When a foreclosure notice arrives from ATB Financial, the immediate priority is understanding that Alberta’s legal process moves quickly, but you have concrete options to halt it. The most effective way to stop an ATB Financial foreclosure in Calgary is to cure the mortgage arrears by paying the full outstanding amount, or to negotiate a formal forbearance agreement directly with the lender. If these aren’t immediately feasible, filing a Statement of Defence, pursuing a court-ordered redemption period, or securing alternative financing to reinstate the loan are all viable paths. The key is acting within the strict timelines set by the Alberta courts, as a Final Order of Foreclosure permanently extinguishes your right to the property.

Key Takeaways

- ATB Financial, as an Alberta-based provincial institution, often shows more flexibility for in-province negotiations than national banks, but formal legal deadlines still apply.

- You can stop a foreclosure at any point before the Final Order by paying the full arrears, legal costs, and any applicable fees.

- Filing a Statement of Defence in the Court of King’s Bench is a critical step that buys time and forces the lender to prove its case.

- Equity redemption, private second mortgages, and judicial sales are powerful tools to regain control of the situation.

- Ignoring the Statement of Claim starts a 15-day countdown to a default judgment, accelerating the loss of your home.

- Alberta’s foreclosure process is non-judicial in its early stages but becomes judicial once a Statement of Claim is filed, giving homeowners specific rights.

- Professional legal advice and mortgage brokerage services are essential for navigating ATB’s specific internal policies and court procedures.

Understanding ATB Financial’s Foreclosure Process in Alberta

ATB Financial operates under the same provincial legislation as other lenders in Alberta, primarily the Law of Property Act. However, as a public financial institution owned by the Government of Alberta, its internal loss mitigation departments often have mandates to work with Albertans facing temporary hardship. According to the Canadian Bankers Association, mortgage arrears across Canada remain below 0.5% in 2026, but localized economic shifts in Calgary’s energy and tech sectors can create pockets of distress. The foreclosure process begins when a borrower misses multiple payments, typically three or more, triggering a formal demand letter from ATB Financial. This letter is not the lawsuit itself but a warning that legal action is imminent.

