Creating a payment plan for mortgage arrears in Calgary requires immediately quantifying your financial shortfall, documenting your current income, and presenting a data-driven repayment proposal to your lender before the 90-day default window expires. By proactively addressing missed payments through capitalized arrears, blend-and-extend modifications, or strategic equity leveraging, homeowners can halt foreclosure proceedings, avoid severe credit damage, and stabilize their monthly housing costs. The key to success lies in early communication and proposing a mathematical solution rather than an emotional plea.

Key Takeaways

- Act within 30 days: Contacting your lender before the second missed payment drastically increases your chances of approval for a hardship program.

- Data drives decisions: Lenders require a comprehensive 30-day expense tracker and realistic income projections to approve any modified payment structure.

- Understand capitalization: Rolling missed payments into your principal balance is often the most effective way to resolve immediate cash flow crises.

- Equity is leverage: Homeowners with more than 20% equity have access to alternative financing options that can instantly clear arrears.

- Legal timelines are strict: Failing to establish a plan within 90 to 120 days typically triggers formal legal action in Alberta.

The 2026 Economic Reality for Calgary Homeowners

When monthly obligations outpace household income, homeowners face the daunting reality of mortgage arrears. In Calgary’s shifting 2026 economy, where fluctuating energy sectors and persistent inflation influence housing costs, proactive financial strategies are no longer optional—they are essential for survival. The Financial Consumer Agency of Canada (FCAC) warns that prolonged arrears can quickly trigger negative amortization, a dangerous financial state where your total debt grows despite making partial payments.

Rising borrowing costs over the past few years have made this challenge increasingly pressing. According to recent data from Statistics Canada, household debt now averages $1.79 for every dollar of disposable income. Many homeowners with variable-rate products have hit their trigger rates, meaning their standard payments no longer cover the accrued interest. Consequently, balances increase even when regular contributions are made.

As Marcus Thorne, Senior Underwriter at The Second Mortgage Store, explains: “Lenders in 2026 are highly receptive to structured repayment plans, provided the borrower presents a realistic, data-backed budget rather than vague promises. The institutions do not want your property; they want a predictable return on their capital.”

Step 1: Conduct a Ruthless Financial Assessment

Building a clear financial roadmap starts with an honest, comprehensive evaluation of your household economy. Research indicates that over 60% of homeowners underestimate their total monthly obligations by at least $400 when facing budget gaps. This lack of clarity often delays critical decisions until the lender’s options narrow significantly.

Documenting Income and Categorizing Expenses

Start by listing all verifiable income sources. Next, track every single expense for a 30-day period. You must categorize your spending into non-negotiable survival costs (housing, basic utilities, groceries) and discretionary spending (subscriptions, dining out, entertainment). When you present a proposal to your bank, they will scrutinize your bank statements to ensure you have eliminated discretionary spending before asking for financial relief.

Establishing a Debt Hierarchy

Not all debt is created equal. You must prioritize your debts based on interest rates, penalties, and the security tied to the loan. Unsecured credit cards often demand immediate attention due to compounding interest, but your mortgage must remain the absolute priority to protect your shelter. Understanding how compounding frequency silently increases debt is vital when deciding which secondary debts to pay minimums on while you funnel cash toward your mortgage arrears.

Step 2: Evaluate Your Property Equity and LTV Ratio

Your property’s equity dictates the breadth of your negotiation power. To calculate your Loan-to-Value (LTV) ratio, divide your current outstanding mortgage balance (including arrears and penalties) by the current fair market value of your Calgary home.

For example, if your home is valued at $600,000 and your total outstanding balance is $450,000, your LTV is 75%. This leaves you with 25% equity. Positive equity (an LTV below 80%) opens doors to refinancing, capitalization, or securing alternative credit lines. Conversely, negative equity requires entirely different approaches, such as specialized government relief programs or negotiating a short sale.

If you have substantial equity but poor cash flow, comparing secondary financing to cash-out refinancing is a critical next step. Leveraging this equity can provide the lump sum needed to cure the default instantly.

Step 3: Structuring the Repayment Proposal

Financial institutions process thousands of default files annually. To stand out and secure approval, your proposal must be professional, documented, and mathematically sound. A standard hardship proposal should include:

- The Hardship Letter: A concise, one-page explanation of why you fell behind (e.g., medical emergency, job loss, divorce) and, crucially, why this hardship is now resolved or stabilizing.

- Proof of Income: Recent pay stubs, T4s, or Notice of Assessments proving you have the cash flow to support the proposed new payment.

- The Repayment Formula: A specific calculation showing your standard payment plus a portion of the arrears spread over a realistic timeframe (usually 6 to 12 months).

