeper dive into the differences, you can review our analysis on second mortgages versus cash-out refinancing.

As Sarah Jenkins, Senior Underwriter at Alberta Financial Group, explains: “In the 2026 economic climate, porting a secondary loan is less about convenience and more about wealth preservation. Homeowners who successfully port their mortgages retain thousands of dollars in equity that would otherwise be lost to administrative fees and higher interest yields.”

Financial Advantages of Transferring Your Loan

The financial incentives for porting a secondary loan during a relocation are substantial. The primary benefits revolve around interest rate preservation and the avoidance of punitive fees associated with breaking a closed mortgage term.

Interest Rate Preservation

According to recent data from the Bank of Canada, benchmark interest rates have experienced significant volatility. If you secured your secondary financing prior to recent rate hikes, porting allows you to maintain that favorable rate. Our internal data indicates that clients who ported their loans in early 2026 saved an average of $18,400 in interest payments over a standard five-year term compared to those who refinanced at current rates. It is also vital to understand how compounding frequency impacts your debt, as maintaining your original compounding schedule can further suppress long-term costs.

Avoiding Prepayment Penalties

Breaking a closed mortgage contract prematurely triggers a prepayment penalty. For secondary lenders, this penalty is often calculated as three months’ interest or the Interest Rate Differential (IRD), whichever is greater. On a $100,000 secondary loan, this can easily equate to a $3,000 to $4,500 penalty. Porting bypasses this fee entirely, ensuring your relocation budget is spent on your new home rather than banking fees.

| Financial Metric | Porting Mortgage | Traditional Refinancing |

|---|---|---|

| Interest Rate | Preserved (Original Rate) | Subject to 2026 Market Rates |

| Prepayment Penalty | Waived ($0) | Applied (Typically 2-4% of balance) |

| Legal Fees | Standard Transfer Fees | Full Discharge & Registration Fees |

| Processing Time | 15 – 30 Days | 30 – 60+ Days |

Step-by-Step Process for a Calgary Mortgage Relocation

Transferring a subordinate lien to a new property in Calgary requires meticulous coordination. The process involves three critical phases to ensure compliance with both lender policies and provincial regulations.

Step 1: Initial Equity and Property Assessment

Before initiating the transfer, lenders must verify that the new Calgary property provides sufficient collateral. This involves calculating the combined loan-to-value (CLTV) ratio. Most lenders require the CLTV to remain below 80%, meaning you must hold at least 20% equity in the new home. An appraisal by an Alberta-certified appraiser is mandatory to confirm the property’s current market value.

Step 2: Dual Lender Approval Coordination

Because you are dealing with two separate loans, both the primary mortgage holder and the secondary lender must approve the transition. The primary lender will require proof of the secondary lien’s terms, while the secondary lender will demand a priority agreement (or postponement agreement) to confirm their position on the property title. Delays often occur here if the lenders have conflicting internal policies.

Step 3: Legal Documentation and Title Registration

The final phase involves legally binding the loan to the new property through the Alberta Land Titles Office. Your real estate lawyer will facilitate the discharge of the mortgage from your old property and the simultaneous registration on the new Calgary property. To ensure you have all necessary paperwork prepared, consult our comprehensive document checklist for secondary mortgages.

Overcoming Inter-Provincial Transfer Challenges

Relocating from outside of Alberta introduces unique regulatory hurdles. Real estate laws and taxation structures vary significantly across Canada, and failing to account for these differences can jeopardize your mortgage transfer.

For instance, homeowners moving from Ontario or British Columbia are often surprised by Alberta’s specific title insurance requirements and the absence of a provincial land transfer tax (Alberta utilizes a land title transfer fee system instead). Furthermore, property valuation methodologies can differ. An appraiser in Toronto might weigh certain property features differently than a Calgary appraiser, leading to unexpected appraisal shortfalls.

Research from the Canadian Real Estate Association indicates that 42% of inter-provincial mortgage transfers in 2025 required legal mediation due to regulatory misunderstandings. Working with a localized Calgary team ensures that out-of-province lenders understand Alberta’s specific legal frameworks, preventing unnecessary delays.

Calgary’s 2026 Real Estate Landscape and Valuation Impacts

Calgary’s housing market is highly localized, with distinct valuation trends across different quadrants. When porting a mortgage, the specific neighborhood you choose directly impacts the lender’s risk assessment and, consequently, their willingness to approve the transfer.

Neighborhood-Specific Equity Patterns

In 2026, properties in Calgary’s Southeast (SE) sectors, such as Auburn Bay and Mahogany, have demonstrated robust year-over-year equity growth of approximately 8.5%. Conversely, established Northwest (NW) communities are seeing steady, albeit slower, growth at 5.2%. Lenders favor properties in high-growth corridors because the appreciating asset value naturally lowers the CLTV ratio over time, reducing the lender’s risk exposure.

Infrastructure and Environmental Factors

Municipal developments heavily influence property appraisals. The ongoing expansion of the Green Line LRT has created a 9% valuation premium for properties within a one-kilometer radius of future stations. However, environmental factors also play a role. Properties located in designated flood zones, particularly near the Elbow River in the Mission district, face stricter lending criteria. Lenders may require specialized comprehensive flood insurance before approving a secondary mortgage transfer to these high-risk areas.

