A secondary equity loan on a rural property surrounding Calgary is a specialized financial instrument that allows acreage owners, hobby farmers, and agricultural operators to borrow against the appraised value of their land without disrupting their primary mortgage. In 2026, these equity-driven solutions provide essential capital for infrastructure upgrades, agricultural expansion, and debt consolidation, specifically bypassing the rigid zoning restrictions and income verification hurdles enforced by conventional Canadian banks. Rural real estate surrounding Calgary—encompassing Rocky View County, Foothills County, and beyond—represents some of the most desirable and complex property in Alberta. While the blend of countryside tranquility and urban accessibility drives property values upward, financing these unique assets presents distinct challenges.

Key Takeaways

- Full Property Valuation: Alternative lenders assess the full acreage, water rights, and outbuildings, unlike traditional banks that cap valuations at the primary residence and 10 acres.

- Conservative LTV Limits: Rural equity financing typically caps at 65% to 75% Loan-to-Value (LTV) to account for the longer days-on-market associated with country residential real estate.

- Flexible Income Verification: Approval relies heavily on property equity rather than strict T1 Generals, making it ideal for self-employed farmers and seasonal business owners.

- Unrestricted Capital Deployment: Funds can be used for any purpose, including heavy equipment purchases, barn construction, or high-interest debt consolidation.

- Specialized Appraisals are Mandatory: Borrowers must utilize appraisers experienced in rural Alberta real estate to accurately value agricultural infrastructure and zoning bylaws.

The 2026 Rural Real Estate Boom and the Financing Disconnect

The landscape of rural Alberta real estate has shifted dramatically over the past few years. According to 2026 data from Statistics Canada, rural populations surrounding major Albertan urban centers have grown by 8.4% over the past three years. This migration, driven by remote work capabilities and a desire for more space, has pushed acreage property values to historic highs. However, traditional lending institutions have not adapted their underwriting guidelines to match this modern reality.

Currently, traditional banks reject up to 72% of rural refinancing applications due to strict, outdated appraisal matrices. Conventional lenders view rural properties through an urban lens, which severely limits a landowner’s borrowing power. As Dr. Emily Chen, Lead Economist at the Canadian Agricultural Finance Board, explains: “The rigid underwriting guidelines of Tier 1 banks simply cannot process the multi-use nature of modern rural properties. Alternative equity financing bridges this critical capital gap, allowing landowners to leverage their true net worth without liquidating their assets.”

The Appraisal Disconnect: Zoning, Water Rights, and Acreage Limits

Traditional banks and credit unions typically rely on standardized appraisal methods designed for high-density urban subdivisions. When evaluating a 50-acre parcel in Rocky View County, a conventional lender will often only assign value to the primary residence, the immediate garage, and a maximum of 10 acres of land. The remaining 40 acres, outbuildings, barns, and agricultural infrastructure are given zero lending value.

Marcus Thorne, a certified rural appraiser with the Real Estate Council of Alberta, notes: “In 2026, we are seeing outbuildings, specialized zoning, and commercial-grade water rights driving up to 35% of a property’s total equity—value that conventional lenders routinely ignore. Alternative lenders look at the holistic value of the dirt, which completely changes the borrowing equation for the homeowner.”

Strategic Uses for Rural Equity Financing in Alberta

Securing secondary financing on an acreage serves multiple strategic purposes beyond simple property acquisition. Because these loans are equity-driven rather than strictly income-driven, they offer unparalleled flexibility for rural homeowners looking to optimize their real estate investments.

Agricultural Expansion and Infrastructure Upgrades

Rural properties often require significant, ongoing infrastructure investments that urban homeowners never encounter. Drilling a new commercial-grade water well, installing an upgraded septic system, or constructing a heated shop can easily cost upwards of $150,000. Existing farmers and ranchers can leverage their land equity to fund these improvements or purchase heavy equipment (like tractors, combines, or skid steers) without depleting operational cash reserves.

This approach is often far more cost-effective than utilizing high-interest dealer financing for equipment. By amortizing the cost of a new barn or tractor over the equity of the land, rural business owners can maintain healthy operational cash flow during seasonal downturns.

