When the Canada Revenue Agency begins garnishing your wages, the impact on your household budget can be devastating. Understanding the critical differences between having your income legally redirected to the CRA and accessing the equity in your Calgary property can mean the difference between years of financial hardship and a clear path to resolving your tax obligations. This guide provides a comprehensive comparison of both options, with specific strategies for Alberta residents facing CRA enforcement actions.

- CRA wage garnishment can seize up to 50% of your disposable earnings without court approval in Canada

- Home equity loans in Calgary can provide lump-sum funding to settle tax debt and stop garnishment immediately

- Alberta homeowners have unique protections under provincial legislation that affect garnishment procedures

- Acting quickly when you receive a garnishment notice dramatically improves your options

- Both solutions have distinct advantages depending on your equity position and monthly cash flow needs

- Professional legal and financial advice is essential before committing to either approach

Understanding CRA Wage Garnishment in Alberta

The Canada Revenue Agency possesses broad powers of enforcement when taxpayers fail to meet their obligations. Unlike traditional creditors who must obtain court judgments before wage garnishment can begin, the CRA can issue a Requirement to Pay notice directly to your employer, compelling them to withhold a portion of your salary and remit it directly to the federal government. This administrative process bypasses the court system entirely, making CRA garnishment one of the most aggressive debt collection mechanisms available to creditors in Canada.

According to the Canada Revenue Agency’s official enforcement guidelines, the agency can garnish up to 50% of your disposable earnings when you have other family dependents, and up to 30% if you have no dependents. The calculation of disposable earnings accounts for basic necessities, but the formula is complex and often results in significant monthly deductions that strain household budgets. Research from the Financial Consumer Agency of Canada indicates that wage garnishment is one of the top three enforcement actions taken by the CRA, with tens of thousands of Canadians affected annually.

In Alberta specifically, the provincial Employment Standards Code provides some framework for wage garnishment, but federal tax obligations take precedence under the Income Tax Act. When your employer receives a Requirement to Pay notice, they are legally obligated to comply within 10 business days or face penalties themselves. This means that even if you dispute the underlying tax debt, the garnishment typically continues while disputes are resolved, creating a prolonged period of reduced income.

Home Equity Loans: A Strategic Alternative for Tax Debt

Home equity loans represent borrowing against the value you have accumulated in your property. In Calgary’s real estate market, where single-family homes in established neighborhoods often carry significant equity positions, these financial products can provide substantial lump-sum capital that borrowers can use to settle outstanding tax obligations. Unlike credit cards or personal loans that come with high interest rates, home equity financing typically offers substantially lower rates because the loan is secured by real property.

The fundamental mechanics work as follows: your home is appraised, and lenders calculate the loan-to-value ratio based on your current mortgage balance and the property’s market value. Most Canadian lenders will extend credit up to 80% of the home’s value minus existing mortgage balances, though private lenders and alternative financing sources may offer higher ratios. For a Calgary homeowner with a $600,000 property and a $300,000 existing mortgage, this could mean access to $180,000 in additional equity financing after accounting for standard lending limits.

As mortgage broker Sarah Mitchell, Senior Broker at Dominion Lending Centres Calgary, explains: “Home equity products have become increasingly popular among clients facing CRA enforcement because the interest rates are typically 4-6% lower than unsecured alternatives, and the lump-sum payout can eliminate tax debt in a single transaction rather than enduring years of monthly garnishment deductions.”

Head-to-Head Comparison: Garnishment vs. Home Equity Solutions

When evaluating your options for resolving CRA tax debt, understanding the fundamental differences between accepting wage garnishment and pursuing home equity financing is essential for making an informed decision that aligns with your financial goals and circumstances.

| Factor | CRA Wage Garnishment | Home Equity Loan Calgary |

|---|---|---|

| Speed of Impact | Begins within 10 business days of employer notification | Typical approval 7-21 days; some private lenders close faster |

| Interest Costs | CRA compounds interest at prescribed rates (currently 6-9%) | Home equity rates typically 5.5-9% depending on credit profile |

| Monthly Payment | Fixed garnishment percentage deducted automatically | Flexible terms; can be structured to match your cash flow |

| Credit Score Impact | Garnishment itself doesn’t report to credit bureaus | New loan inquiry affects score temporarily (15-25 point drop) |

| Risk Level | Low immediate risk but prolonged financial drain | Secured debt; default could lead to foreclosure |

| Tax Deductibility | Not applicable to garnishment amounts | Interest may be deductible if funds used for investment property |

The comparison reveals that neither solution is universally superior. Wage garnishment requires no additional borrowing and poses no risk to your property, but it creates an extended period of reduced income that can persist for years depending on the tax debt amount. Home equity loans provide immediate resolution but introduce new debt obligations and the theoretical risk of foreclosure if payments cannot be maintained.