For instance, if your standard payment is $2,000 and you are $4,000 in arrears, proposing a $2,500 monthly payment for 8 months shows a clear, mathematical path to curing the default.

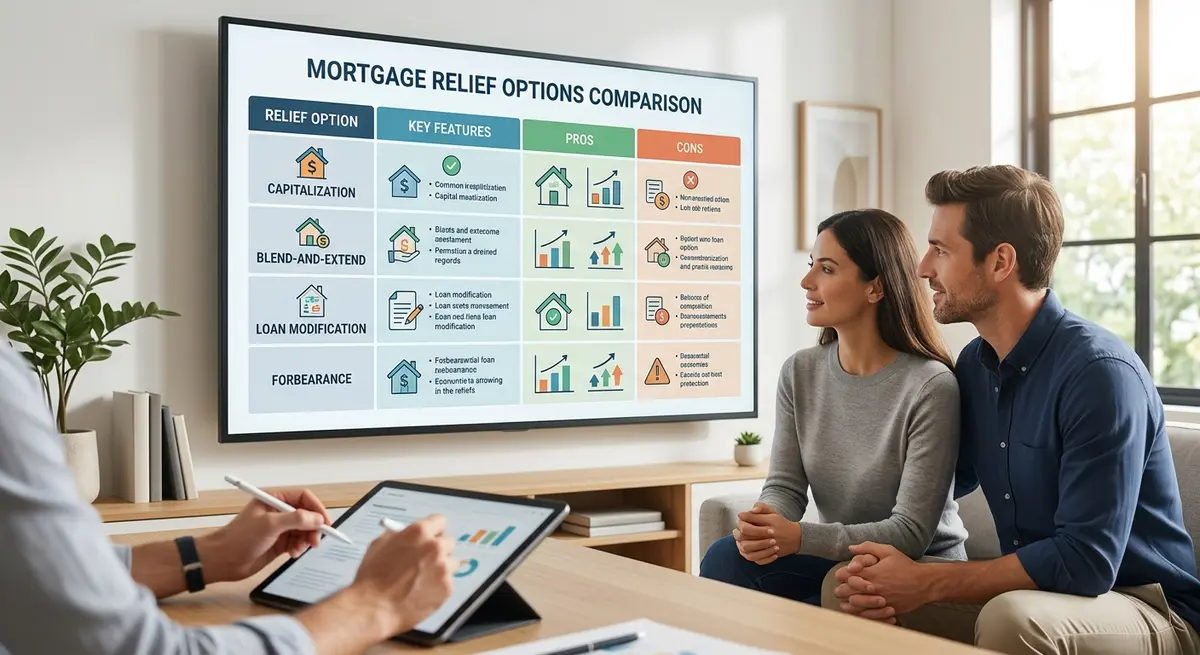

Step 4: Negotiating Relief Options with Your Lender

Most major Canadian banks and credit unions have dedicated retention or hardship departments. You must bypass standard customer service and speak directly to these specialists. When negotiating, you are typically asking for one of the following structural modifications:

| Modification Type | How It Works | Best Suited For | Long-Term Impact |

|---|---|---|---|

| Capitalization of Arrears | Adds the missed payments and fees to the total principal balance of the loan. | Homeowners who have regained income but lack lump-sum cash. | Increases total interest paid over the life of the mortgage. |

| Blend-and-Extend | Blends your current rate with a new rate and extends the term duration. | Borrowers needing to lower their monthly payment immediately. | Locks you into a longer contract, potentially at a mixed rate. |

| Temporary Interest-Only | Pauses principal contributions for 3-6 months. | Those facing short-term, verifiable income disruptions. | Extends the amortization period; principal remains unchanged. |

| Payment Deferral (Skip) | Moves 1-2 missed payments to the end of the mortgage term. | Emergencies where cash flow will return to normal within 30 days. | Accrues additional interest on the deferred amount. |

As Dr. Elena Rostova, a prominent housing economist, notes: “The primary catalyst for irreversible default is not the initial income shock, but the 60-day delay in communicating that shock to the mortgage servicer. Early intervention is the ultimate form of equity protection.”

Navigating the Legal Timeline in Alberta

Understanding the legal framework of Calgary real estate is vital if negotiations stall. Lenders typically allow a strict 90 to 120-day window to resolve arrears before initiating formal foreclosure proceedings. Every missed payment compounds credit damage, potentially lowering your beacon score by 100+ points.

If you fail to establish a payment plan, the lender will issue a demand letter. If ignored, this escalates to formal legal action. It is crucial to understand the legal difference between a notice of default and a statement of claim. A Statement of Claim officially starts the foreclosure process in the Court of King’s Bench of Alberta.