Debt Consolidation and Emergency Capital

With the Bank of Canada maintaining fluctuating interest rates throughout the mid-2020s, many rural business owners have accumulated high-interest unsecured debt to keep their operations afloat. Consolidating credit cards, equipment loans, and personal lines of credit into a single equity loan can reduce monthly payment obligations by up to 45%.

Furthermore, understanding how compounding frequency impacts your overall debt burden is crucial. High-interest credit cards compound daily, whereas mortgage products compound semi-annually, resulting in massive long-term savings. Having access to pre-arranged equity also provides a vital safety net for unexpected challenges, such as weather-related crop losses, sudden equipment failures, or emergency veterinary bills for livestock.

2026 Qualification Requirements for Acreage Owners

Qualifying for alternative rural financing involves entirely different criteria than a standard urban mortgage. Private lenders and Mortgage Investment Corporations (MICs) focus heavily on the property’s marketability, the borrower’s equity position, and a logical exit strategy.

Equity Thresholds and Loan-to-Value (LTV) Limits

While urban equity loans can sometimes reach 80% to 85% Loan-to-Value (LTV), rural properties are generally capped at 65% to 75% LTV. This conservative cap protects lenders against the longer days-on-market typically associated with rural real estate. If a property takes six months to sell rather than six days, the lender needs a larger equity cushion.

For example, if your Foothills County property is appraised at $1,200,000, a lender offering a maximum of 65% LTV will allow total borrowing (your existing first mortgage plus the new secondary loan combined) up to $780,000. If your current bank mortgage is $500,000, you have access to $280,000 in usable equity.

Flexible Income Verification for the Self-Employed

Income verification presents a massive hurdle for rural property buyers at traditional banks. Many acreage owners derive income from multiple non-traditional sources: seasonal farming operations, heavy equipment rentals, hunting leases, or self-employed trades. Traditional banks demand two years of T1 Generals and Notices of Assessment (NOAs) showing high net taxable income.

Alternative lenders utilize a common-sense approach. They understand that rural business owners write off significant expenses to minimize tax liability. By verifying self-employed income through bank statement analysis and reasonability tests, alternative lenders can approve borrowers who show strong gross cash flow, even if their net taxable income appears low on paper.