When Home Equity Loans Make Sense to Stop CRA Garnishment

Not every situation warrants pursuing home equity financing to address CRA tax debt. Understanding the specific circumstances where this strategy provides the greatest benefit helps homeowners make appropriate decisions rather than applying for loans that may create more problems than they solve.

Home equity loans are most advantageous when you have substantial equity accumulated in your property relative to your existing mortgage balance. Calgary’s real estate market has experienced significant appreciation in recent years, meaning many homeowners who purchased properties a decade ago now carry equity positions that would have been impossible to access through traditional refinancing alone. If your equity position exceeds the amount needed to settle your tax debt by a comfortable margin, the loan can accomplish your goal while leaving adequate cushion for future financial emergencies.

Another favorable scenario involves borrowers who have strong, stable income but poor credit scores that prevent them from qualifying for unsecured debt consolidation options. Because home equity loans are secured by collateral, lenders are often willing to approve applicants with credit scores as low as 550, provided the property has sufficient equity. This makes home equity one of the few viable paths to debt resolution for individuals whose credit histories have been damaged by previous financial difficulties.

Consider the case of a Calgary family facing $45,000 in unpaid GST and income tax obligations. With two children and a combined household income of $95,000, the CRA garnishment would redirect approximately $1,500 monthly from the primary earner’s paycheck. By accessing $50,000 in home equity (after accounting for settlement costs and a small buffer), they could satisfy the tax debt entirely, stop the garnishment immediately, and restructure repayment through a home equity loan with a monthly payment of approximately $950, resulting in net monthly income improvement of $550.