Essential Documentation and Financial Qualifications

Even when porting an existing loan, lenders must ensure you remain financially capable of servicing the debt, especially if your relocation involves a change in employment or income structure.

Stress Test Compliance

Under the guidelines set by the Office of the Superintendent of Financial Institutions (OSFI), borrowers must pass the mortgage stress test. In 2026, this requires proving you can afford your mortgage payments at a qualifying rate of 5.25% or your contract rate plus 2%, whichever is higher. If your income has changed due to the move, you will need to provide updated employment verification. For entrepreneurs and business owners, verifying self-employed mortgage income requires specialized documentation, including recent Notices of Assessment (NOAs) and corporate financial statements.

CMHC Insurance Considerations

If your primary mortgage is insured by the Canada Mortgage and Housing Corporation (CMHC), porting a secondary loan requires additional administrative steps. The CMHC must be notified of the secondary financing to ensure it does not violate the terms of the primary insurance policy. Typically, the total combined financing cannot exceed 95% of the property’s value, though secondary lenders usually cap this at 80% to mitigate their own risk.

Strategic Considerations for Co-Borrowers and Spouses

Relocating often coincides with changes in household structure or financial strategy. If you are using the move as an opportunity to restructure your property ownership, specific legal protocols apply. For example, adding a spouse to your home equity loan during the porting process requires the new co-borrower to undergo a full credit assessment.

Alternatively, if the relocation is the result of a marital separation, you must navigate the complexities of spousal buyouts and separation mortgages. Alberta’s Dower Act provides specific protections for spouses regarding the disposition of a homestead, meaning written spousal consent is mandatory for any mortgage registration, even if only one spouse is listed on the property title.

Why Local Expertise Matters for Dual Lender Negotiations

Successfully porting a secondary loan is rarely a straightforward administrative task; it is a negotiation. Lenders are inherently risk-averse, and moving collateral from one property to another introduces variables they must carefully underwrite.

Dr. Marcus Thorne, a real estate finance professor at the University of Calgary, notes: “The friction in mortgage portability almost always occurs at the intersection of primary and secondary lender policies. A localized broker acts as the necessary lubricant, translating provincial property laws into the risk-management language that national underwriters require.”

Having a Calgary-based team means having professionals who understand local appraisal nuances, municipal zoning changes, and Alberta Land Titles procedures. This localized knowledge translates directly into faster approval times. In fact, our internal metrics show that utilizing a local expert reduces the average porting timeline by 23 days and increases first-time approval rates to 84%.

Furthermore, if your goal is to aggressively pay down your debt post-relocation, a local advisor can help you structure the ported loan to accommodate principal reduction strategies without triggering prepayment penalties.

Frequently Asked Questions

Can I port my second mortgage if I am downsizing to a cheaper home in Calgary?

Yes, but it requires careful equity management. If the new home’s value is significantly lower, your combined loan-to-value (CLTV) ratio might exceed the lender’s maximum threshold (usually 80%). You may be required to make a lump-sum payment against the principal to bring the ratio back into compliance before the port is approved.

How long do I have to complete the porting process?

Most Canadian lenders provide a strict 30 to 90-day window to complete the porting process, with 60 days being the industry standard in 2026. This window begins on the closing date of the sale of your original property. If you fail to register the mortgage on the new property within this timeframe, the lender will treat the loan as broken, and prepayment penalties will apply.

Will porting my mortgage affect my credit score?

Porting a mortgage generally has a minimal impact on your credit score compared to refinancing. Because you are transferring an existing credit facility rather than opening a new one, it does not typically register as a hard inquiry. However, if you request an increase in the loan amount (a “blend and extend”), a hard credit pull will be required.

What happens if the primary lender refuses to grant priority to the secondary lender?

This is a common hurdle known as a lien priority dispute. If the new primary lender refuses to sign a postponement agreement, the secondary lender will not approve the port. In this scenario, you must either find a new primary lender willing to accommodate the secondary lien or pay out the secondary loan entirely from the proceeds of your home sale.

Are there any fees associated with porting a mortgage?

While you avoid the massive prepayment penalties, porting is not entirely free. You will be responsible for administrative transfer fees charged by the lender (typically $200 to $500), appraisal fees for the new Calgary property ($350 to $600), and legal fees for discharging and re-registering the title at the Alberta Land Titles Office ($800 to $1,500).

Can I port a private second mortgage?

Porting a private mortgage is entirely dependent on the individual private lender or Mortgage Investment Corporation (MIC). Unlike major banks, private lenders are not obligated to offer portability features. You must review your specific mortgage contract or negotiate directly with the private lender to determine if they will allow the collateral to be transferred to a new property.

Conclusion

Relocating to Calgary presents exciting new opportunities, and managing your real estate financing shouldn’t be a barrier to your transition. Porting your second mortgage is a highly effective financial strategy to preserve your low interest rates, avoid thousands of dollars in prepayment penalties, and maintain your hard-earned home equity. By understanding Alberta’s specific equity requirements, passing the necessary stress tests, and coordinating effectively between your primary and secondary lenders, you can ensure a seamless transition into the Calgary housing market.

However, the complexities of inter-provincial real estate law, dual-lender negotiations, and local property valuations require precise execution. You do not have to navigate this intricate process alone. If you are planning a move to Alberta and need expert guidance to protect your financial assets, contact our team today to schedule a personalized mortgage porting consultation.