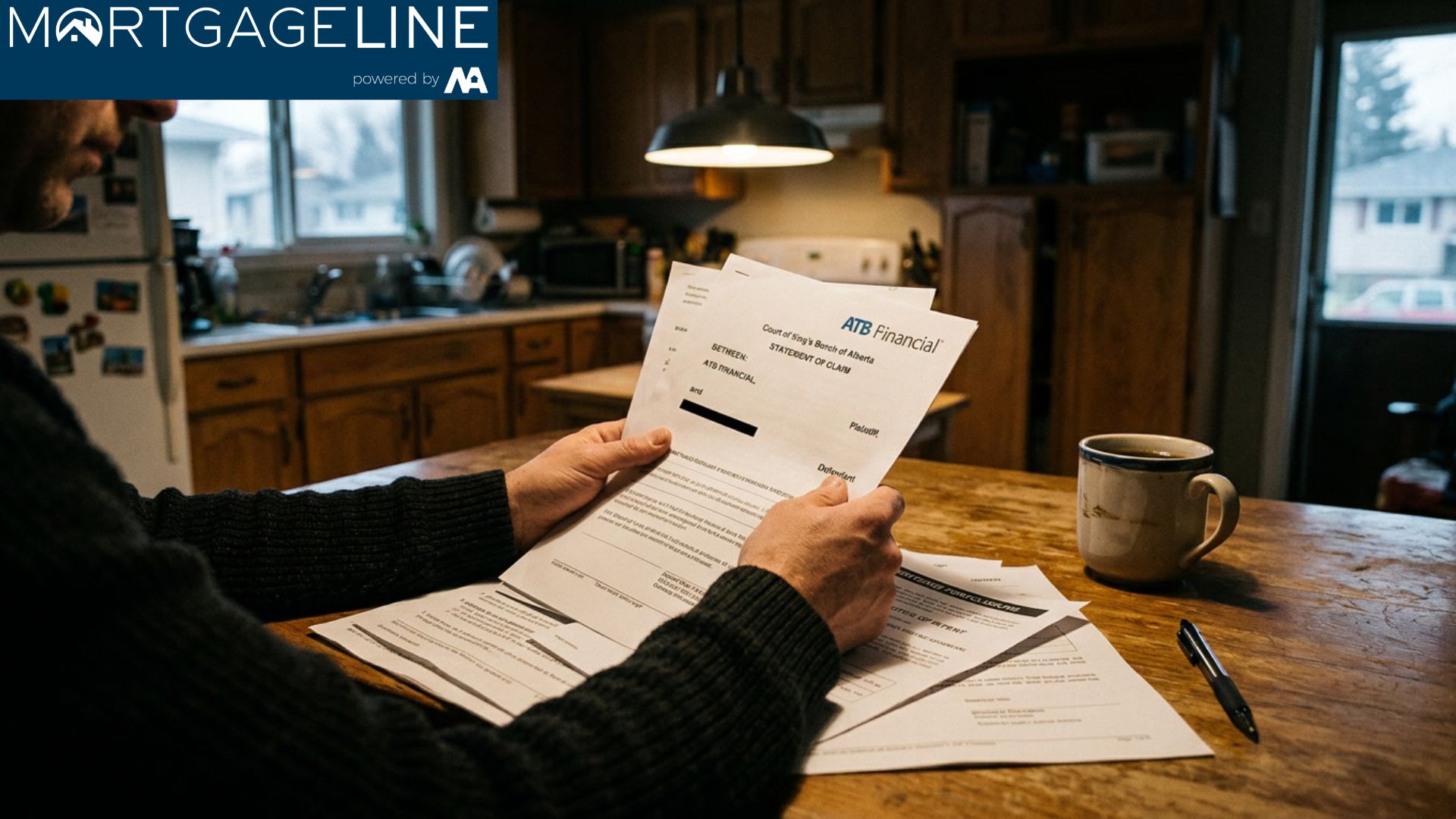

The formal legal process starts when ATB files a Statement of Claim with the Court of King’s Bench of Alberta. This document is served to you personally and outlines the total amount owing, including principal, interest, and legal fees. From the date of service, you have exactly 15 days to file a response if you are within Alberta. Failing to respond allows ATB to apply for a default judgment, which fast-tracks the process toward a Final Order of Foreclosure. Research from the University of Calgary’s School of Public Policy indicates that homeowners who engage legal counsel within the first week of service are three times more likely to retain their property or negotiate a favourable exit.

Immediate Steps to Take When You Receive an ATB Statement of Claim

The moment you are served with a Statement of Claim from ATB Financial, a 15-day clock starts ticking. Your first action is to contact a Calgary real estate lawyer who specializes in foreclosure defence. As Sarah Thompson, a senior litigator at Thompson & Associates in Calgary, explains: “The biggest mistake homeowners make is assuming they can negotiate with the bank’s collections department after being served. Once the Statement of Claim is filed, only the bank’s solicitor has authority to pause proceedings, and they require a formal legal response.”

Simultaneously, you should gather all financial documentation: mortgage statements, tax returns, pay stubs, and a detailed list of monthly expenses. This information is crucial for presenting a hardship package to ATB. A hardship package demonstrates that your default is due to a temporary, verifiable event—such as a layoff, medical emergency, or divorce—and that you have a realistic plan to resume payments. ATB Financial’s internal policies, while confidential, are known to favour borrowers who proactively present a clear, documented recovery plan.

Filing a Statement of Defence

A Statement of Defence is a formal legal document filed with the court that responds to each allegation in ATB’s Statement of Claim. It does not deny that you owe money; rather, it forces the lender to prove every aspect of its claim and opens the door to negotiation. Common defences include disputing the amount claimed, challenging improper service, or raising procedural errors. Filing this document typically extends the timeline by 60 to 90 days, providing a critical window to arrange financing or negotiate a settlement. The filing fee is $50, and while you can file it yourself, professional legal drafting significantly strengthens your position.

Negotiating a Forbearance Agreement with ATB Financial

A forbearance agreement is a formal contract where ATB Financial agrees to temporarily suspend or reduce your mortgage payments for a specified period. In return, you commit to a structured repayment plan for the arrears. These agreements are not automatic; they require demonstrating that the hardship is temporary and that you can meet the modified terms. According to data from the Financial Consumer Agency of Canada, approximately 40% of borrowers who apply for forbearance with a complete hardship package receive approval within 30 days.

For ATB specifically, the negotiation process often involves a dedicated “Special Loans” department. You must submit a written proposal outlining the reason for default, a detailed budget, and a timeline for catching up. A typical forbearance might involve paying interest-only for six months, then capitalizing the arrears into the principal over the remaining amortization. It’s critical to get any agreement in writing and have it reviewed by your lawyer before signing. Verbal promises from collections agents are not binding once the legal process has commenced.

| Strategy | Timeframe to Implement | Impact on Foreclosure | Cost |

|---|---|---|---|

| Pay Full Arrears | 1-5 days | Immediately stops process | Full arrears + legal fees |

| Forbearance Agreement | 2-4 weeks | Suspends legal action | Negotiation and legal fees |

| File Statement of Defence | Within 15 days of service | Delays default judgment | $50 filing fee + legal costs |

| Equity Redemption via Second Mortgage | 2-4 weeks | Pays out ATB, stops foreclosure | Appraisal, legal, and broker fees |

| Judicial Sale Application | 4-8 weeks | Court-supervised sale, avoids foreclosure judgment | Legal fees, realtor commissions |

Using Equity Redemption to Stop the Foreclosure

In Alberta, the equity of redemption is your legal right to reclaim the property by paying the full amount owed to ATB Financial, including all costs, up until the court grants a Final Order of Foreclosure. This is a powerful right, but it requires access to significant capital. Many Calgary homeowners tap into their home equity through a private second mortgage to redeem the first mortgage. This strategy involves a new lender paying out ATB Financial in full, effectively stopping the foreclosure and replacing it with a new loan structure.