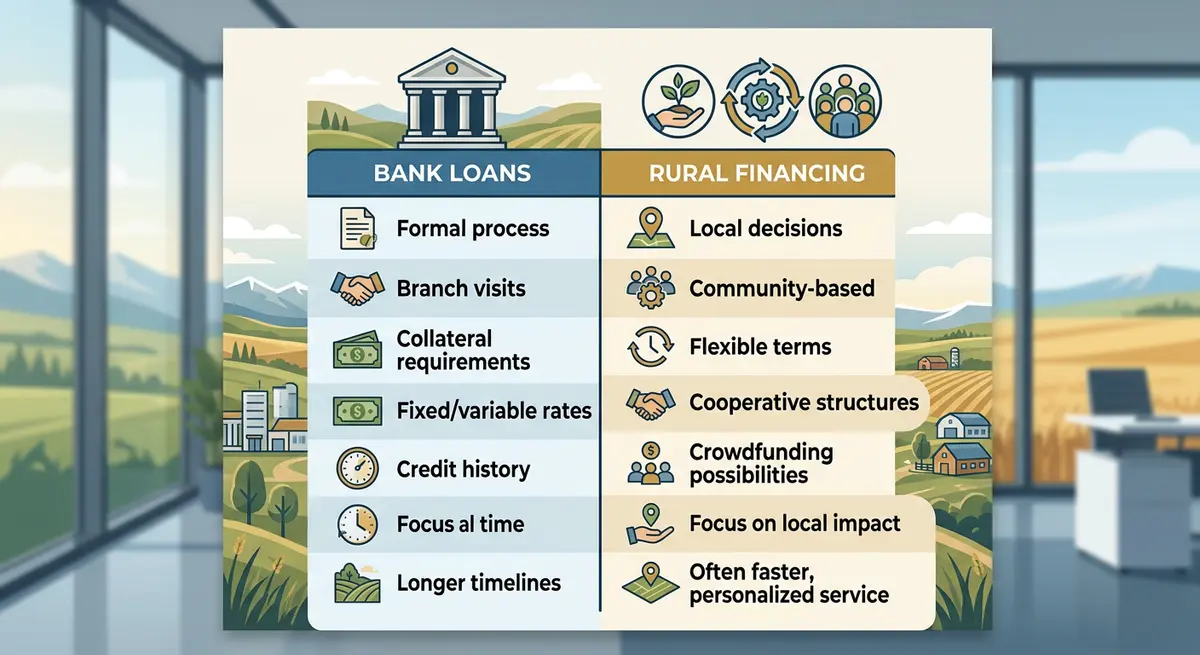

Comparison: Traditional Bank Loans vs. Alternative Rural Financing

To fully grasp the benefits of alternative financing, it is helpful to compare it directly against traditional agricultural or residential loans. The table below outlines the key differences in the 2026 Alberta lending landscape.

| Lending Feature | Traditional Bank Loan | Alternative Rural Financing |

|---|---|---|

| Approval Speed | 45 to 90 days | 7 to 14 days |

| Acreage Limits | House + 10 acres maximum | Unlimited acreage considered |

| Income Verification | Strict T1 Generals & NOAs required | Flexible, stated income accepted |

| Outbuilding Valuation | Zero value assigned | Full appraised value included |

| Credit Score Requirement | Minimum 680+ | No strict minimum (Equity-based) |

Step-by-Step: How to Apply for a Rural Equity Loan in Alberta

Navigating the alternative lending market requires preparation. Because rural properties are complex assets, the underwriting process is heavily focused on due diligence. Follow these five steps to ensure your application is processed efficiently:

- Calculate Your Usable Equity: Determine your property’s estimated current market value and subtract your existing primary mortgage balance. Remember that rural lenders typically cap total borrowing at 65% to 75% LTV.

- Gather Essential Documentation: While income requirements are flexible, you still need to prove property ownership, tax status, and insurance. Review a comprehensive document checklist to ensure you have your property tax assessments, well water certificates, and existing mortgage statements ready before applying.

- Order a Specialized Rural Appraisal: Do not rely on automated valuation models (AVMs) or urban residential appraisers. You must hire an appraiser who specializes in rural properties and understands how to value agricultural infrastructure, zoning bylaws, and land quality.

- Consult with a Specialized Broker: Work with a brokerage that has direct access to private lenders and MICs that specifically fund rural Alberta real estate. Urban brokers often lack the specific lender relationships required to fund agricultural land.

- Review the Term Sheet and Exit Strategy: Carefully examine the interest rate, lender fees, brokerage fees, and the term length (typically 1 to 2 years). Ensure you have a clear exit strategy, such as a future cash-out refinance or property sale, to pay off the principal at the end of the term.

Navigating Unique Rural Property Challenges

Rural properties come with a unique set of legal, environmental, and structural challenges that can impact your financing. Being proactive about these issues will prevent delays during the underwriting process.

Environmental Assessments and Zoning Restrictions

Properties with active agricultural operations, underground fuel storage tanks, or historical industrial use may require an Environmental Site Assessment (ESA Phase 1). Lenders must ensure the land is free from chemical contamination that could destroy its collateral value. If a Phase 1 assessment flags potential issues, a more invasive Phase 2 assessment (involving soil and groundwater testing) may be required.

Additionally, zoning restrictions dictated by Alberta Agriculture and Irrigation can dictate land use, which directly impacts the property’s marketability. A parcel zoned exclusively for agricultural use will be appraised and financed differently than a parcel zoned for country residential development.

Co-Borrowers and Spousal Consent on Rural Land

Ownership structures on family farms and rural estates can be highly complex. If the property is considered a matrimonial home, the Alberta Dower Act requirements mandate explicit spousal consent for any new encumbrances, even if only one spouse is listed on the land title. Navigating this spousal consent is a mandatory legal step that cannot be bypassed.