Even if a Statement of Claim is filed, all is not lost. Alberta law provides specific grace periods for homeowners to pay off the arrears and reinstate the mortgage. Familiarizing yourself with Alberta’s specific redemption periods can help you understand exactly how much time you have to secure alternative financing or finalize a payment plan before the court grants a final order of foreclosure timeline.

The Role of Alternative Financing and Secondary Lenders

When traditional banks refuse to negotiate a payment plan—often due to strict federal stress-test regulations or internal risk policies—alternative financing becomes the primary defense against property loss. Local experts at The Second Mortgage Store specialize in Calgary-specific solutions that bypass traditional banking hurdles.

If you have sufficient equity, a secondary lender can provide a home equity loan specifically designed to pay off your primary mortgage arrears, cover property tax shortfalls, and consolidate high-interest consumer debt. Because alternative lenders focus heavily on property equity rather than just credit scores, they are often willing to fund loans even if your credit has been damaged by the recent missed payments.

Furthermore, working with professionals who understand principal reduction strategies ensures that your new loan structure actually helps you pay down debt, rather than just shifting it around.

Executing and Monitoring Your Payment Plan

Once a repayment strategy is agreed upon with your lender, flawless execution is mandatory. According to industry data, nearly 40% of revised agreements fail within the first six months due to unrealistic assumptions about income stability or unexpected expense fluctuations.

Automating Your Success

To prevent a secondary default—which lenders treat with zero tolerance—set up automatic transfers for your new mortgage payment two days before the due date. This buffer protects against banking delays or statutory holidays. Additionally, aim to create a $500 emergency buffer fund specifically earmarked for unexpected bank fees or minor utility spikes.

Quarterly Financial Reviews

Mark calendar reminders every 90 days to reassess your financial health. During these reviews, analyze any income changes, monitor interest rate forecasts from the Bank of Canada, and check property value trends in your specific Calgary neighborhood. If you notice your budget tightening again, proactively contact your lender or mortgage broker before you miss a payment.

Credit recovery strategies work best when paired with consistent, automated payments. Three consecutive on-time installments under a revised plan often begin to rehabilitate your credit score, signaling to future lenders that the financial crisis has been successfully managed.

Conclusion

Managing financial obligations requires decisive action, especially when housing costs threaten your family’s stability. Borrowers facing growing balances must act swiftly to prevent default scenarios. By evaluating your income streams, understanding your property’s equity, and presenting a data-driven proposal to your lender, you can successfully navigate mortgage arrears.

Remember that local expertise proves invaluable in these high-stakes situations. Professionals who understand the nuances of the Calgary market and the specific legal frameworks of Alberta can negotiate terms that individuals often cannot access independently. Delaying action risks permanent credit damage and the devastating loss of your home.

If you are struggling to communicate with your lender or need to explore equity-based solutions to clear your arrears, do not wait until legal action begins. Get in touch with our team at The Second Mortgage Store today to explore tailored, confidential solutions that protect your home and your financial future.

Frequently Asked Questions

What triggers mortgage arrears in Calgary’s current market?

Missed payments are typically triggered by sudden life events such as job loss, medical emergencies, or divorce. In the 2026 economic climate, many arrears are also caused by rising interest rates hitting variable-rate trigger points, causing standard payments to fall short of covering accrued interest.

Can a lender refuse my proposed payment plan?

Yes, lenders are under no legal obligation to accept a payment plan. They will reject proposals that lack realistic repayment timelines, fail to provide proof of stable income, or do not adequately cover the ongoing interest. Presenting a highly detailed, mathematically sound budget improves approval odds significantly.

What happens if I default on a newly negotiated payment plan?

Defaulting on a modified agreement is severely penalized. Lenders will typically revoke the hardship terms immediately, accelerate the loan balance, and initiate formal foreclosure proceedings. It also causes catastrophic damage to your credit score, making alternative financing much harder to secure.

How does capitalizing arrears affect my long-term mortgage costs?

Capitalization rolls your missed payments and late fees into your total principal balance. While this provides immediate cash flow relief by eliminating the need for a lump-sum catch-up payment, it means you will pay interest on those arrears for the remainder of your mortgage amortization, increasing your total lifetime borrowing costs.

Will entering a hardship program ruin my credit score?

While the initial missed payments will lower your score, entering a formal arrears agreement stops the bleeding. Credit bureaus will note the account as having “renegotiated terms.” While this is a negative marker, it is vastly preferable to a foreclosure or a series of unresolved 90-day late markers, and your score will gradually recover with consistent payments.

Can I use a second mortgage to pay off my arrears?

Yes, if you have sufficient equity in your home (typically 20% or more), you can secure a second mortgage to pay off the arrears in a lump sum. This instantly brings your primary mortgage back into good standing, stops foreclosure proceedings, and protects your primary interest rate.