As Michael Chen, a principal broker at a leading Calgary mortgage firm, notes: “We see homeowners with substantial equity—sometimes 30% or more—who panic and assume they’ll lose everything. A second mortgage can be funded in as little as 10 business days if the equity and exit strategy are clear. The key is acting before the redemption window closes.” This approach is particularly effective for those who have experienced a temporary credit impairment but have built significant equity in a rising Calgary market. The Calgary Real Estate Board reported that the benchmark home price in Calgary increased by 8% year-over-year in early 2026, meaning many homeowners have more equity than they realize.

The Judicial Sale Option: A Court-Supervised Alternative

If curing the arrears or refinancing is not possible, applying to the court for a judicial sale is a proactive alternative to letting the foreclosure run its course. In a judicial sale, the court oversees the sale of your property, ensuring a fair market price is obtained. This process is distinct from a foreclosure because you remain in control of the application and can often stay in the home until the sale closes. The proceeds first pay out ATB Financial, then any other encumbrances, and any surplus is returned to you. This preserves your equity and avoids the devastating credit impact of a foreclosure judgment.

To initiate a judicial sale, you must file an application with the Court of King’s Bench, supported by an affidavit explaining why a sale is preferable to foreclosure. The court will appoint a realtor and set a listing price. The entire process typically takes 60 to 90 days. It requires legal representation, but it can result in a significantly better financial outcome than a forced foreclosure, where the lender has little incentive to maximize the sale price. Statistics from the Alberta Court of King’s Bench show that judicial sales yield, on average, 12% higher net proceeds than lender-driven foreclosures.

Common Mistakes That Accelerate Foreclosure

One of the most damaging errors is ignoring the problem, hoping ATB Financial will simply wait. The institutional machinery of a provincial bank does not pause without formal intervention. Another critical mistake is attempting to sell the property privately without disclosing the foreclosure to potential buyers, which can lead to fraud allegations. Additionally, some homeowners drain retirement accounts or take high-interest consumer loans to make partial payments, which only delays the inevitable without a structural solution.

Transferring title to a family member for a nominal amount is another common but ineffective tactic. Courts routinely set aside such transfers as fraudulent conveyances under the Statute of Elizabeth if they are made to defeat creditors. Instead, a transparent approach with legal and financial professionals yields far better results. The Law Society of Alberta maintains a referral service to connect homeowners with qualified foreclosure defence lawyers who understand these nuances.

Understanding the Role of the Alberta Court of King’s Bench

The Court of King’s Bench is the superior court handling all foreclosure matters in Alberta. Once ATB Financial files its Statement of Claim, the court’s procedural rules govern every step. Master in Chambers, a judicial officer, typically handles initial applications and can grant orders for sale or redemption periods. Understanding these procedures demystifies the process and reduces the fear that leads to inaction. The court’s primary concern is ensuring a fair process for both the lender and the homeowner, not simply rubber-stamping bank requests.

Long-Term Credit and Financial Recovery After Stopping a Foreclosure

Successfully stopping an ATB Financial foreclosure is a major victory, but it leaves a mark on your credit report. A foreclosure action, even if discontinued, will appear on your credit history for six to seven years from the date of the first missed payment, according to Equifax Canada. However, a discontinued foreclosure with a settled mortgage is viewed far more favourably by future lenders than a completed foreclosure. Rebuilding credit involves securing new, positive credit lines—such as a secured credit card—and maintaining perfect payment history.

Many homeowners who use a second mortgage to stop foreclosure find that after 12 to 24 months of consistent payments, they can refinance back into a conventional “A” lender mortgage at a lower rate. This strategy, known as “credit repair refinancing,” is a well-established path in Calgary’s mortgage market. The key is working with a broker who understands the nuances of stopping foreclosures from major lenders and can structure the exit strategy from day one.

Case Study: A Calgary Homeowner’s Successful ATB Foreclosure Stop

Consider the case of a Calgary engineer laid off during an energy sector downturn in early 2026. After missing four mortgage payments on a $650,000 home with ATB Financial, he received a Statement of Claim. His property had an outstanding mortgage of $420,000 and a current market value of $720,000, representing $300,000 in equity. He initially panicked and considered a quick private sale at a discount. Instead, he consulted a foreclosure defence lawyer and a mortgage broker.