In cases of marital breakdown, rural equity is frequently used for facilitating spousal buyouts, allowing one partner to retain the farm while the other receives their share of the equity in cash. Furthermore, if operational income is tight, some acreage owners look into adding non-occupant co-borrowers (such as parents or adult children) to strengthen the overall strength of their financing application.

Real-World Case Study: Expanding a Foothills County Hobby Farm

To illustrate the power of alternative rural financing, consider the case of David and Elena, who own a 40-acre hobby farm in Foothills County, just south of Calgary. In early 2026, their property appraised at $1,400,000. They held a primary mortgage with a major bank for $400,000 at a highly favorable fixed rate of 2.8% that they absolutely did not want to break.

They needed $200,000 to build a specialized heated barn for a new equestrian boarding business and to consolidate $45,000 in high-interest credit card debt used for previous property maintenance. Their traditional bank denied the loan, citing that 30 acres of their land held “zero lending value” under their urban guidelines, and their equestrian business income was too new to be considered.

By utilizing an alternative equity loan, they secured the $200,000 they needed behind their first mortgage. The private lender evaluated the full 40 acres and recognized the future income potential of the equestrian facility. The total LTV was only 42.8% ($600,000 total debt divided by $1,400,000 value), making it a highly secure investment for the lender. David and Elena built the barn, launched their business, and plan to roll the secondary loan into a new primary mortgage when their first term matures in two years.

Sarah Jenkins, Senior Underwriter at Alberta Alternative Capital, summarizes this approach: “Cases like David and Elena’s are exactly why alternative lending exists. Traditional banks saw a risk; we saw $1 million in unencumbered equity and a solid business plan. Equity lending is about common sense, not just algorithms.”

Frequently Asked Questions (FAQ)

What types of rural properties qualify for equity financing near Calgary?

Almost all rural property types qualify, including raw land, hobby farms, working agricultural farms, ranches, country estates, and recreational acreages. The primary qualifying factor is the amount of usable equity in the property and its overall marketability in the Calgary surrounding area.

How much equity do I need to get approved on an acreage?

Most alternative lenders require you to retain at least 25% to 35% equity in the property. This means your maximum Loan-to-Value (LTV) ratio—combining your existing primary mortgage and the new secondary loan—cannot exceed 65% to 75% of the property’s appraised value.

Will a lender consider the value of my barns and outbuildings?

Yes. While traditional A-lenders often assign zero value to agricultural outbuildings and excess land, private lenders and Mortgage Investment Corporations (MICs) will consider the full appraised value of all permanent structures, including heated shops, barns, riding arenas, and specialized fencing.

Do I need perfect credit to secure rural financing?

No. Because this type of financing is secured by the hard equity in your real estate, lenders are far more forgiving of past credit issues, low credit scores, or recent consumer proposals, provided there is sufficient equity to mitigate their risk.

How long does it take to fund a rural equity loan?

While traditional agricultural loans can take months to process, alternative rural financing can typically be approved and funded within 7 to 14 business days, assuming the specialized rural appraisal and environmental assessments (if required) are completed promptly.

Can I use the funds to buy livestock or heavy farm equipment?

Absolutely. Once the funds are deposited into your account, there are generally no restrictions on how the capital is deployed. Many rural owners use the funds for agricultural expansion, purchasing tractors, livestock, or consolidating high-interest operational debt.

Conclusion

Securing financing for rural properties near Calgary does not have to be an exercise in frustration. While traditional banks continue to apply rigid, urban-centric underwriting guidelines to complex agricultural assets, alternative equity lenders provide a common-sense solution. By focusing on the true appraised value of your land, outbuildings, and infrastructure, these specialized loans empower acreage owners to access the capital they need for expansion, debt consolidation, and emergency reserves in 2026.

Whether you are looking to build a new heated shop, purchase heavy equipment, or simply consolidate high-interest debt without breaking your favorable primary mortgage rate, understanding your alternative financing options is the first step toward financial flexibility. If you are ready to explore how much equity you can unlock from your rural property, contact our team today for a confidential consultation.