The Process: Obtaining Home Equity Financing in Calgary

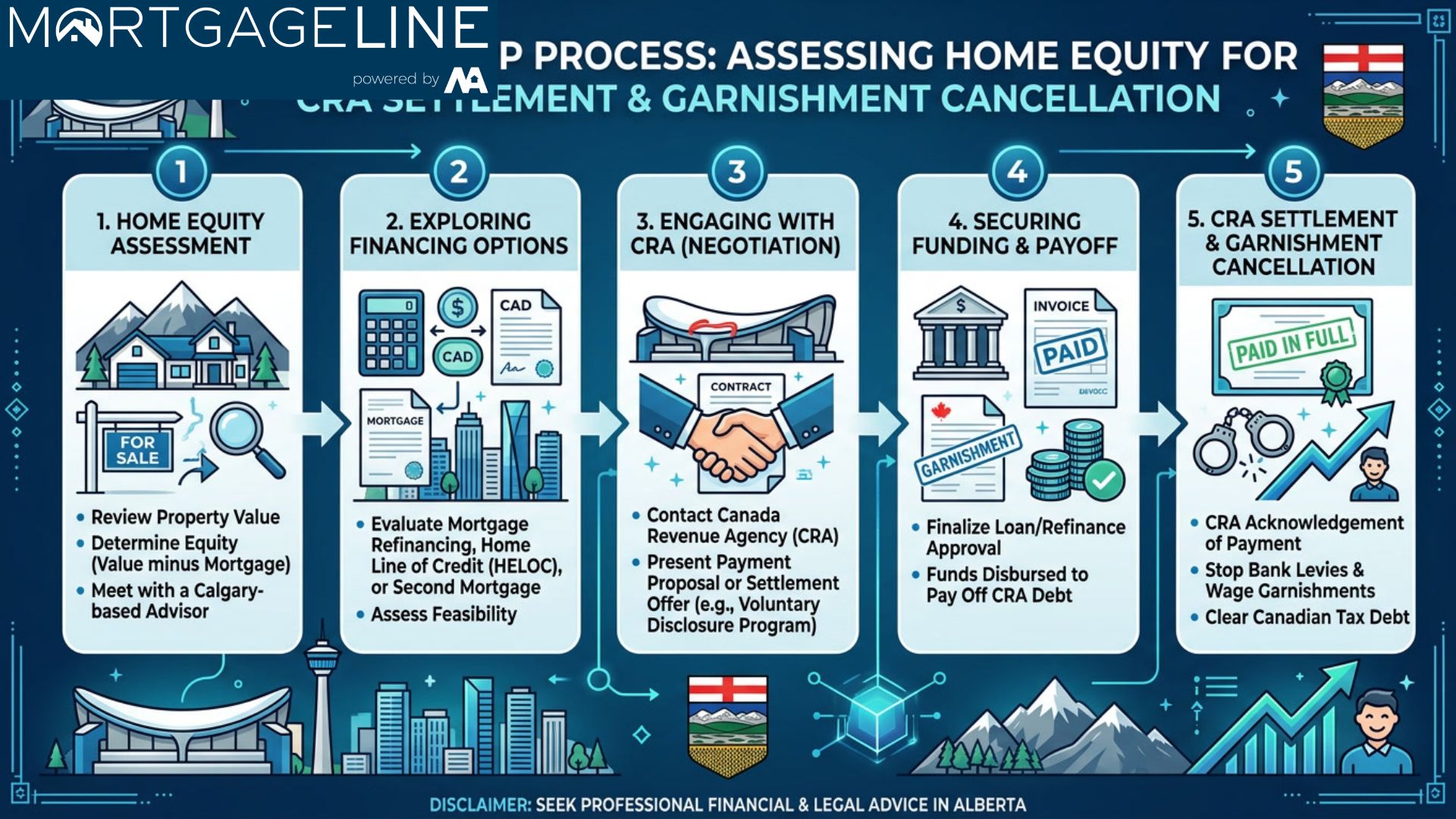

Securing home equity financing to address CRA tax debt involves several distinct phases, each requiring careful attention to documentation, lender requirements, and timing considerations that can affect the outcome of your transaction.

Step 1: Assess Your Equity Position

Before approaching lenders, obtain a current market valuation of your property. This can come from comparative market analysis by a local real estate professional or a formal appraisal. Calculate your available equity by subtracting your existing mortgage balance(s) from the property value, then multiply by 0.80 to determine conventional lending limits. If your tax debt exceeds 80% of your equity, you may need to explore private lenders or alternative structures.

Step 2: Gather Required Documentation

Lenders require comprehensive financial documentation including recent pay stubs, Notice of Assessment from the CRA, bank statements, existing mortgage statements, and property tax bills. For self-employed individuals, two years of Notice of Assessment and financial statements may be necessary. Organizing these documents before applying accelerates the approval process and demonstrates financial responsibility to potential lenders.

Step 3: Compare Lender Options

Calgary homeowners have access to multiple lending channels including major banks, credit unions, mortgage brokers, and private lenders. Banks and credit unions typically offer the lowest rates but have the most stringent approval criteria. Mortgage brokers can access multiple lenders and find products suited to your specific situation. Private lenders offer speed and flexibility but at higher interest costs. Each channel has advantages depending on your credit profile, equity position, and urgency of funding.

Step 4: Complete Application and Appraisal

Once you’ve selected a lender, completing the application typically takes one to two hours. Most lenders will order a formal appraisal of your property, which costs $300-500 and takes five to ten business days. During this period, you can continue gathering any additional documentation the lender requests.

Step 5: Settlement and CRA Payment

Upon loan approval, the closing process typically takes three to five business days. Funds are disbursed directly to you or can be wired directly to the CRA to satisfy the tax debt. Obtain written confirmation from the CRA that your account has been settled in full, then request written confirmation that the wage garnishment has been cancelled. This documentation protects you if any administrative errors occur in the CRA’s system.

Common Mistakes to Avoid

Homeowners pursuing home equity financing to address CRA tax debt frequently encounter pitfalls that can derail their plans or create new financial complications. Being aware of these common errors helps you navigate the process more effectively and achieve the intended outcome.

One of the most significant mistakes is failing to verify that the home equity loan amount will actually satisfy the tax debt completely. The CRA charges compound interest on outstanding balances, meaning the amount owed when you apply for financing may be substantially higher than the amount stated in your most recent notice. Always request a current account balance from the CRA before finalizing your loan amount, and build in a buffer of at least 10% to cover accrued interest between the statement date and the actual payment date.

Another frequent error involves not confirming the garnishment cancellation with the CRA after settlement. Some homeowners assume that paying the tax debt automatically stops the wage garnishment, but the CRA requires explicit written confirmation that enforcement actions have been discontinued. Without this documentation, your employer may continue deducting garnishment amounts for weeks or months until the CRA processes the cancellation.

Borrowers also sometimes underestimate the importance of maintaining emergency reserves after using home equity to pay tax debt. Depleting all available equity to resolve an immediate crisis leaves no financial cushion for future emergencies, which may force you back into debt or create circumstances where you cannot make home equity loan payments. Financial planners generally recommend maintaining at least three to six months of living expenses in accessible savings before committing all equity to debt resolution.