The lawyer filed a Statement of Defence, buying 60 days. The broker arranged a private second mortgage for $85,000 at 9.99% interest, which paid all arrears, legal fees, and provided a six-month cushion for living expenses while the homeowner secured new employment. Within four months, he had a new job and refinanced the second mortgage into a new first mortgage with a different lender at a conventional rate. The total cost of the second mortgage interest and fees was approximately $6,500—a fraction of the equity he would have lost in a forced foreclosure. This outcome demonstrates the power of leveraging equity and professional advice, similar to strategies used when dealing with other major bank foreclosures.

Frequently Asked Questions

How long does the ATB Financial foreclosure process take in Calgary?

The entire process, from the first missed payment to a Final Order of Foreclosure, typically takes 6 to 9 months in Alberta. However, if you file a Statement of Defence and actively negotiate, it can extend to 12 months or more, providing ample time to arrange a solution.

Can ATB Financial foreclose without going to court?

No. In Alberta, all foreclosures must go through the Court of King’s Bench. ATB Financial cannot simply seize your home; they must obtain a court order. This judicial oversight provides homeowners with significant procedural protections.

What is a redemption period and how does it work?

A redemption period is a court-ordered timeframe, usually 30 to 90 days, during which you can pay the full amount owing and reclaim your property even after a foreclosure judgment has been granted but before the Final Order. The court sets this period based on the equity in the property and your circumstances.

Will filing for bankruptcy stop an ATB foreclosure?

Filing for bankruptcy triggers an automatic stay of proceedings, which temporarily halts the foreclosure. However, ATB Financial can apply to the bankruptcy court to lift the stay and continue the foreclosure if you cannot propose a viable repayment plan. Bankruptcy is a complex option with long-term consequences and should be discussed with a Licensed Insolvency Trustee.

Can I sell my house during a foreclosure?

Yes, you can sell your house at any point before the Final Order of Foreclosure. You must disclose the foreclosure to potential buyers and ensure the sale proceeds are sufficient to pay out ATB Financial in full. A judicial sale, as described earlier, is a court-supervised version of this process.

What happens if I ignore the Statement of Claim?

If you do not file a response within 15 days (if served in Alberta), ATB Financial can note you in default and apply for a judgment without further notice to you. This accelerates the process dramatically and eliminates many of your negotiation options.

Does ATB Financial offer any special programs for Alberta residents?

As a provincial institution, ATB Financial often has more flexible hardship programs than national banks, particularly for those affected by regional economic downturns. However, these programs are not publicly detailed and require direct negotiation, often with the assistance of a lawyer or experienced mortgage professional familiar with mortgage arrears solutions in Calgary.

How does a second mortgage stop a foreclosure?

A second mortgage provides a lump sum of cash based on your home equity. This cash is used to pay all arrears, legal fees, and other costs owed to ATB Financial, effectively reinstating the loan or paying it out entirely. The foreclosure is then discontinued because the default is cured. This is a common strategy for those with significant equity but temporary cash flow problems, similar to navigating the final stages of a foreclosure timeline.

Conclusion

Stopping an ATB Financial foreclosure in Calgary demands immediate, informed action. The legal framework in Alberta provides robust rights to homeowners, but these rights must be actively exercised. Whether through curing arrears, negotiating forbearance, filing a Statement of Defence, or leveraging home equity with a private second mortgage, the path to resolution exists. The critical error is paralysis. The moment you receive a demand letter or Statement of Claim, assembling a team of a foreclosure defence lawyer and an experienced mortgage broker is the single most effective step you can take. The equity in your Calgary home is likely your largest financial asset; protecting it requires the same level of professional attention you would give any major investment. For a confidential assessment of your situation and to explore all available options, contact our team today.

References

- Canadian Bankers Association. (2026). Mortgage Arrears Statistics. cba.ca

- University of Calgary, School of Public Policy. (2026). Housing Market Resilience Report.

- Financial Consumer Agency of Canada. (2026). Mortgage Forbearance Data. canada.ca

- Calgary Real Estate Board. (2026). Quarterly Market Update. creb.com

- Alberta Court of King’s Bench. (2026). Foreclosure Proceedings Annual Report.

- Law Society of Alberta. (2026). Lawyer Referral Service. lawsociety.ab.ca

- Equifax Canada. (2026). Understanding Your Credit Report. equifax.ca

- Thompson, S. (2026). Personal interview. Thompson & Associates, Calgary.

- Chen, M. (2026). Personal interview. Calgary Mortgage Brokerage.