Calgary-Specific Considerations

Calgary’s unique economic landscape and real estate market create specific considerations for homeowners evaluating home equity strategies to address CRA tax debt. The city’s economy, historically tied to oil and gas but increasingly diversified, affects both property values and lending practices in ways that differ from other Canadian markets.

Property values in Calgary have shown resilience despite economic fluctuations, with the Calgary Real Estate Board reporting average single-family home prices of approximately $580,000 as of early 2026. This substantial base value means that homeowners who purchased properties even five to seven years ago often carry significant equity positions that can be leveraged for debt resolution. However, certain neighborhoods and property types have experienced more volatility, which lenders account for when evaluating loan applications.

Alberta’s consumer protection framework provides some advantages for borrowers compared to other provinces, including more flexible regulations around private lending and fewer restrictions on home equity products. This regulatory environment has attracted numerous alternative lenders to the Calgary market, providing homeowners with more options when conventional bank financing is not available. However, this same flexibility means borrowers must exercise additional caution to ensure they are working with reputable, licensed lenders.

The Alberta Court of Queen’s Bench has jurisdiction over most civil matters including foreclosure proceedings, and local legal professionals have extensive experience with home equity products and debt resolution. Engaging a lawyer familiar with both real estate transactions and CRA enforcement matters provides valuable protection when structuring home equity financing to address tax debt.

FAQ: CRA Wage Garnishment and Home Equity Loans in Calgary

How long does CRA wage garnishment continue in Alberta?

Wage garnishment continues until the tax debt is paid in full, including all accrued interest and penalties. For significant tax debts, this can persist for five to ten years or longer. Unlike some provinces, Alberta does not impose statutory limits on the duration of CRA garnishment orders.

Can the CRA take my home instead of garnishing wages?

Yes, the CRA can register a lien against your property or pursue foreclosure if tax debt remains unpaid. However, this process requires more time and administrative steps than wage garnishment, making it a secondary enforcement tool that the CRA typically uses when garnishment is insufficient or unavailable.

What percentage of my wages can the CRA garnish?

The CRA can garnish up to 50% of your disposable earnings if you have family dependents, or 30% if you have no dependents. Disposable earnings are calculated after deducting required payroll deductions, creating a formula that often results in substantial monthly withholdings.

Will a home equity loan affect my credit score?

Yes, applying for a home equity loan generates a credit inquiry that temporarily lowers your credit score by approximately 15 to 25 points. However, making payments on time will gradually improve your score over the following 12 to 24 months, and successfully eliminating the tax debt may ultimately benefit your credit profile.

Can I negotiate directly with the CRA instead of using home equity?

The CRA does offer payment arrangement options and may consider accepting a compromise on certain penalties, but these negotiations can take months or years to complete while garnishment continues. Home equity financing provides immediate resolution but at the cost of new debt obligations.

What happens if I default on a home equity loan used for tax debt?

Defaulting on a home equity loan can result in foreclosure proceedings, meaning you could lose your property to satisfy the secured debt. This risk makes it essential to carefully evaluate your ability to maintain home equity loan payments before proceeding with this strategy.

Are home equity interest rates deductible on my taxes?

Interest on home equity loans is only tax-deductible if the funds are used to generate investment income, such as purchasing rental property or investments. Interest on loans used for personal expenses like tax debt is generally not deductible.

Conclusion

Resolving CRA wage garnishment through home equity financing represents a powerful strategy for Calgary homeowners facing significant tax debt. By accessing the equity accumulated in your property, you can eliminate the CRA’s enforcement action immediately, restore your full income, and establish a clear repayment structure through a secured loan with favorable interest rates. However, this approach requires careful evaluation of your equity position, realistic assessment of your ability to service new debt, and thorough documentation of the settlement process to ensure garnishment is properly cancelled.

The decision between accepting wage garnishment and pursuing home equity financing depends on your specific circumstances including equity position, credit profile, monthly cash flow, and long-term financial goals. For many Calgary homeowners, the immediate restoration of full income and the psychological relief of eliminating CRA enforcement justify the introduction of new secured debt. For others, maintaining existing arrangements while negotiating directly with the CRA may be more appropriate.

Before committing to either approach, consult with a qualified mortgage professional who understands both home equity products and CRA enforcement procedures. The complexity of these transactions and the significant financial stakes involved make professional guidance essential. If you’re ready to explore whether home equity financing can help you resolve your CRA tax debt, our team at The Second Mortgage Store has extensive experience helping Calgary homeowners navigate these exact situations. Visit our blog for additional resources on debt management strategies, or connect with our specialists to discuss your specific circumstances and explore available options.